RV Loan Calculator

Calculate Monthly Payments for Recreational Vehicle & Truck Camper

RV Loan Calculator

Calculation Results

Amortization Table

| Month | Date | Payment | Principal | Interest | End Balance |

|---|

| Year | Date | Payment | Principal | Interest | End Balance |

|---|

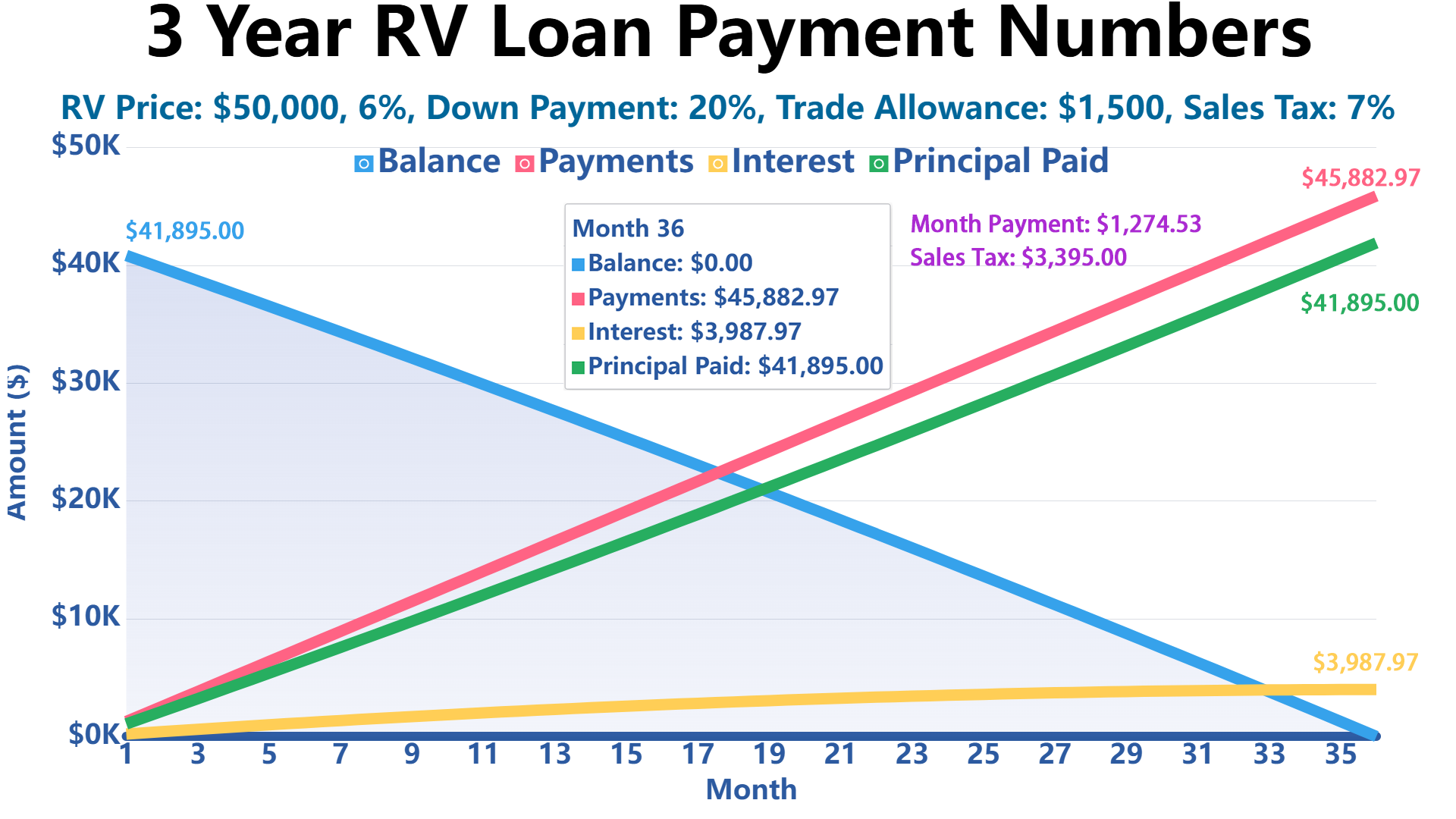

Payment Visualization

RV Loan Reality Check: The Loan Term Changes Everything

RV buyers often focus on the monthly payment, but the real cost of financing shows up in the total interest paid over the life of the loan. A longer term can make an expensive RV feel affordable, but it may also keep you in debt long after the RV has lost a large portion of its value.

The example below assumes an $80,000 RV loan at 6.5% APR. The monthly payment gets smaller as the loan term increases, but the total interest rises sharply.

| Loan Term | Estimated Monthly Payment | Total Interest Paid | Total of Payments |

|---|---|---|---|

| 10 years / 120 months | $908 | $28,984 | $108,984 |

| 15 years / 180 months | $697 | $45,486 | $125,486 |

| 20 years / 240 months | $596 | $63,137 | $143,137 |

Why a 20-Year RV Loan Can Be Risky

A 20-year term can lower the monthly payment, but it also slows down principal repayment. That matters because RVs typically depreciate much faster than real estate and often faster than the loan balance falls. If you sell or trade the RV early, you may owe more than the RV is worth.

