Mortgage Calculator

Estimate your monthly mortgage payment and total out-of-pocket costs, including PMI, property taxes, homeowners insurance, and HOA fees.

Mortgage Calculator

Calculation Results

| Item | Monthly | Total |

|---|---|---|

| Mortgage Payment | ||

| Property Tax | ||

| Home Insurance | ||

| PMI | ||

| HOA Fee | ||

| Other Costs | ||

| Total Out-of-Pocket | With PMI: After PMI: |

If Biweekly Repayment without Additional Payments

Payment Visualization

Amortization Table

| Year | Date | Payments | Principal | Interest | End Balance | Total OOP |

|---|

| Month | Date | Payments | Principal | Interest | End Balance |

|---|

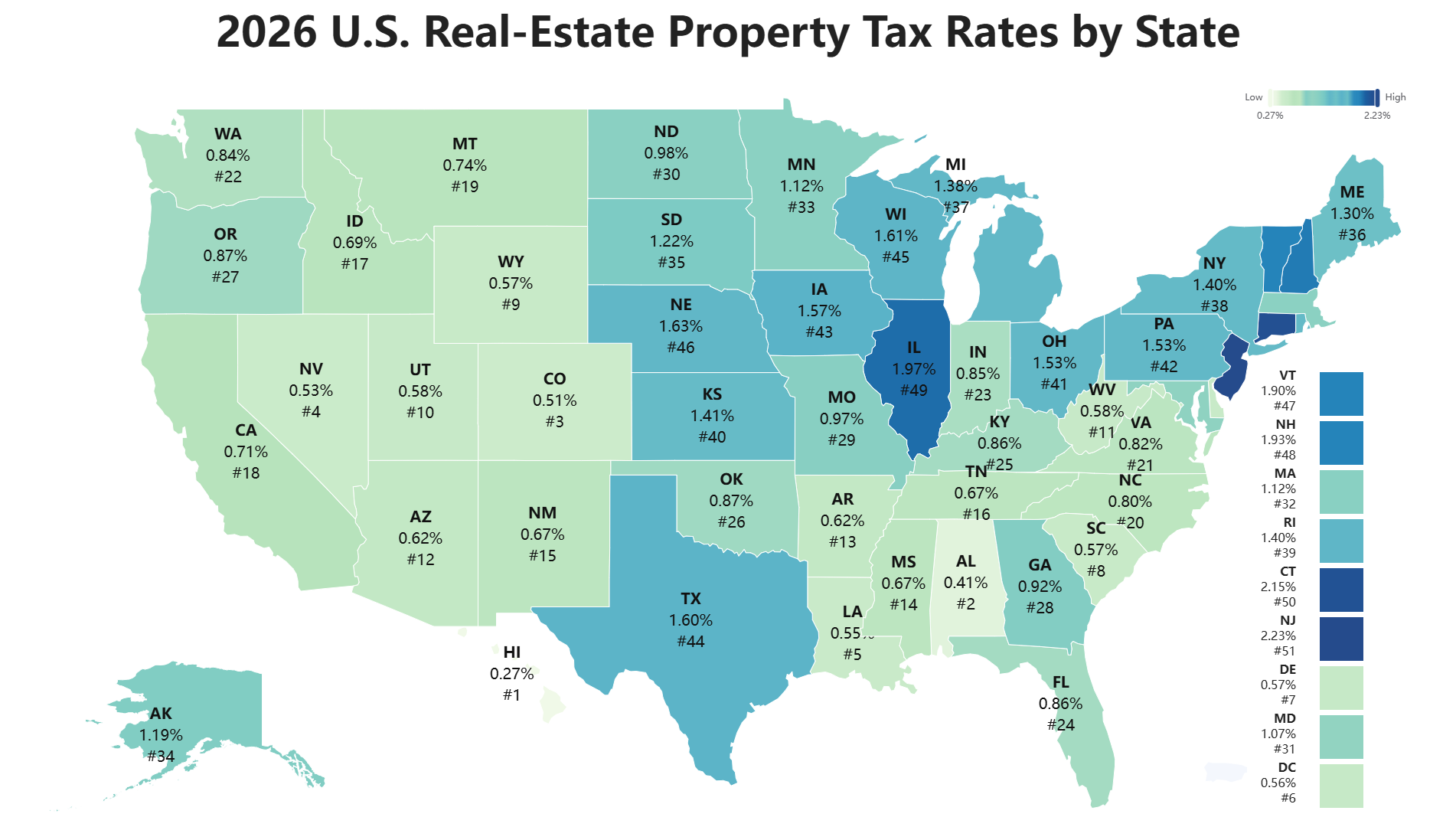

Average Property Tax Rates by State: 50 States + DC

The table below provides a planning-level comparison of average property tax rates, median home values, estimated median annual property taxes, and common homestead exemptions or tax relief rules. These figures should be used as a starting point, not as a substitute for county-level tax verification.

| # | State | Tax Rate | Median Home Value | Median Annual Tax |

|---|---|---|---|---|

| 1 | Hawaii | 0.27% | $722,500 | $1,951 |

| 2 | Alabama | 0.41% | $179,500 | $734 |

| 3 | Colorado | 0.51% | $488,600 | $2,492 |

| 4 | Nevada | 0.53% | $410,100 | $2,174 |

| 5 | Louisiana | 0.55% | $198,300 | $1,091 |

| 6 | District of Columbia | 0.56% | $635,900 | $3,561 |

| 7 | Delaware | 0.57% | $305,200 | $1,740 |

| 8 | South Carolina | 0.57% | $239,800 | $1,367 |

| 9 | Wyoming | 0.57% | $294,600 | $1,679 |

| 10 | Utah | 0.58% | $443,400 | $2,572 |

| 11 | West Virginia | 0.58% | $145,000 | $841 |

