Debt Avalanche Calculator

Compare Paying off Your Current Debts Using the Debt Avalanche Method Versus Making Only Minimum Payments.

Debt Avalanche Calculator

Calculation Results

| Month | Principal | Interest | Payment | Ending Balance | Cumulative Principal | Cumulative Interest | Cumulative Payment |

|---|

How the Debt Avalanche Method Works?

The Avalanche method prioritizes paying off debts with the highest interest rates first while making minimum payments on others. The strategy follows these principles:

- List all debts with their current balances, minimum payments, and APRs

- Sort debts by APR from highest to lowest interest rate

- Pay minimum amounts on all debts to avoid penalties

- Apply extra payments to the highest APR debt until it's eliminated

- Move to next highest APR and repeat the process

- Continue until debt-free - each eliminated debt frees up more money for the next target

How to Use the Debt Avalanche Method to Pay Off Debt?

Debt avalanche example

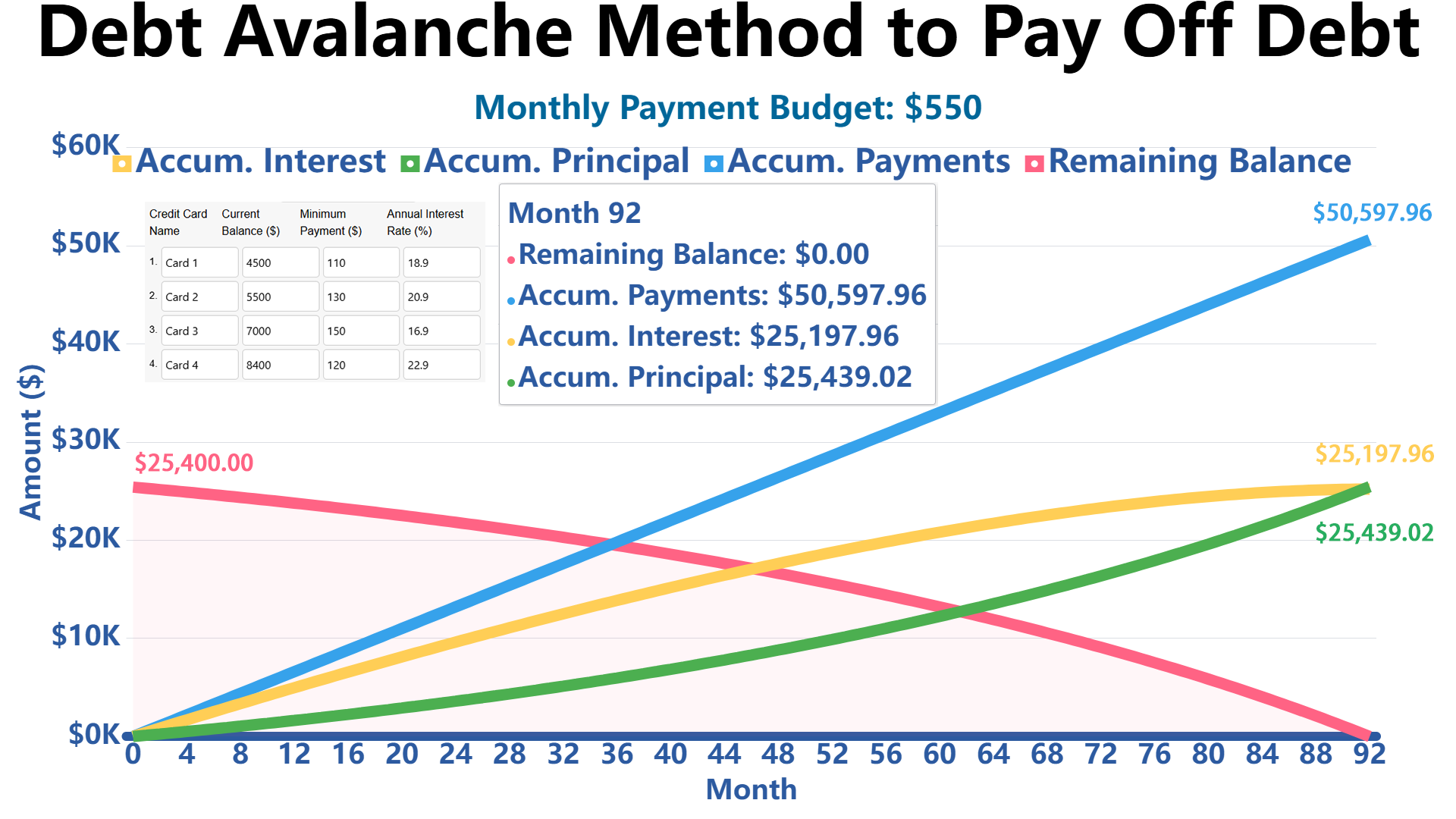

Monthly budget set aside for credit cards: $550

Let’s say you have the following debts:

- Credit card 1 balance: $4,500 at 18.9% interest, with a $110 minimum payment.

- Credit card 2 balance: $5,500 at 20.9% interest, with a $130 minimum payment.

- Credit card 3 balance: $7,000 at 16.9% interest, with a $150 minimum payment.

- Credit card 4 balance: $8,400 at 22.9% interest, with a $120 minimum payment.

With a monthly payment of $550.00, all credit cards will be cleared in 92 months (7 years 8 months). Total paid: $50,597.96, including $25,197.96 in interest.

| Credit Card | APR (%) | Payoff Duration | Total Interest Paid ($) | Total Amount Paid ($) | Repayment Schedule |

|---|---|---|---|---|---|

| #4: Card 4 | 22.90% | 92 months (7 years 8 months) | $13,385.68 | $21,785.68 | Pay $160.00/month until month #66, Then Pay $253.56/month until month #67, Then Pay $270.00/month until month #76, Then Pay $336.01/month until month #77, Then Pay $508.15/month until month #78, Then Pay $550.00/month until month #91, Then Pay $547.96/month until month #92 (final payment). |

| #2: Card 2 | 20.90% | 78 months (6 years 6 months) | $4,551.85 | $10,051.85 | Pay $130.00/month until month #77, Then Pay $41.85/month until month #78 (final payment). |

| #1: Card 1 | 18.90% | 67 months (5 years 7 months) | $2,776.44 | $7,276.44 | Pay $110.00/month until month #66, Then Pay $16.44/month until month #67 (final payment). |

| #3: Card 3 | 16.90% | 77 months (6 years 5 months) | $4,483.99 | $11,483.99 | Pay $150.00/month until month #76, Then Pay $83.99/month until month #77 (final payment). |

References

This calculator is based on established financial principles and formulas. For additional information on debt management and financial planning, consult these authoritative sources:

- Consumer Financial Protection Bureau (CFPB) - Best Strategies for Paying Off Credit Card Debt

- Federal Trade Commission - Paying Off Credit Card Debt

- U.S. Government Accountability Office - Credit Cards: Increased Complexity in Rates and Fees

- Federal Reserve - Credit Card Interest Rates and Consumer Behavior

- MyMoney.gov - Managing Debt (Official U.S. Government financial education website)

- FINRA Investor Education Foundation - Understanding Debt and Credit

Mathematical formulas used in this calculator are based on standard compound interest calculations as defined by financial institutions and regulatory agencies.

Write Reply to This Calculator