Loan Amortization Calculator

See how extra payments reduce your payoff time and save you interest.

Loan Amortization Calculator

Calculation Results

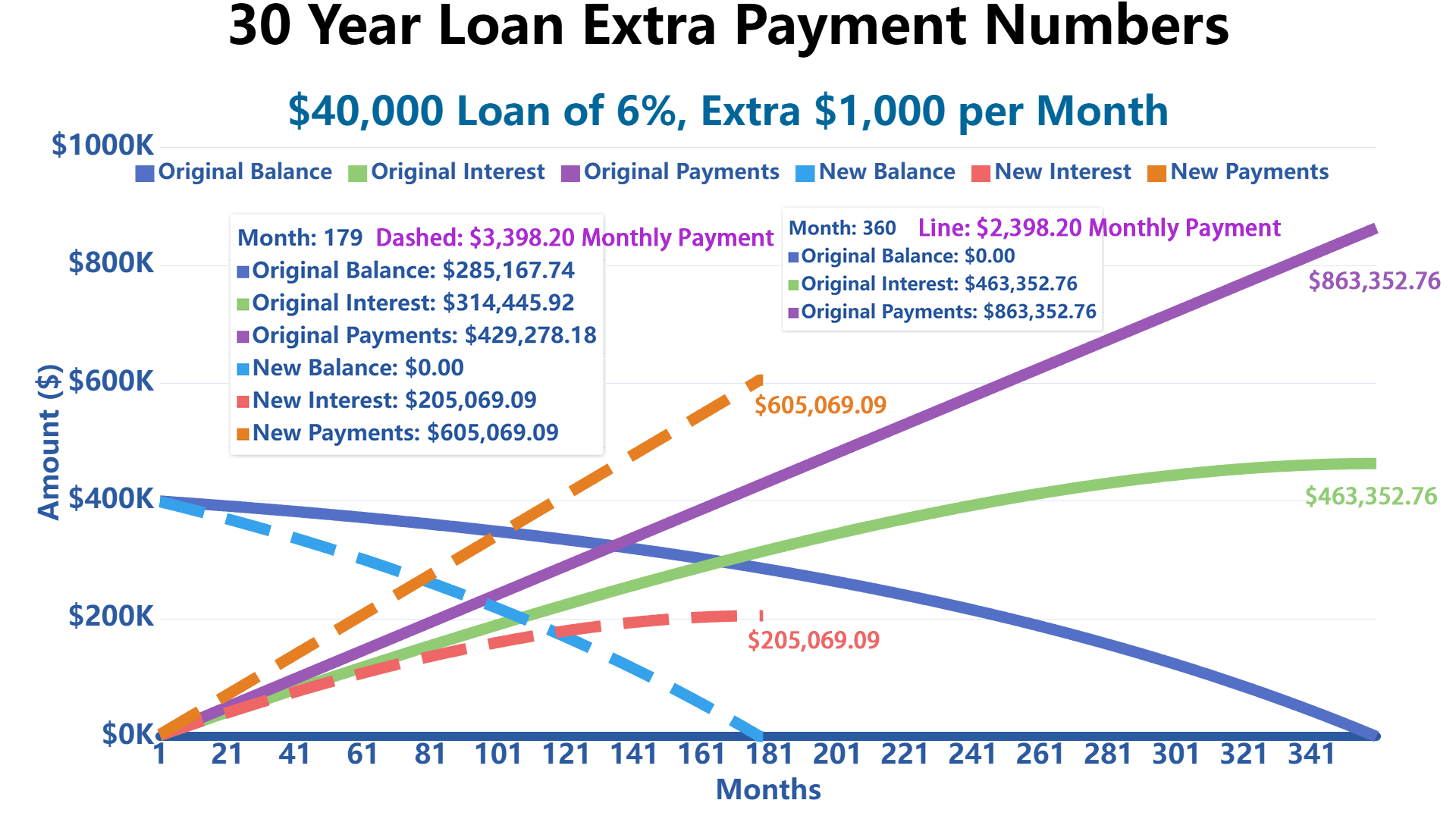

Repayment Details Visualization

Amortization Schedule

| Year | Date | Payment | Interest | Principal | Ending Balance |

|---|

| Month | Date | Payment | Interest | Principal | Ending Balance |

|---|

What Happens If I Pay Two Extra Mortgage Payments a Year?

