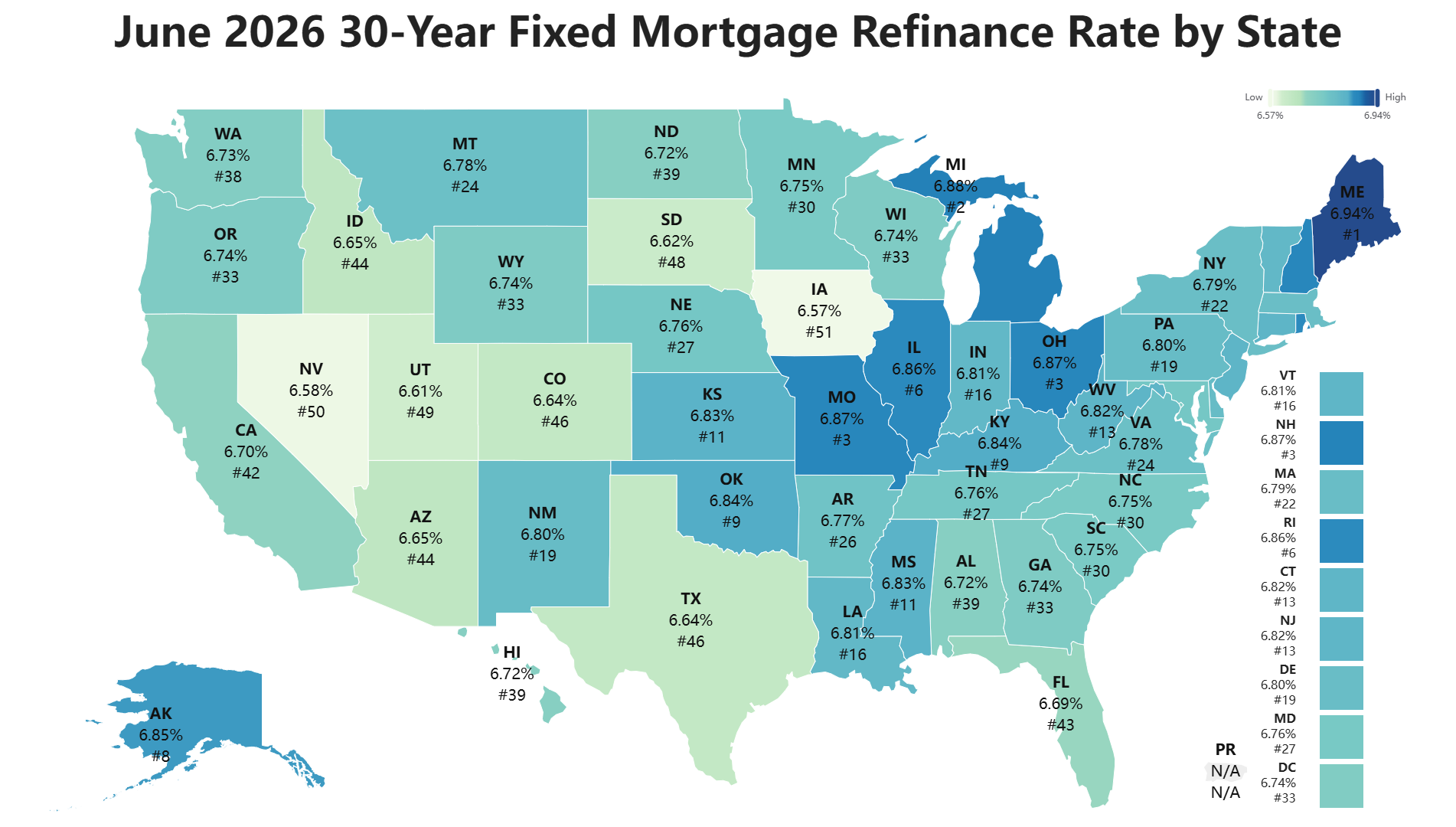

Mortgage Refinance Calculator

Is It Worth Refinancing Your Loan?

Mortgage Refinance Calculator

Current Loan

New Loan

Calculation Results

Current vs. New Loan Comparison

| Item | Current Loan (Remaining) | New Loan | Difference |

|---|---|---|---|

| Principal / Loan Amount | |||

| Monthly Pay | |||

| Loan Term | |||

| Interest Rate / APR | |||

| Total Monthly Payments | |||

| Total Interest | |||

| Cash-Out Amount | |||

| Total Upfront Costs | |||

| Net Cash Proceeds |

Refinancing Visual Comparison

Monthly Payment Schedule Comparison

| Original Schedule | New Schedule | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| Month | Date | Payment | Interest | Principal | End Balance | Payment | Interest | Principal | End Balance |

What Is the Difference Between a Mortgage and a Refinance?

