FHA Loan Calculator

Calculate Monthly Payments & Mortgage Insurance (MIP) for FHA loans.

FHA Loan Calculator

Calculation Results

| Item | Monthly | Total |

|---|---|---|

| Mortgage Payment | ||

| Property Tax | ||

| Home Insurance | ||

| Annual FHA MIP | ||

| HOA Fee | ||

| Other Costs | ||

| Total Buyer Costs |

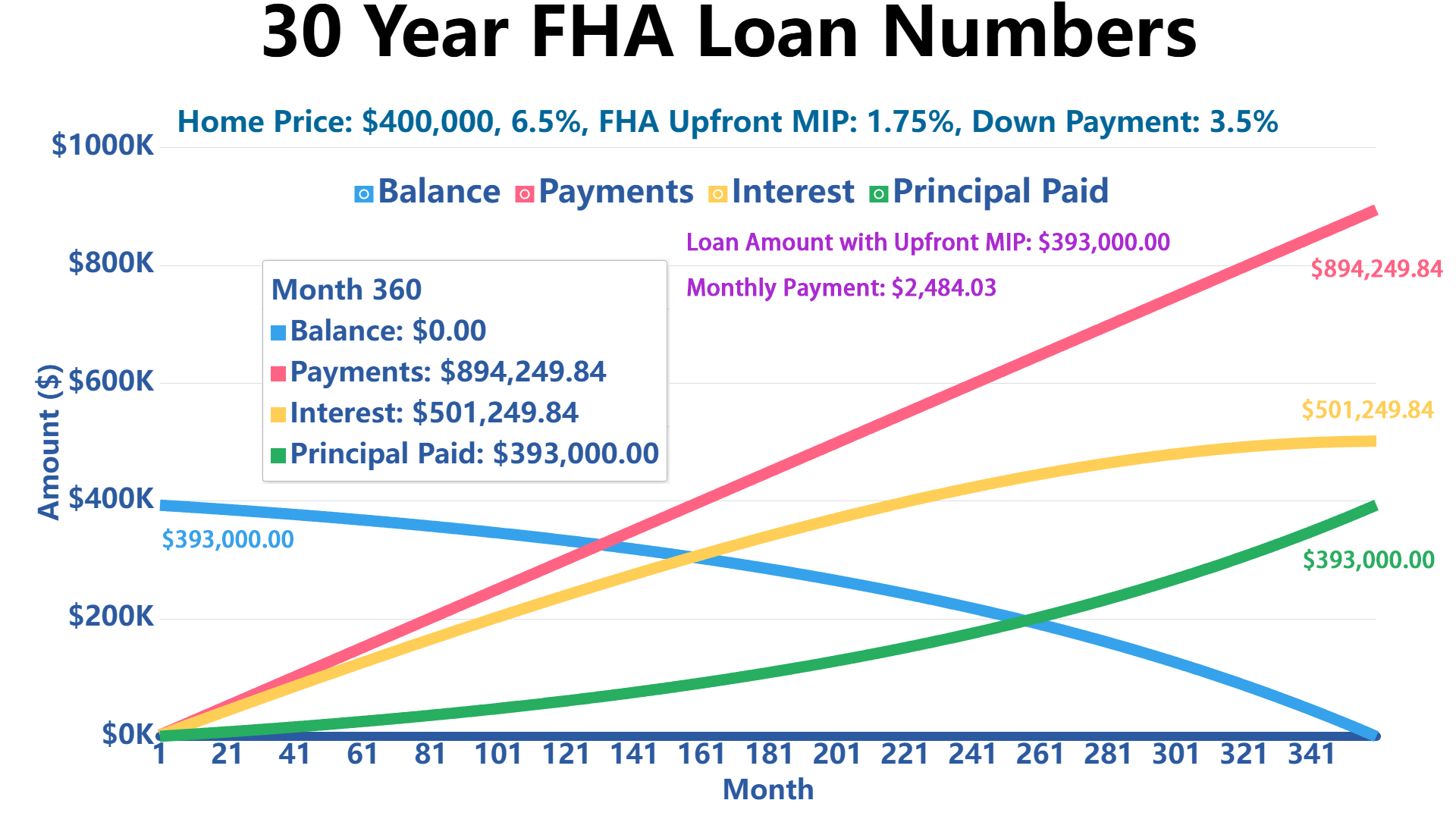

Payment Schedule Visualization

Payment Amortization Table

| Year | Date | Interest | Principal | Payment | Ending Balance | Cumulative Payment | Cumulative Principal |

|---|

| Month | Date | Interest | Principal | Payment | Ending Balance | Cumulative Payment | Cumulative Principal |

|---|

Real FHA Loan Case Study: Buying a $400,000 Home in Texas in 2026

To make the FHA loan numbers easier to understand, let’s look at a realistic example. Assume “Michael” is a first-time homebuyer in Texas with a 620 credit score. In 2026, he wants to buy a $400,000 single-family home and is comparing an FHA loan with a low-down-payment conventional loan.