Estimated RV Monthly Payments by Price and Interest Rate

The table below gives a quick payment estimate for common RV price points. It assumes a 60-month loan, a 20% down payment, and principal-and-interest payments only. Use the calculator above for a more complete estimate that includes your exact down payment, trade allowance, taxes, and loan term.

| RV Price | Loan Amount | 5% APR | 6.5% APR | 8% APR |

|---|---|---|---|---|

| $20,000 | $16,000 | $302 | $313 | $324 |

| $30,000 | $24,000 | $453 | $469 | $487 |

| $40,000 | $32,000 | $604 | $626 | $649 |

| $50,000 | $40,000 | $755 | $782 | $811 |

| $70,000 | $56,000 | $1,057 | $1,095 | $1,136 |

| $100,000 | $80,000 | $1,510 | $1,564 | $1,622 |

These estimates do not include insurance, fuel, maintenance, campground fees, storage, registration, sales tax, or dealer add-ons.

Underwater RV Loans: The Risk Many Buyers Miss

Being underwater on a loan means your loan balance is higher than the resale or trade-in value of the RV. This risk is especially important with RVs because many models lose value quickly during the first several years of ownership.

If Your Down Payment Is Below 15%, Be Careful

With a small down payment, taxes and fees rolled into the loan, and a long repayment term, many RV owners can become underwater almost immediately. A buyer who puts down less than 15% may still owe more than the RV is worth in years 2 through 5, especially on a 10- to 20-year loan.

The risk is even higher if the RV was purchased at full retail price, includes dealer add-ons, or is financed with an extended service contract, gap coverage, accessories, or sales tax included in the loan.

Example: How the Underwater Risk Happens

Assume a buyer purchases an RV for $80,000, puts down 10%, and finances the remaining $72,000 over 15 years. If the RV loses 20% to 25% of its market value in the first year, the RV may be worth roughly $60,000 to $64,000 while the loan balance may still be close to the original financed amount.

That gap can make it expensive to sell, trade, or refinance. In practical terms, you may need to bring cash to the dealership just to exit the loan.

How to Reduce the Risk

- Put at least 15% to 20% down when possible, especially on new RVs or long-term loans.

- Avoid rolling every fee into the loan if doing so pushes your loan-to-value ratio too high.

- Compare the loan balance against resale value each year using market listings and NADA Values.

- Choose the shortest term you can comfortably afford instead of focusing only on the lowest monthly payment.

- Consider gap coverage carefully if your down payment is small, but understand the exclusions before buying it.

RV Loan Case Studies

The best RV loan is not the same for every buyer. Credit score, cash reserves, retirement income, trade-in equity, and how long you plan to keep the RV all affect the right financing strategy. The following case studies are realistic examples for educational purposes.

Case Study A: Retired Couple With 720 Credit Buying an $80,000 Class A Motorhome

Profile: A retired couple has a 720 credit score, stable pension income, and $25,000 in available cash. They want a Class A motorhome priced at $80,000 and plan to travel seasonally for the next 8 to 10 years.

Financing challenge: The dealer offers a 20-year loan to make the payment look comfortable. The monthly payment is lower, but the couple would pay much more interest and could remain upside down for several years.

Better approach: A 10- or 12-year term with a 20% down payment gives them a healthier balance between monthly affordability and total interest cost. Because they have good credit, they should get a credit union pre-approval before visiting the dealer finance office.

Takeaway: For financially stable retirees, the lowest payment is not always the safest choice. Preserving cash is important, but avoiding a 20-year debt on a depreciating RV can be just as important.

Case Study B: Young Family With 660 Credit Buying a $35,000 Travel Trailer

Profile: A family with a 660 credit score wants a $35,000 travel trailer. They have $5,000 for a down payment and plan to tow with a vehicle they already own.

Financing challenge: Their credit is fair, not poor, but they may receive a higher APR than advertised promotional rates. If they add accessories, sales tax, and an extended warranty into the loan, the amount financed could rise quickly.

Better approach: They should keep the term near 60 to 84 months if possible, avoid unnecessary add-ons, and compare at least three lenders. A slightly cheaper trailer may create a much safer monthly budget once insurance, storage, campsite fees, and maintenance are included.

Takeaway: For buyers with mid-tier credit, controlling the purchase price and add-ons usually matters more than stretching the loan term.

Case Study C: Self-Employed Buyer With Strong Income Purchasing a $120,000 Fifth Wheel

Profile: A self-employed buyer has strong income but irregular monthly cash flow. They want a $120,000 fifth wheel and plan to use it for extended trips.

Financing challenge: Even with good income, lenders may request stronger documentation, larger reserves, or a higher down payment. A long loan term may look attractive because it protects monthly cash flow, but it can create a long period of negative equity.

Better approach: A larger down payment of 20% or more can improve approval odds and reduce underwater-loan risk. The buyer should also keep a separate maintenance reserve because large fifth wheels can have expensive tires, brakes, roof maintenance, and appliance repairs.

