Adjustable Rate Mortgage Calculator

Compare Fixed-Rate and Adjustable-Rate Mortgage Payments

ARM Calculator

Calculation Results

| Comparison | Fixed | ARM |

|---|---|---|

| Beginning Monthly Payment | ||

| Total Payment | ||

| Total Interest | ||

| Maximum Monthly Payment | ||

| Beginning Interest Rate | ||

| Maximum Interest Rate |

Monthly Amortization Schedule

| Fixed Rate | Adjustable Rate | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Month | Date | Interest | Principal | Payment | End Balance | Interest | Principal | Payment | End Balance | Interest Rate |

How This ARM Calculator Works

This ARM Calculator helps you compare a traditional fixed-rate mortgage with an adjustable-rate mortgage (ARM). You can estimate the beginning monthly payment, total payment, total interest, maximum monthly payment, and the effect of future rate adjustments over the life of the loan.

Enter the home price, down payment, loan term, fixed interest rate, adjustable beginning rate, adjustment amount, adjustment frequency, and rate cap. The calculator will generate a side-by-side comparison, charts, and a monthly amortization schedule.

This calculator compares two loan scenarios:

- Fixed-Rate Mortgage: The interest rate remains the same for the entire loan term.

- Adjustable-Rate Mortgage (ARM): The loan starts with a beginning interest rate, then adjusts by the selected amount at the chosen interval until the interest rate cap is reached.

What Is an Adjustable-Rate Mortgage (ARM)?

An adjustable-rate mortgage (ARM) is a home loan that begins with a fixed interest rate for an initial period and then adjusts periodically based on the loan terms. After the fixed period ends, the interest rate may increase or decrease at scheduled intervals, subject to any caps stated in the mortgage agreement.

Because ARMs often start with a lower initial rate than fixed-rate mortgages, they may offer lower beginning monthly payments. However, future payments can rise if interest rates increase.

5/1 ARM vs. 5/6 ARM Explained

A 5/1 ARM and a 5/6 ARM both start with a fixed introductory interest rate for the first five years of the loan. After that initial fixed period ends, the loan becomes adjustable for the remaining 25 years on a typical 30-year mortgage.

With a 5/1 ARM, the interest rate adjusts once every year after the first five years. With a 5/6 ARM, the interest rate adjusts every six months after the first five years.

In simple terms:

- 5/1 ARM: fixed for 5 years, then adjusts every 1 year.

- 5/6 ARM: fixed for 5 years, then adjusts every 6 months.

A 5/6 ARM may react to market changes more frequently, which can lead to payment changes sooner than a 5/1 ARM after the fixed-rate period ends.

Other common ARM products include 7/1 ARMs, 7/6 ARMs, 10/1 ARMs, and 10/6 ARMs. The first number shows how many years the initial rate stays fixed, and the second number shows how often the rate adjusts afterward.