| Scenario | FHA Loan | Conventional Loan |

|---|---|---|

| Home Price | $400,000 | $400,000 |

| Down Payment | 3.5% / $14,000 | 3% to 5%, depending on lender program |

| Credit Score | 620 | 620 |

| Mortgage Insurance | Upfront MIP + Annual MIP | Private Mortgage Insurance, usually based on credit score and LTV |

| Typical Advantage | Easier qualification and potentially better approval odds | May be cheaper if credit score is stronger or down payment is larger |

Using this calculator, Michael sees that the FHA loan includes monthly mortgage insurance, but it may still be more accessible because FHA underwriting is often more flexible for borrowers with lower credit scores. In a sample comparison using a 30-year term, a 6.565% FHA interest rate, 0.55% annual FHA MIP, and a hypothetical 7.125% conventional rate with higher PMI, the FHA option could save roughly $10,000 to $14,000 over the first five years. Actual savings depend on the lender, credit profile, PMI rate, taxes, insurance, and whether the borrower refinances later.

This example is for educational purposes only. Always compare official Loan Estimates from multiple lenders before choosing between FHA and conventional financing.

2026 FHA Loan Limits: Why Your County Matters

FHA loan limits are not the same everywhere. They vary by county and property type. A borrower buying a home in a lower-cost county may face a lower maximum FHA loan amount, while buyers in high-cost areas may qualify for a higher limit.

For calendar year 2026, the basic standard FHA forward mortgage limits are:

| Property Type | 2026 FHA Forward Basic Limit | 2026 FHA High-Cost Ceiling |

|---|---|---|

| One-family | $541,287 | $1,249,125 |

| Two-family | $693,050 | $1,599,375 |

| Three-family | $837,700 | $1,933,200 |

| Four-family | $1,041,125 | $2,402,625 |

The FHA high-cost area limits are based on a ceiling tied to the Freddie Mac loan limits. In expensive housing markets, the FHA loan limit can be significantly higher than the basic standard limit.

For comparison, the 2026 Fannie Mae and Freddie Mac baseline conforming limits are:

| Property Type | 2026 Fannie/Freddie Basic Limit | 2026 High-Cost Ceiling |

|---|---|---|

| One-family | $832,750 | $1,249,125 |

| Two-family | $1,066,250 | $1,599,375 |

| Three-family | $1,288,800 | $1,933,200 |

| Four-family | $1,601,750 | $2,402,625 |

Before applying, check the FHA loan limit for the specific county where the property is located. A $400,000 home may be eligible in many counties, but higher-priced homes can exceed the FHA limit in some areas.

When Does FHA Mortgage Insurance Automatically Cancel?

FHA mortgage insurance premium rules are different from conventional PMI rules. With a conventional loan, PMI can often be removed once the borrower reaches enough equity. FHA annual MIP is usually harder to remove.

| FHA Down Payment / Original LTV | Annual MIP Duration | How It Can Be Removed |

|---|---|---|

| Less than 10% down | Usually for the life of the loan | Typically removed only by refinancing into a conventional loan |

| 10% down or more | Usually 11 years | Ends after the required MIP period if the loan remains eligible |

| Refinance into conventional loan | FHA MIP ends when FHA loan is paid off | Possible if the borrower qualifies and has enough equity |

For example, if you buy a home with the minimum 3.5% FHA down payment, your annual MIP will generally last for the entire FHA loan term. If home values rise or you pay down enough principal, you may be able to refinance into a conventional mortgage later and remove FHA MIP.

In a short 5-year FHA loan, the MIP may last for the entire loan. In a typical 30-year FHA loan with less than 10% down, the MIP usually also lasts for the full 30 years unless the borrower refinances.

Can I Put 20% Down on FHA?

Yes, you can put 20% down on an FHA loan.

However, it’s important to know:

- The minimum down payment for an FHA loan is typically 3.5% if your credit score is 580 or higher.

- Putting 20% down or more on an FHA loan is allowed, but many borrowers choose FHA because of the low down payment requirement.

- If you put 20% down (or more), you may not have to pay the monthly mortgage insurance premium (MIP) for the life of the loan, depending on the loan terms.

- In some cases, putting 20% down on an FHA loan may offer limited advantage compared to conventional loans, which often do not require mortgage insurance with 20% down.

If you plan to put 20% down, you might also consider a conventional loan as an alternative, since it might be more cost-effective at higher down payment levels.

How to Reduce or Cover the FHA Down Payment in 2026

FHA loans generally require a minimum 3.5% down payment if your credit score is 580 or higher. You usually cannot get a true zero-down FHA loan, but you may be able to reduce or cover the down payment using approved assistance sources.