Mortgage = your original home loan.

Refinance = replacing that original loan with a new one under hopefully better terms.

When You Refinance a Loan, Do You Get Money?

You only get money if you do a cash-out refinance. The funds from the loan are first used to pay off your current mortgage, covering closing costs and any prepaid expenses (like mortgage points or fees); any leftover amount is then given to you. If it’s a rate-and-term refinance, no extra cash is given—you’re just adjusting the loan terms.

Hidden Refinance Fees Checklist: What Lenders May Not Emphasize

Closing costs are one of the most misunderstood parts of refinancing. Many borrowers focus only on the interest rate, but the real cost of the refinance is often hidden in the Loan Estimate. Before accepting a refinance offer, review the following fees carefully.

Common Third-Party Fees

- Appraisal Fee: The cost of determining the current market value of your home. This can often range from a few hundred dollars to over $700, depending on the property and location.

- Title Search Fee: A fee charged to verify property ownership and check for liens or title problems.

- Title Insurance: A policy that protects the lender, and sometimes the borrower, against title defects. This can be one of the larger closing costs.

- Attorney or Settlement Fee: In some states, an attorney or settlement agent must review or close the transaction.

- Recording Fee: A local government fee for recording the new mortgage documents.

- Credit Report Fee: A smaller fee, but still worth checking.

- Flood Certification Fee: Used to determine whether the property is located in a flood zone.

- Tax Service Fee: Charged to monitor property tax payments for the lender.

- Prepaid Interest: Interest charged from the closing date until the first scheduled payment date.

- Escrow Funding: Money collected upfront for property taxes and homeowners insurance.

Lender Fees to Negotiate

- Origination Fee: This is one of the most negotiable fees. Ask directly whether the lender can waive or reduce it.

- Processing Fee: Sometimes negotiable, especially if the lender is competing for your business.

- Underwriting Fee: Often presented as fixed, but still worth questioning.

- Rate Lock Fee: Ask whether the lock is free and how long it lasts.

- Discount Points: Points lower your rate, but they only make sense if you keep the loan long enough to recover the cost.

How to Negotiate Refinance Fees

Do not ask the lender only, “What is my rate?” Instead, ask these questions:

- “What is my total lender fee, excluding third-party costs?”

- “Can you provide an origination fee waiver?”

- “How much would the rate increase if I paid zero points?”

- “Can you match or beat this competing Loan Estimate?”

- “Which fees are lender-controlled and which are third-party charges?”

A serious borrower should compare at least two or three Loan Estimates on the same day. Mortgage rates change quickly, so comparing quotes from different days can be misleading.

Is It Good to Refinance a Loan?

Steps to Evaluate:

- Compare Current and New Loan Terms: Understand the current loan balance, interest rate, monthly payment, and compare them to the new loan’s interest rate, term, fees, and any cash-out amount.

- Calculate New Loan Amount: Include any fees, points, and cash-out money into the new loan principal.

- Calculate New Monthly Payment: Use the new loan amount, interest rate, and loan term to estimate the new monthly payment.

- Analyze Payment Difference and Loan Term: Compare the new monthly payment to the current one and note how much the loan term changes.

- Decide Based on Your Financial Situation:

Refinancing is good if you can afford higher payments and want to pay off the loan faster with interest savings.

It is not advisable if the higher payments cause financial strain.

Example:

- Current loan balance: $200,000

- Current rate: 8%

- Current monthly payment: $4,000

- New loan rate: 6%

- Loan term: 3 years

- Fees: 2% points + $1,500 closing costs

- Cash-out: $1,000

Result:

- New loan amount: about $201,000 (only includes cash-out)

- New monthly payment: around $6,115

- Monthly payment increases by $2,115, but loan payoff is much faster.

This straightforward approach helps you understand if refinancing fits your budget and goals.

What Is the Refinance Break-Even Period?

The refinance break-even period tells you how long it takes for your monthly savings to recover your upfront refinancing costs.

The formula is simple:

Break-Even Period = Total Refinance Costs ÷ Monthly Savings

For example, if refinancing costs $7,500 and reduces your monthly payment by $250, the break-even period is 30 months. That means you need to keep the home or keep the new loan for at least 30 months before the refinance begins to produce real savings.

If you sell the home or refinance again before the break-even point, you may lose money even though your monthly payment was lower.

This is why the break-even period is often more useful than the interest rate alone. A lower rate is attractive, but the refinance only becomes profitable if you keep the loan long enough for the savings to exceed the cost.

Expert Case Studies: When Refinancing Worked — and When It Did Not

The following examples are anonymous composite case studies based on common refinance scenarios. They show why the lowest advertised rate is not always the best deal.