Takeaway: Self-employed buyers should optimize for lender confidence and cash-flow flexibility without ignoring depreciation risk.

Is RV Loan Interest Tax Deductible?

RV loan interest may be tax deductible only in specific situations. In general, an RV must qualify as a second home for the interest to potentially be treated like qualified residence interest. That usually means the RV must have basic living facilities, including sleeping space, cooking facilities, and toilet facilities.

2026 Tax Compliance Note

For 2026 planning, the practical test remains focused on whether the RV functions as a qualified residence. A simple cargo trailer, pop-up without permanent facilities, or vehicle used only for transportation generally will not meet the second-home standard. A motorhome, fifth wheel, or travel trailer with dedicated sleeping, cooking, and bathroom facilities is more likely to qualify.

Deductibility can also depend on how the loan is secured, your total mortgage debt, whether the RV is used personally or rented out, and whether you itemize deductions. Keep the purchase agreement, loan documents, and proof of RV facilities with your tax records.

This is a tax-sensitive area, so confirm your specific situation with a qualified tax professional before claiming the deduction.

FAQ

What Credit Score Do I Need for an RV Loan?

Most RV lenders prefer a credit score of at least 600 to 650, but the best rates usually go to borrowers above 700. For large motorhomes or longer terms, lenders may look beyond the score and review debt-to-income ratio, down payment, liquidity, and prior installment-loan history.

From a lender's perspective, an RV is a luxury asset, not a necessity. That means underwriting can be less forgiving than a basic auto loan, especially when the loan amount is high.

How Much Should I Put Down on an RV?

A 10% to 20% down payment is common, but for RVs I prefer to see buyers aim for 15% to 20% whenever possible. The reason is simple: RVs depreciate quickly, and a small down payment can leave you underwater early in the loan.

If you are financing sales tax, dealer fees, accessories, and an extended warranty, a 10% down payment may not provide much real equity. A larger down payment gives you more flexibility if you need to sell or trade sooner than expected.

Can I Finance a Used RV?

Yes, used RV financing is widely available. However, lenders often care about the RV's age, mileage, condition, book value, and whether it is being purchased from a dealer or private seller. Older RVs may require shorter loan terms, higher rates, or larger down payments.

Before financing a used RV, compare the selling price with NADA Values and recent market listings. A clean-looking RV can still have expensive hidden issues such as roof leaks, soft floors, slide-out problems, or aging tires.

What Is the Maximum Loan Term for an RV?

Some RV loans can run as long as 20 years, especially for expensive motorhomes and fifth wheels. That does not mean a 20-year term is always wise. Longer terms reduce the monthly payment but increase total interest and extend the period where you may owe more than the RV is worth.

A good rule of thumb: use the longest term only if you need payment flexibility, but make extra principal payments when cash flow allows. Make sure the loan has no prepayment penalty before using this strategy.

Should I Finance Through a Dealer, Bank, or Credit Union?

As a former banking executive, my advice is to get a credit union or bank pre-approval before you let the dealer arrange financing. This gives you a real baseline rate and stops the dealer finance office from controlling the entire conversation.

Here is the part many buyers do not realize: dealers may be allowed to add a finance markup to the lender's buy rate. For example, the lender may approve you at one rate, and the dealer may present a slightly higher rate, keeping part of the difference as compensation. That does not make dealer financing bad, but it means you should negotiate it like any other profit center.

The strongest strategy is to walk in with a written pre-approval, then ask the dealer if they can beat it without adding unwanted products or extending the term.

Is RV Loan Interest Tax Deductible?

RV loan interest may be deductible if the RV qualifies as a second home and the loan meets applicable tax rules. For an RV to potentially qualify, it generally needs dedicated sleeping, cooking, and toilet facilities.

Do not assume every camper or trailer qualifies. The details matter, including how the loan is secured, how you use the RV, whether you rent it out, your total mortgage-interest limits, and whether you itemize deductions. Keep your documentation and ask a tax professional before claiming the deduction.

Should I Include Taxes and Fees in the RV Loan?

Including taxes and fees in the loan lowers the cash needed at signing, but it increases the amount financed and can raise the risk of being underwater. This matters more with RVs than with many cars because RV depreciation can be steep in the first few years.

If rolling taxes and fees into the loan pushes your loan amount close to or above the RV's market value, consider increasing your down payment or choosing a less expensive RV.

What Costs Should I Budget for Beyond the Monthly Payment?

The loan payment is only one part of RV ownership. Budget for insurance, registration, maintenance, tires, storage, campground fees, fuel, winterization, repairs, and possible HOA or parking restrictions.

For larger motorhomes and fifth wheels, maintenance surprises can be significant. A lower monthly loan payment does not help much if the total ownership cost strains your budget.

References

Government Resources

- Federal Trade Commission - Vehicle Financing Guide

- Consumer Financial Protection Bureau - Auto Loans

- USA.gov - Buying a Vehicle

- IRS Publication 936 - Home Mortgage Interest Deduction

Industry Resources

Write Reply to This Calculator