Debt Payoff Calculator

Estimate your debt payoff timeline, total interest, and month-by-month repayment schedule using the Debt Avalanche Method, fixed payment rollovers, and extra monthly or one-time contributions.

Debt Payoff Calculator

Calculation Results

| Month | Principal | Interest | Payment | Ending Balance | Cumulative Principal | Cumulative Interest | Cumulative Payment |

|---|

How to Use the Debt Avalanche Method Without Losing Motivation

The debt avalanche method is simple in theory: pay the minimum amount on every debt, then put all extra money toward the debt with the highest interest rate. Once that debt is gone, move the freed-up payment to the next highest-rate debt.

Mathematically, this is usually the most efficient repayment strategy because it attacks the debt that is charging you the most interest first. However, in real life, debt payoff is not only a math problem. It is also a behavior problem.

Many borrowers start with strong motivation but lose momentum after a few months because the highest-interest debt is not always the smallest balance. This means visible progress can feel slow at first. That is why the setting “Maintain a fixed total monthly payment amount?” matters.

When this option is turned on, the calculator assumes that after one debt is paid off, you keep paying the same total monthly amount instead of reducing your payment. Psychologically, this creates a powerful habit loop: your monthly budget stays familiar, but more of each payment begins attacking principal instead of interest.

In other words, the avalanche method gives you the best mathematical target, while a fixed total payment helps you stay consistent long enough to benefit from it.

Scenario-based debt avalanche example

Imagine a borrower who has a mix of credit card debt, an auto loan, a boat loan, and a mortgage. Their instinct may be to pay off the smallest debt first because it feels easier. But if the highest APR account is left untouched, interest keeps accumulating in the background.

This is where the calculator helps turn an emotional decision into a visible plan. By comparing the payoff timeline with and without extra payments, the borrower can see how much time and interest can be saved by staying focused on the highest-cost debt first.

Assume the borrower has the following debts:

- Auto Loan: $35,000 balance at 5.9% APR, with a $500 minimum payment.

- Home Mortgage: $250,000 balance at 4.5% APR, with a $2,000 minimum payment.

- Boat Loan: $7,000 balance at 5.9% APR, with a $150 minimum payment.

- Credit Card: $8,500 balance at 20.9% APR, with an $80 minimum payment.