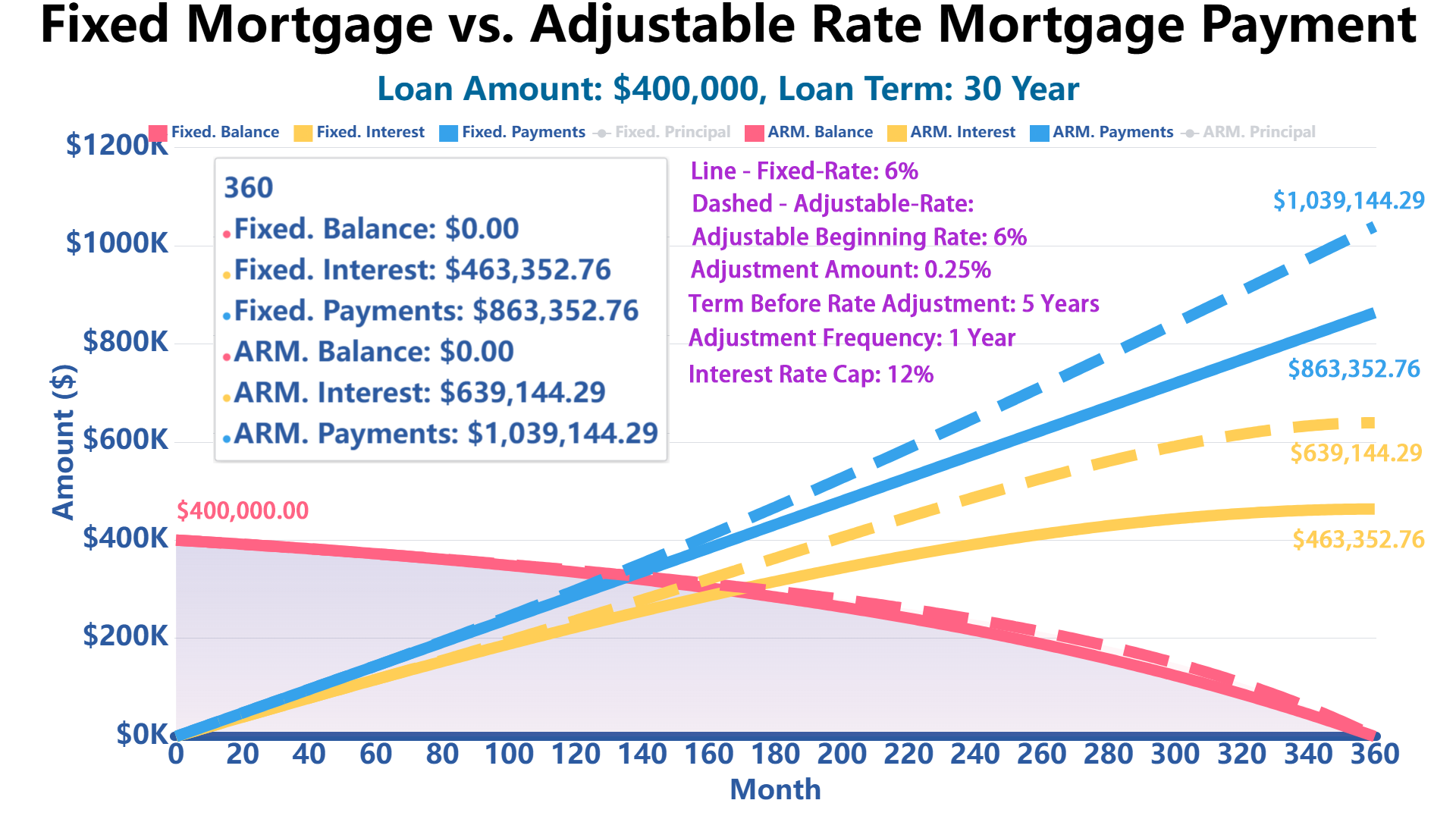

Adjustable Rate Mortgage Example

Let’s say you took out a 30-year 5/1 ARM for $400,000 with an introductory rate of 6%. Here’s how your payment schedule might look, assuming interest rates rose annually by 0.25%. The ARM has a lifetime cap of 12%.