Common ways to cover the FHA down payment include:

- State Housing Finance Agency programs: Many states offer down payment assistance through their Housing Finance Agency. Examples include the California Housing Finance Agency (CalHFA), Texas State Affordable Housing Corporation (TSAHC), Florida Housing Finance Corporation (Florida Housing), and New York State Mortgage Agency (SONYMA).

- Local city or county DPA grants: Some counties and cities offer grants or forgivable second mortgages for first-time homebuyers, teachers, police officers, firefighters, healthcare workers, and moderate-income households.

- Gift funds: FHA allows eligible gift funds from family members, employers, labor unions, charitable organizations, or approved government programs, as long as the funds are properly documented.

- Employer-assisted housing programs: Some employers offer homebuyer assistance, closing cost support, or matching funds for eligible employees.

Down payment assistance rules vary by state, county, income limit, purchase price, and lender. Always confirm that the assistance program is compatible with FHA financing.

Does Everyone Get Approved for FHA?

No. FHA loans are easier to qualify for than many conventional loans, but approval is not automatic. Borrowers still need to meet credit, income, debt-to-income, property, and documentation requirements.

Typical FHA qualification guidelines include:

- Credit score: 580 or higher for a 3.5% down payment. Borrowers with scores from 500 to 579 may need at least 10% down.

- Front-end DTI: Housing payment is commonly expected to be around 31% or less of gross monthly income.

- Back-end DTI: Total monthly debt payments are commonly expected to be around 43% or less of gross monthly income.

- Possible flexibility: Some lenders may allow higher DTI ratios if the borrower has compensating factors, such as strong reserves, stable employment, or a stronger credit history.

- Property standards: The home must meet FHA minimum property requirements and pass an FHA appraisal.

- Documentation: Borrowers usually need income verification, tax documents, bank statements, employment history, and proof of funds.

Final approval depends on the lender’s underwriting standards as well as FHA rules.

FHA Loan vs. Conventional Loan: Which Costs Less?

FHA loans can be a strong option for borrowers with lower credit scores or limited cash for a down payment. However, conventional loans may become more cost-effective when the borrower has stronger credit, a larger down payment, or enough equity to remove PMI.

| Feature | FHA Loan | Conventional Loan |

|---|---|---|

| Minimum Down Payment | 3.5% with 580+ credit score | Often 3% to 5%, depending on program |

| Credit Flexibility | More flexible for lower credit scores | Usually better for stronger credit profiles |

| Mortgage Insurance | Upfront MIP + annual MIP | PMI if down payment is below 20% |

| Mortgage Insurance Cancellation | Often lasts for the life of the loan if less than 10% down | PMI may be removable after reaching sufficient equity |

| Best For | Borrowers with lower credit scores or limited savings | Borrowers with stronger credit or larger down payments |

| 20% Down Payment Scenario | Allowed, but FHA MIP may still apply depending on terms | Often better because PMI is usually not required |

If you can put 20% down and qualify for a competitive conventional rate, a conventional loan may have lower total costs. If your credit score is lower or your savings are limited, FHA may provide a more realistic path to approval.

Quick FHA vs. Conventional Cost Comparison

| Item | FHA Loan | Conventional Loan |

|---|---|---|

| Estimated Monthly Principal & Interest | ||

| Estimated Monthly Mortgage Insurance | ||

| Estimated Monthly Total | ||

| Estimated First 5-Year Cost | ||

| Estimated Difference Over 5 Years | ||

FQAs

Who Is an FHA Loan Best for?

An FHA loan is best for borrowers with lower credit scores, limited savings for a down payment (first-time homebuyers), and those seeking easier qualification requirements.

What Is the Downside to an FHA Loan?

The downside to an FHA loan is the requirement to pay both upfront and ongoing mortgage insurance premiums, which can increase the overall loan cost.

Do FHA Loans Have Higher Interest Rates?

FHA loans often have slightly higher interest rates compared to conventional loans because of the added mortgage insurance and government backing, but this can vary based on your credit profile and market conditions.

What Would the Minimum Down Payment Be for an FHA Loan of $400,000?

You may qualify with as little as 3.5% down. $400,000 x 3.5% = $14,000.

What Do You Need for a FHA Loan 2026?

For an FHA loan in 2026, you need a minimum 3.5% down payment, a credit score of at least 580 (or 500–579 with a 10% down payment), steady income, acceptable debt-to-income ratio, and required financial documents.

References

For official FHA information and current rates, please visit:

- U.S. Department of Housing and Urban Development (HUD)

- Federal Housing Administration (FHA)

- FHA Mortgage Insurance Premiums - HUD.gov

- Consumer Financial Protection Bureau - Home Buying

Write Reply to This Calculator