Case Study A: The Borrower Who Chased the Lowest Rate and Lost Money

A homeowner with a 740 credit score wanted to refinance mainly because a lender advertised a much lower rate. On the surface, the new loan looked attractive: the monthly payment dropped by about $78.

- Current loan balance: $410,000

- Current rate: 6.875%

- New quoted rate: 6.125%

- Total refinance costs: about $7,500

- Estimated monthly savings: about $78

The issue was the break-even period. At $78 per month in savings, the borrower needed roughly 96 months, or 8 years, just to recover the $7,500 refinance cost.

This borrower was likely to move within five years. Even though the rate was lower, the refinance did not make sense because the borrower would probably sell the home before reaching the break-even point.

Lesson: A lower rate does not automatically mean a better loan. Always compare the monthly savings against the total cost of refinancing.

Case Study B: The Smaller Rate Drop That Actually Made Sense

Another homeowner had a larger loan balance and was not planning to move. The rate reduction was less dramatic, but the economics were much stronger.

- Current loan balance: $685,000

- Current rate: 7.25%

- New rate: 6.50%

- Total refinance costs: about $5,200

- Estimated monthly savings: about $345

The break-even period was about 15 months. Since this homeowner planned to stay in the property for at least seven years, the refinance had a much stronger financial case.

Lesson: A refinance with less than a 2% rate drop can still be excellent when the loan balance is large, fees are controlled, and the homeowner plans to keep the loan long enough.

How Many Times Can I Refinance My House?

There’s no strict limit on how many times you can refinance your house. However, lenders and loan programs often have their own requirements and guidelines, such as:

- Waiting periods: Many lenders require you to wait a certain amount of time (e.g., 6 to 12 months) after your last refinance before you can refinance again.

- Loan seasoning: Some loan types, like FHA or VA loans, have minimum time requirements before refinancing.

- Costs and benefits: Frequent refinancing may not be cost-effective because of closing costs and fees.

- Credit and income: Lenders need to see your ability to repay each time you apply.

It’s best to check with your lender about their specific rules and consider whether refinancing again makes financial sense for you.

Why the Traditional 2% Rule for Refinancing Is Outdated in 2026

The old “2% rule” says that refinancing only makes sense if your new mortgage rate is at least 2 percentage points lower than your current rate. That rule was easy to remember, but it is no longer a reliable decision tool in today’s housing market.

In a high-home-price and high-loan-balance environment, even a smaller rate reduction can produce meaningful savings. For example, a 0.75% rate reduction on a $700,000 mortgage may save more money than a 2% reduction on a much smaller loan. The loan amount, closing costs, remaining term, and expected holding period matter just as much as the rate difference.

The bigger problem is that the 2% rule ignores refinancing costs. A borrower may get a lower rate but pay thousands of dollars in points, lender fees, title charges, appraisal fees, and prepaid costs. If the monthly savings are small, it may take many years to recover those costs.

A Better Method: Break-Even and Net Present Value Analysis

A more modern way to evaluate a refinance is to use two tests:

- Break-Even Period: How many months of savings are required to recover the upfront refinancing costs?

- Net Present Value, or NPV: Are the future savings worth more than the costs when adjusted for time value of money?

The simple break-even formula is:

Break-Even Period = Total Refinance Costs ÷ Monthly Savings

For example, if your refinance costs $7,500 and saves you $150 per month, your break-even period is 50 months. If you plan to sell the home in two years, that refinance probably does not make sense.

NPV goes one step further. Instead of treating every future dollar as equal, NPV discounts future savings back to today’s value. This is important because saving $200 per month five years from now is not the same as having $200 today.

A simplified NPV approach is:

NPV = Present Value of Monthly Savings − Refinance Costs

If the NPV is positive, the refinance may be financially worthwhile. If the NPV is negative, the refinance may look attractive on paper but still destroy value once costs and timing are considered.

Editorial view: In 2026, the 2% rule is too blunt. A borrower with a large mortgage balance may benefit from a rate drop of less than 2%, while another borrower may lose money even with a 2% rate drop if the closing costs are excessive or the break-even period is too long. The smarter question is not “Did my rate drop by 2%?” The better question is: “Will I keep this loan long enough for the refinance to pay for itself?”

How to Improve Your Chances of Qualifying for a Refinance

Most refinance approvals come down to five things: credit, income, debt-to-income ratio, home equity, and documentation. But in practice, the borderline files are where strategy matters most.

From an underwriting perspective, applicants with a debt-to-income ratio near 43% often need to strengthen the file before applying. A borrower can sometimes improve approval odds by paying down revolving credit cards, removing a small monthly debt, documenting bonus income correctly, or choosing a slightly longer loan term to reduce the qualifying payment.