Total Payment: $1,039,144.29, Total Interest: $639,144.29

| Month | Interest Rate | Monthly Payment |

|---|---|---|

| 1 | 6% | $2,398.20 |

| 61 | 6.25% | $2,455.40 |

| 73 | 6.50% | $2,511.62 |

| 85 | 6.75% | $2,566.76 |

| 97 | 7.00% | $2,620.77 |

| 109 | 7.25% | $2,673.55 |

| 121 | 7.50% | $2,725.02 |

| 133 | 7.75% | $2,775.10 |

| 145 | 8.00% | $2,823.70 |

| 157 | 8.25% | $2,870.72 |

| 169 | 8.50% | $2,916.06 |

| 181 | 8.75% | $2,959.62 |

| 193 | 9.00% | $3,001.28 |

| 205 | 9.25% | $3,040.93 |

| 217 | 9.50% | $3,078.46 |

| 229 | 9.75% | $3,113.72 |

| 241 | 10.00% | $3,146.59 |

| 253 | 10.25% | $3,176.93 |

| 265 | 10.50% | $3,204.58 |

| 277 | 10.75% | $3,229.40 |

| 289 | 11.00% | $3,251.23 |

| 301 | 11.25% | $3,269.91 |

| 313 | 11.50% | $3,285.26 |

| 325 | 11.75% | $3,297.12 |

| 337 | 12.00% | $3,305.31 |

| 349 | 12.00% | $3,305.31 |

Real Loan Approval Case: Why I Chose an ARM Instead of a Fixed-rate Mortgage

I once worked with a borrower who was approved for a $520,000 mortgage. The fixed-rate option was quoted at 6.875%, while the 5/1 ARM started at 5.875%. On paper, the ARM looked better because the beginning monthly payment was lower. But the approval decision was not based on the lower first payment alone.

The borrower was relocating for a five-year employment contract and had no plan to keep the property long term. In that case, the initial fixed period of the 5/1 ARM matched the expected ownership period. The borrower used the monthly savings to build a cash reserve instead of stretching the purchase budget.

Here is the important lesson: the ARM worked because the exit plan came first. The borrower had three clear options before the first adjustment: sell the home, refinance if rates improved, or keep enough cash reserves to handle a higher payment.

I would not have recommended the same ARM to a borrower planning to stay for 15 or 20 years with a tight monthly budget. For long-term owners, payment certainty often matters more than the lower introductory rate.

FAQ

Is an ARM Better Than a Fixed-rate Mortgage?

It depends on your goals, loan horizon, and comfort with payment changes. A fixed-rate mortgage offers stability, while an ARM may offer a lower initial rate.

What Does the Interest Rate Cap Mean?

The interest rate cap is the maximum rate the ARM can reach under the assumptions used in this calculator.

What Is a Periodic Adjustment Cap?

A periodic adjustment cap limits how much the rate can change at one adjustment. For example, if the periodic cap is 1%, the rate cannot jump from 5.5% to 8.5% at a single adjustment.

What Is a Lifetime Cap?

A lifetime cap is the highest rate your ARM can reach over the entire loan term. This is one of the most important numbers to check before accepting an ARM.

What Is a Margin?

The margin is the lender’s fixed markup added to the market index after the ARM begins adjusting. For example, if the index is 4.5% and the margin is 2.25%, the adjusted rate would be 6.75%, subject to caps.

What Is an Index?

The index is the market-based rate your ARM follows after the fixed period ends. Common ARM indexes may be tied to broad short-term interest rate benchmarks. When the index rises, your ARM rate may rise. When the index falls, your ARM rate may fall.

What Is Payment Shock?

Payment shock happens when the monthly payment rises sharply after the introductory period. This is the biggest practical risk of an ARM. Always compare the beginning payment with the maximum possible payment.

Does This Calculator Include Taxes and Insurance?

No. This calculator estimates principal and interest only. Property taxes, homeowners insurance, mortgage insurance, HOA fees, and other housing costs are not included.

References

For official consumer information about mortgage loans and adjustable-rate mortgages, please review guidance from the U.S. Consumer Financial Protection Bureau (CFPB) and the U.S. Department of Housing and Urban Development (HUD).

- Consumer Financial Protection Bureau (CFPB) – Adjustable-rate mortgages: https://www.consumerfinance.gov/ask-cfpb/what-is-an-adjustable-rate-mortgage-arm-en-1949/

- Consumer Financial Protection Bureau (CFPB) – Home loan toolkit: https://www.consumerfinance.gov/owning-a-home/explore/home-loan-toolkit/

- HUD – Homeownership and housing counseling resources: https://www.hud.gov/topics/buying_a_home

Write Reply to This Calculator