Mortgage Tax Savings Calculator

Estimate Mortgage Interest Deduction Savings

Mortgage Tax Savings Calculator

Calculation Results

Visual Charts

Detailed Amortization Schedule

| Month | Starting Balance | Payment | Tax Savings | Principal | Interest | Ending Balance |

|---|

| Year | Starting Balance | Payment | Tax Savings | Principal | Interest | Ending Balance |

|---|

How Does the Mortgage Interest Tax Deduction Work?

In the U.S., mortgage interest can reduce your taxable income, but only when it actually helps you itemize deductions. Under current mortgage-interest deduction rules, interest is generally deductible only on up to $750,000 of qualified home loan debt, or $375,000 if married filing separately.

That means a larger mortgage does not always create a larger tax break. If your loan is above the deductible debt limit, the interest tied to the excess balance may not count. And if your total itemized deductions are still below your standard deduction, your mortgage interest may not create any additional tax savings at all.

This calculator helps you estimate the combined federal and state tax impact of your mortgage interest, points, and closing costs. It also checks whether your mortgage deduction is likely to clear the standard deduction threshold, so you can see the difference between a theoretical tax benefit and the savings you may actually receive.

Standard Deduction vs. Itemized Deduction Quiz

Mortgage interest only creates a real tax benefit if your total itemized deductions exceed your standard deduction. In other words, paying mortgage interest does not automatically mean you will save taxes.

Step 1

Add your non-mortgage itemized deductions, such as property taxes, state and local taxes, charitable donations, and eligible medical expenses.

Step 2

Compare that amount with your standard deduction.

Step 3

Only the portion that pushes your total itemized deductions above the standard deduction produces an actual tax benefit.

This calculator estimates both the gross mortgage-interest tax savings and the more realistic savings after considering the standard deduction threshold.

High-Tax-State Comparison: California vs. Texas

Two buyers can purchase the same $800,000 home and still experience very different tax outcomes. The hidden difference often comes from state income tax, property tax, and whether the buyer is already close to itemizing.

Example: Buying an $800,000 Home

Assume two buyers purchase an $800,000 home with a $640,000 mortgage. The mortgage balance is below the $750,000 federal mortgage-interest deduction limit, so the interest may be fully eligible before applying the standard deduction test.

| Scenario | California Buyer | Texas Buyer |

|---|---|---|

| State Income Tax | Often high | No state income tax |

| Property Tax | Usually lower as a percentage of value | Often higher as a percentage of value |

| SALT Deduction Pressure | May hit the SALT cap quickly | Property tax may still push toward the SALT cap |

| Mortgage Interest Benefit | Can be more valuable if the taxpayer itemizes and has a high marginal rate | Can still help, but the lack of state income tax may reduce the combined tax rate effect |

In California, a high-income buyer may already have enough state taxes, property taxes, and charitable deductions to itemize. In that case, mortgage interest may create a more direct tax benefit. However, the federal SALT cap can limit how much state and local tax actually counts.

In Texas, there is no state income tax, but property taxes can be substantial. A Texas homeowner may still itemize if property taxes, mortgage interest, and charitable donations together exceed the standard deduction. The key difference is that the combined federal-plus-state tax rate may be lower because there is no state income tax to add to the calculation.

Bottom line: a high-tax state does not automatically mean a bigger mortgage tax break, and a no-income-tax state does not mean there is no deduction value. The real answer depends on your marginal tax rate, property tax, other deductions, loan size, and whether you itemize.

Expert Commentary: Are Mortgage Points Worth It for the Tax Deduction?

Many borrowers hear that paying points can reduce taxable income, but the tax deduction should not be the main reason to buy points. Points are prepaid interest. You pay more upfront in exchange for a lower mortgage rate. The real question is not “Can I deduct the points?” but “Will the lower monthly payment recover my upfront cost before I sell, refinance, or pay off the loan?”

The key number is the break-even point:

Break-even months = Cost of points ÷ Monthly payment savings

For example, if one point costs $4,000 and reduces your monthly payment by $80, the break-even point is:

$4,000 ÷ $80 = 50 months

That means you need to keep the mortgage for a little over four years before the points start to work in your favor. If you refinance or sell before that, paying points may have been a bad trade, even if you received some tax benefit.

Practical Rule

If the break-even point is within the first three to five years and you are confident you will keep the loan beyond that period, buying points can make sense. If the break-even point is seven years or longer, I would be cautious unless the rate reduction is unusually strong or you are highly certain you will hold the loan long term.

Common Pitfall

Do not treat the points deduction as “free money.” A tax deduction only reduces taxable income; it does not refund the full amount you paid. If your combined marginal tax rate is 30%, a $4,000 deductible point payment may reduce taxes by about $1,200, not $4,000. You still paid the remaining economic cost.

The smartest approach is to compare three numbers together: the upfront point cost, the monthly payment reduction, and the realistic tax benefit after the standard deduction test.

What Formulas Does This Calculator Use?

This calculator uses a simplified combined marginal tax rate:

Combined Tax Rate = Federal Tax Rate + State Tax Rate × (1 − Federal Tax Rate)

Example: if your federal tax rate is 24% and your state tax rate is 8%, the combined rate is:

24% + 8% × (1 − 24%) = 30.08%

Mortgage Interest Deduction Limit

For qualified residential mortgage debt, interest is generally deductible only on up to $750,000 of loan principal, or $375,000 if married filing separately.

If the mortgage balance is within the deductible limit, the calculator estimates tax savings as:

Mortgage Interest × Combined Tax Rate

If the mortgage balance is above the deductible limit, only the interest attributable to the deductible portion of the loan is counted.