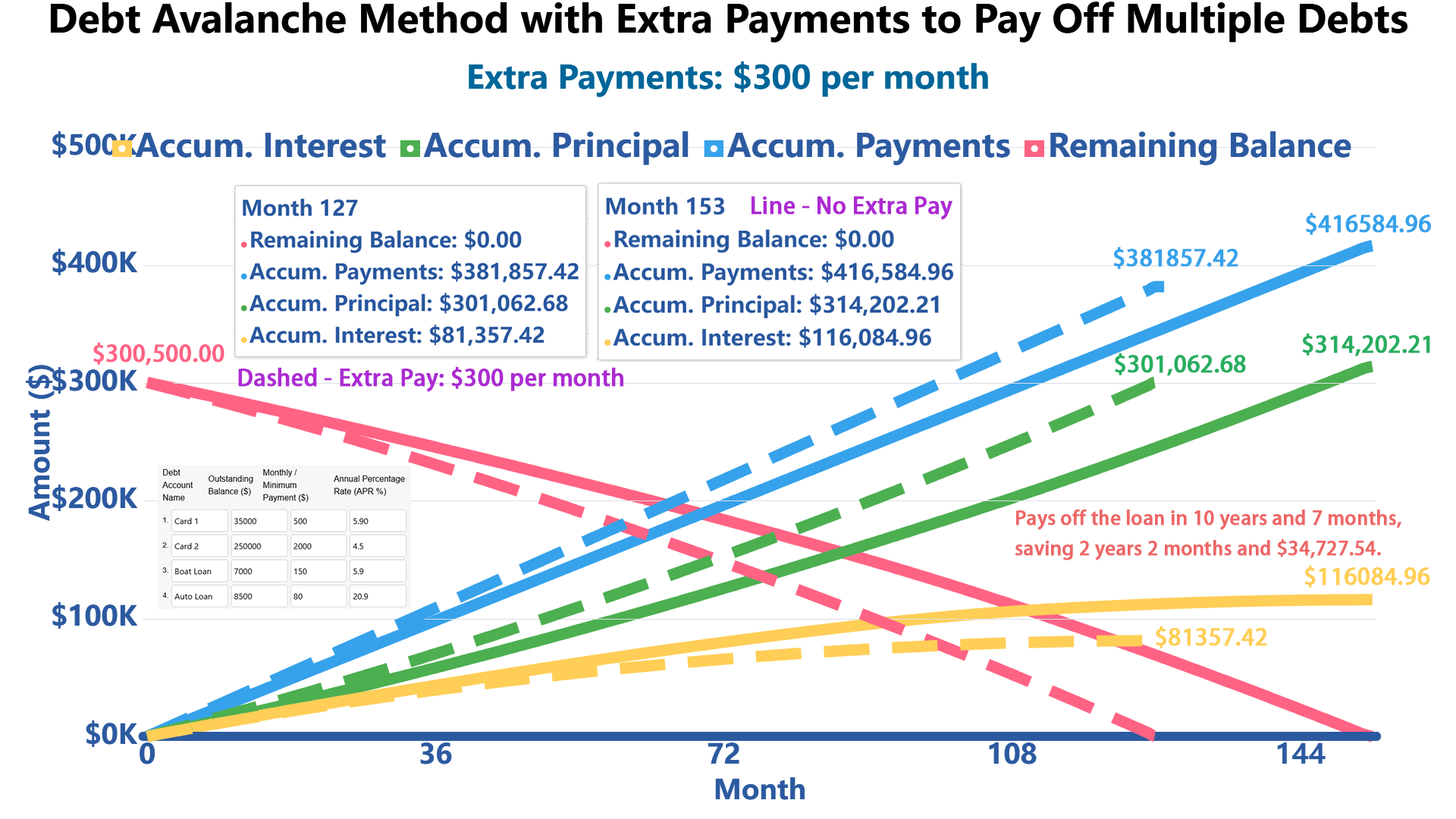

With only the fixed monthly or minimum payments, this debt portfolio would be fully repaid in 153 months, or 12 years and 9 months. The total amount paid would be $416,584.96, including $116,084.96 in interest charges.

This baseline result is important because it shows the hidden cost of slow repayment. Even when every account is being paid on time, high-interest balances can keep generating interest for years.

| Debt | Payoff Duration | Total Interest Paid ($) | Total Amount Paid ($) | Payment Schedule |

|---|---|---|---|---|

| #4: Credit card | 113 months (9 years and 5 months) | $2,2457.05 | $30,957.05 | Pay $80.00 until month 53. Then Pay $208.59 until month 54. Then Pay $230.00 until month 86. Then Pay $724.76 until month 87. Then Pay $730.00 until month 112. Then Pay $173.71 at month 113 to payoff. |

| #1: Auto Loan | 87 months (7 years and 3 months) | $8,005.24 | $43,005.24 | Pay $500.00 until month 86. Then Pay $5.24 at month 87 to payoff. |

| #3: Boat Loan | 54 months (4 years and 6 months) | $971.41 | $7,971.41 | Pay $150.00 until month 53. Then Pay $21.41 at month 54 to payoff. |

| #2: Home mortgage | 153 months (12 years and 9 months) | $84,651.25 | $334,651.25 | Pay $2,000.00 until month 112. Then Pay $2,556.29 until month 113. Then Pay $2,730.00 until month 152. Then Pay $1,624.96 at month 153 to payoff. |

What Changes If You Add $300 Per Month?

When the borrower adds $300 per month and keeps the total monthly payment fixed, the portfolio is repaid in 127 months, or 10 years and 7 months. Total payments fall to $381,857.42, including $81,357.42 in interest charges.