1. Improve Your Credit Before the Rate Quote

A higher credit score can reduce the interest rate and may also reduce loan-level price adjustments. Before applying, check for high credit card utilization, late payments, collection errors, or authorized-user accounts that may be hurting your score.

If your credit card balances are high, paying them down before the lender pulls your credit may have a bigger impact than expected. Utilization is one of the fastest-moving parts of a credit profile.

2. Lower Your Debt-to-Income Ratio

DTI is one of the main reasons refinance applications get denied. If your DTI is close to the lender’s maximum, focus on debts with monthly payments rather than debts with the largest balances.

For example, paying off a small installment loan with a $250 monthly payment may help your approval more than paying extra principal on a large mortgage balance.

3. Document Income Carefully

Borrowers with variable income, commissions, overtime, bonus income, or self-employment income should be especially careful. Lenders may average income over one or two years, and not every deposit in your bank account counts as qualifying income.

If you are self-employed, review your tax returns before applying. Many business deductions reduce taxable income, but they can also reduce the income a lender uses to qualify you.

4. Know Your Home Equity Position

Equity affects pricing, approval, and available refinance options. A borrower with stronger equity usually has more flexibility. If the appraisal comes in lower than expected, the loan may require more cash, a higher rate, or a different structure.

5. Avoid Major Financial Changes During the Process

Do not open new credit cards, finance a car, change jobs, or make large unexplained deposits while your refinance is being reviewed. These changes can trigger additional underwriting conditions or even cause a denial.

Practical advice: Before you apply, ask your lender to estimate your DTI, credit-based pricing, loan-to-value ratio, and total cash needed to close. A refinance should be planned, not rushed.

When You Should Not Refinance

Refinancing is not automatically smart just because a lender offers a lower rate. In many cases, the best financial decision is to keep the loan you already have.

Do Not Refinance If the Break-Even Period Is Too Long

If your refinance costs $7,500 and saves only $80 per month, your break-even period is almost eight years. If you may sell, move, or refinance again before that point, the refinance may never pay for itself.

Do Not Refinance If You Are Resetting the Clock Without a Plan

Many borrowers refinance from a loan with 20 years remaining into a new 30-year loan. The monthly payment may fall, but the borrower may also extend the debt for another decade. This can increase total interest even when the rate is lower.

Do Not Refinance If You Are Paying Points Without Staying Long Enough

Discount points can make sense, but only when the long-term savings exceed the upfront cost. If you are unsure how long you will keep the home, be careful about paying points to buy down the rate.

Do Not Refinance If Your Credit Profile Is Temporarily Weak

If your credit score recently dropped because of high card balances, missed payments, or new debt, waiting a few months may produce a better offer. Refinancing with a weak credit profile can lock you into worse pricing.

Do Not Refinance Just to Access Cash Without a Repayment Plan

A cash-out refinance can be useful for debt consolidation, home improvements, or investment purposes. But using home equity to fund lifestyle spending can be dangerous because unsecured debt becomes secured by your home.

Bottom line: A refinance should improve your financial position after costs, time, and risk are considered. If the deal only looks good because the monthly payment is lower, review the full numbers carefully.

Using Net Present Value to Evaluate a Refinance

Break-even analysis is useful, but it has one weakness: it treats all future savings as if they are worth the same as money today. Net Present Value, or NPV, solves this problem by discounting future savings back to today’s dollars.

In simple terms, NPV asks:

Are the future savings from this refinance worth more than the costs I must pay today?

A simplified version is:

NPV = Present Value of Future Monthly Savings − Upfront Refinance Costs

If the NPV is positive, the refinance may create value. If the NPV is negative, the refinance may not be worthwhile even if the payment is lower.

NPV is especially useful when comparing several refinance offers. One lender may offer the lowest rate but charge high points. Another lender may offer a slightly higher rate with much lower fees. The best offer is not always the lowest rate; it is the option with the strongest net value over your expected holding period.

References

Official Government Information

- Consumer Financial Protection Bureau (CFPB): Understanding Mortgage Refinancing

- Federal Housing Administration (FHA): FHA Loan Information

- Federal Trade Commission (FTC): Refinancing Your Mortgage: What You Need to Know

- U.S. Department of Veterans Affairs: VA Interest Rate Reduction Refinance Loan (IRRRL)

- Fannie Mae: Conventional Loan Products

- Freddie Mac: Primary Mortgage Market Survey (Historical Rates)

Rate Information Sources

- Federal Reserve Economic Data: 30-Year Fixed Rate Mortgage Average

- U.S. Bureau of Labor Statistics: Economic Indicators and Inflation Data

Consumer Protection Resources

- CFPB Complaint Database: Submit Mortgage-Related Complaints

- HUD Housing Counseling: Find a HUD-Approved Housing Counselor

Write Reply to This Calculator