Paying two extra mortgage payments a year can significantly reduce your loan principal faster, shorten the loan term, and save you money on interest over time.

Real-World Loan Amortization: What This Calculator May Not Capture

A standard loan amortization calculator is useful because it shows how each payment is split between interest and principal. However, real-world loans often include details that can change the actual payoff date, total interest, and savings from extra payments.

Before relying on any amortization estimate, review your loan agreement for compounding rules, payment posting rules, prepayment penalties, adjustable-rate terms, and fees. These details can make the real cost of borrowing different from a simple fixed-rate schedule.

| Real-World Factor | Why It Matters | What to Check |

|---|---|---|

| Compounding Frequency | Some loans calculate interest monthly, while others accrue interest daily. Daily accrual can make payoff timing more sensitive to the exact payment date. | Look for terms such as daily simple interest, monthly compounding, or interest accrual method. |

| Payment Posting Date | An extra payment may not reduce interest immediately if the lender posts it later or applies it first to fees instead of principal. | Confirm when payments are credited and whether extra payments go directly to principal. |

| Prepayment Penalty | Some lenders charge a fee if you pay off the loan early or make large principal reductions. | Review the note, payoff statement, and prepayment clause before making extra payments. |

| Adjustable Rate | For ARM loans, the interest rate can change after the fixed period, which changes future payments and interest costs. | Check the index, margin, adjustment caps, reset frequency, and first adjustment date. |

| Escrow and Servicing Fees | Your actual monthly mortgage bill may include taxes, insurance, mortgage insurance, or servicing charges that are not part of principal and interest. | Separate principal and interest from escrow, insurance, taxes, and other fees. |

Extra Payment Strategy Analysis: Monthly Extra Payments vs. One-Time Annual Payments

Extra payments reduce interest because they lower the outstanding principal. But timing matters. Paying extra earlier usually saves more interest than waiting, even if the total extra amount is the same.

For example, paying an extra $100 every month and paying a one-time $1,200 at the end of the year both add up to $1,200 per year. However, the monthly strategy usually saves slightly more interest because the principal is reduced throughout the year instead of all at once.

| Strategy | How It Works | Typical Result |

|---|---|---|

| Extra $100 Monthly | You add $100 to each monthly payment and instruct the lender to apply it to principal. | Principal falls earlier, so interest usually drops faster over time. |

| Extra $1,200 Once a Year | You make one annual lump-sum principal payment, often after receiving a bonus or extra paycheck. | Still helpful, but interest savings may be slightly lower because the extra principal reduction happens later. |

| Biweekly Payment Strategy | You pay half of your monthly payment every two weeks, resulting in 26 half-payments per year, or 13 full payments. | This creates the effect of one extra monthly payment per year and can shorten the loan term. |

The key principle is simple: the sooner a payment reduces principal, the sooner future interest is calculated on a smaller balance. That is why frequent extra payments can outperform delayed lump-sum payments, even when the annual extra amount is identical.

However, the best strategy depends on your cash flow. Monthly extra payments may produce better interest savings, while annual lump-sum payments may be easier for people who receive bonuses, commissions, tax refunds, or seasonal income.

Biweekly Payment Strategy: Why It Can Work

A biweekly payment plan is often marketed as a way to pay off a mortgage faster. The mechanism is not magic. It works because there are 52 weeks in a year, so making one half-payment every two weeks creates 26 half-payments, which equals 13 full monthly payments per year.

That extra full payment reduces principal, which can shorten the payoff timeline and lower total interest. However, borrowers should be careful with third-party biweekly payment services. Some charge setup fees or hold payments before sending them to the lender, which can reduce or delay the benefit.