Deductible Interest = Monthly Interest × Deductible Loan Limit ÷ Current Loan Balance

Points Paid

Points are treated as prepaid interest in this calculator. For simplified planning, the calculator includes points in the first-year mortgage deduction estimate.

First-Year Mortgage Deduction = First-Year Interest + Points Paid

Standard Deduction Test

The calculator then checks whether your mortgage deduction actually helps you itemize:

Itemized Without Mortgage = Other Itemized Deductions Itemized With Mortgage = Other Itemized Deductions + Mortgage Interest + Points Usable Mortgage Deduction = max(Standard Deduction, Itemized With Mortgage) − max(Standard Deduction, Itemized Without Mortgage)

The estimated real tax savings are:

Estimated Real Tax Savings = Usable Mortgage Deduction × Combined Tax Rate

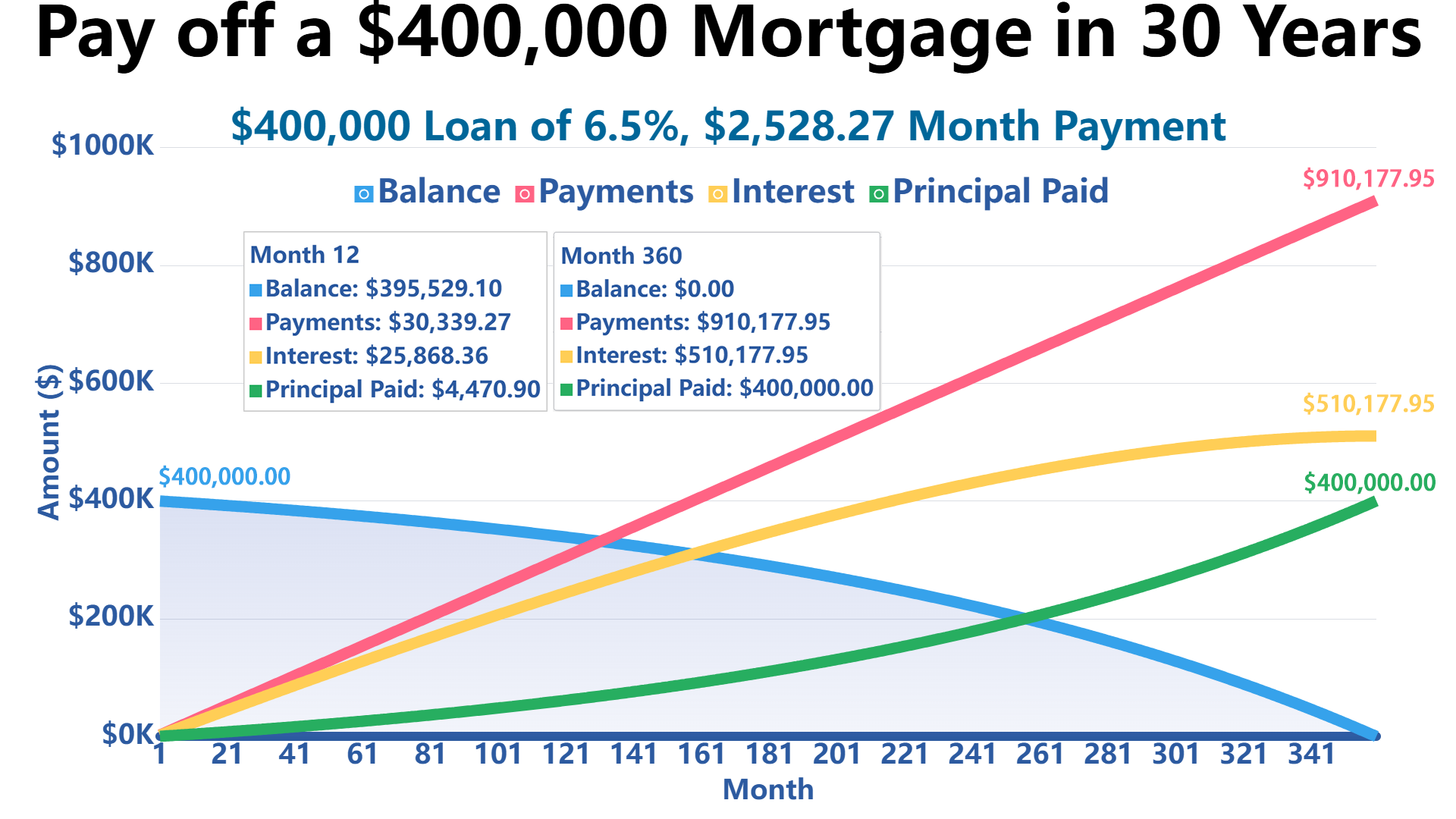

How Much Your Mortgage Payments Could Reduce Your Income Taxes?

Let’s say you:

- Loan Amount: $400,000

- Annual Interest Rate: 6.5%

- Loan Term: 30 years

- Federal Tax Rate: 24 %

- State Tax Rate: 8%

- Origination Fee: 1%

- Points Paid: 1

- Other Fees: $1,000

The total interest paid in the first year was $25,868.36. You also paid $4,000.00 for one discount point. Based on a combined state and federal tax rate of 30.08%, your tax savings in the first year amount to $8,984.40. Over the 30-year loan term, you will save an average of $5,155.49 in taxes per year, for a total tax savings of $154,664.73.

References

- IRS — Home Mortgage Interest Deduction (Publication 936): https://www.irs.gov/publications/p936

- IRS — Topic No. 505, Tax Withholding and Estimated Tax (general guidance on marginal rates): https://www.irs.gov/taxtopics/tc505

Write Reply to This Calculator