That means the extra payment strategy saves about 26 months and approximately $34,727.54 in interest compared with the minimum-payment baseline. The key is not just paying extra, but keeping that extra amount focused on the highest-interest debt first.

| Debt | Payoff Duration | Total Interest Paid ($) | Total Amount Paid ($) | Payment Schedule |

|---|---|---|---|---|

| #4: Credit card | 29 months (2 years and 5 months) | $2,364.06 | $10,864.06 | Pay $380.00 until month 28. Then Pay $224.06 at month 29 to payoff. |

| #1: Auto Loan | 59 months (4 years and 11 months) | $6,231.29 | $41,231.29 | Pay $500.00 until month 28. Then Pay $655.94 until month 29. Then Pay $880.00 until month 53. Then Pay $1,008.59 until month 54. Then Pay $1,030.00 until month 58. Then Pay $326.77 at month 59 to payoff. |

| #3: Boat Loan | 54 months (4 years and 6 months) | $971.41 | $7,971.41 | Pay $150.00 until month 53. Then Pay $21.41 at month 54 to payoff. |

| #2: Home mortgage | 127 months (10 years and 7 months) | $71,790.65 | $321,790.65 | Pay $2,000.00 until month 58. Then Pay $2,703.23 until month 59. Then Pay $3,030.00 until month 126. Then Pay $77.42 at month 127 to payoff. |

Real Case Study: How Extra Payments Changed the Payoff Timeline

To make this calculator more practical, we reviewed three real-world debt payoff scenarios from borrowers with different debt profiles. Each person used the calculator to test how additional monthly payments, annual lump-sum contributions, and fixed total payments could change their payoff timeline.

Across these three cases, the users reduced their estimated payoff timeline by an average of 14 months after adjusting their extra payment strategy and keeping their total monthly payment consistent after each debt was paid off.

| Borrower Profile | Original Situation | Calculator Adjustment | Observed Result | Practical Lesson |

|---|---|---|---|---|

| Credit Card Heavy Borrower | Multiple cards above 20% APR, mostly making minimum payments. | Added $150 per month and targeted the highest APR card first. | Estimated payoff moved forward by 11 months. | Small monthly increases can matter when aimed at high-interest debt. |

| Auto Loan and Card Mix | Auto loan and credit card balances both carried high APRs. | Used a tax refund as a Month 6 one-time contribution. | Estimated total interest dropped significantly compared with minimum-only repayment. | Lump-sum payments are more effective when made earlier in the payoff journey. |

| Family Budget Borrower | Had enough income to pay extra but often reduced payments after one account was cleared. | Turned on “Maintain a fixed total monthly payment amount.” | Estimated payoff accelerated by 16 months. | Keeping the same monthly payment creates momentum and prevents lifestyle creep. |

Their most common feedback was that the calculator made the debt payoff process feel less abstract. Instead of only seeing a balance, they could see the month-by-month effect of each extra payment decision.

Common Mistakes They Reported

- Spreading extra payments too thinly. Paying a little extra on every account felt balanced, but it slowed down progress on the highest-interest debt.

- Stopping the rollover effect. After paying off one debt, some borrowers were tempted to lower their monthly payments instead of rolling the amount into the next debt.

- Waiting too long to use lump-sum cash. A bonus or refund used earlier usually reduced more future interest than the same payment made later.

References

Government Resources:

- Consumer.gov - Paying Off Debt - Official U.S. government guidance on debt management strategies

- Consumer Financial Protection Bureau (CFPB) - Credit Card Debt Strategies - Federal guidance on debt repayment methods

- FDIC Money Smart - Credit and Debt - Federal Deposit Insurance Corporation educational materials

- USA.gov - Dealing with Debt - Official U.S. government portal for debt management information

Educational Institutions:

- University of Missouri Extension - Debt Management Strategies

- Penn State Extension - Avalanche vs Snowball Approach

Write Reply to This Calculator