A practical alternative is to divide one monthly payment by 12 and add that amount to each regular monthly payment. For example, if your monthly principal and interest payment is $2,400, adding $200 per month creates roughly the same effect as making one extra payment per year.

Prepayment Penalties and Hidden Costs: Read This Before Paying Extra

Extra payments are usually beneficial, but they are not always free. Some loan contracts include a prepayment penalty, which means the lender may charge a fee if you pay off the loan early, refinance too soon, sell the property, or make large principal reductions within a restricted period.

Prepayment penalties are more common in certain commercial loans, investment-property loans, private loans, subprime loans, and some non-qualified mortgage products. They may also appear in specialized financing structures where the lender expects a minimum interest return.

For residential mortgages, many standard consumer protections limit or restrict prepayment penalties, but borrowers should still check their exact loan documents. FHA loans generally do not allow traditional prepayment penalties, but borrowers may still encounter timing-related interest rules, payoff statement requirements, or servicing procedures that affect the final payoff amount.

| Potential Issue | How It Can Affect You | Action Step |

|---|---|---|

| Prepayment Penalty | Your interest savings may be reduced or offset by a lender fee. | Ask the lender for a written payoff quote and review the prepayment clause. |

| Extra Payment Not Applied to Principal | The payment may be treated as a future payment instead of reducing the loan balance. | Write or select “apply to principal” when making extra payments. |

| Late Posting | Interest may continue accruing until the payment is officially posted. | Confirm the lender’s payment cutoff time and posting rules. |

| Third-Party Payment Service Fees | Fees can reduce the benefit of biweekly or accelerated payment plans. | Compare the cost of the service with simply paying extra directly. |

How Do Banks Calculate Amortization?

Banks generally calculate amortization by using the loan balance, interest rate, payment frequency, and remaining term to determine how much of each payment goes to interest and how much goes to principal. For a fixed-rate loan, the scheduled payment is usually designed so that the loan reaches a zero balance at the end of the term if every payment is made on time.

The standard monthly payment formula is:

M = P × [r(1 + r)^n] / [(1 + r)^n - 1]

In this formula, M is the monthly payment, P is the loan principal, r is the monthly interest rate, and n is the total number of monthly payments.

In actual banking operations, the calculation can be more nuanced. Many lenders accrue interest daily between payment dates, then collect the accrued interest when the payment is posted. If a loan starts or pays off in the middle of a month, the lender may calculate odd-days interest or per diem interest for the partial period.

This is why a payoff quote from the lender may differ slightly from a calculator estimate. The lender’s payoff amount may include daily interest through the payoff date, unpaid fees, escrow adjustments, recording fees, late charges, or other servicing items.

Why Your Calculator Result May Differ From Your Lender’s Payoff Quote

This calculator provides an estimate based on the information entered. Your lender’s actual payoff quote may be different because lenders use the exact loan contract, payment history, posting dates, accrued interest, fees, and escrow records.

| Reason for Difference | Explanation |

|---|---|

| Daily Interest Accrual | The lender may charge interest through the exact payoff date, not just the end of the last full month. |

| Partial-Month Interest | If your loan begins or ends mid-month, the lender may calculate interest for the exact number of days. |

| Fees and Charges | Late fees, payoff statement fees, recording fees, or servicing fees may be included in the final payoff. |

| Escrow Adjustments | Taxes, insurance, and escrow balances may affect the final settlement amount. |

| ARM Rate Changes | If the loan has an adjustable rate, future payments may change after the rate resets. |

For the most accurate payoff number, request an official written payoff statement from your lender and confirm how long the quote is valid.

References

- Consumer Financial Protection Bureau - What is Amortization?

- U.S. Department of Treasury - Interest Rates and Debt Management

- Federal Reserve - Understanding Interest Rates

- FDIC Consumer Resources

Write Reply to This Calculator