| 12 | Arizona | 0.62% | $349,300 | $2,166 |

| 13 | Arkansas | 0.62% | $162,800 | $1,009 |

| 14 | Mississippi | 0.67% | $140,200 | $939 |

| 15 | New Mexico | 0.67% | $259,900 | $1,741 |

| 16 | Tennessee | 0.67% | $260,800 | $1,748 |

| 17 | Idaho | 0.69% | $359,900 | $2,483 |

| 18 | California | 0.71% | $659,300 | $4,681 |

| 19 | Montana | 0.74% | $366,600 | $2,713 |

| 20 | North Carolina | 0.80% | $288,200 | $2,306 |

| 21 | Virginia | 0.82% | $370,800 | $3,040 |

| 22 | Washington | 0.84% | $504,500 | $4,238 |

| 23 | Indiana | 0.85% | $200,100 | $1,701 |

| 24 | Florida | 0.86% | $352,800 | $3,034 |

| 25 | Kentucky | 0.86% | $183,700 | $1,580 |

| 26 | Oklahoma | 0.87% | $177,500 | $1,544 |

| 27 | Oregon | 0.87% | $423,400 | $3,683 |

| 28 | Georgia | 0.92% | $275,800 | $2,537 |

| 29 | Missouri | 0.97% | $214,100 | $2,077 |

| 30 | North Dakota | 0.98% | $232,900 | $2,282 |

| 31 | Maryland | 1.07% | $380,700 | $4,074 |

| 32 | Massachusetts | 1.12% | $524,800 | $5,878 |

| 33 | Minnesota | 1.12% | $305,100 | $3,417 |

| 34 | Alaska | 1.19% | $318,200 | $3,785 |

| 35 | South Dakota | 1.22% | $255,500 | $3,117 |

| 36 | Maine | 1.30% | $273,900 | $3,561 |

| 37 | Michigan | 1.38% | $220,200 | $3,039 |

| 38 | New York | 1.40% | $384,100 | $5,378 |

| 39 | Rhode Island | 1.40% | $368,100 | $5,153 |

| 40 | Kansas | 1.41% | $204,200 | $2,879 |

| 41 | Ohio | 1.53% | $199,400 | $3,051 |

| 42 | Pennsylvania | 1.53% | $243,400 | $3,724 |

| 43 | Iowa | 1.57% | $192,300 | $3,019 |

| 44 | Texas | 1.60% | $290,400 | $4,646 |

| 45 | Wisconsin | 1.61% | $254,000 | $4,090 |

| 46 | Nebraska | 1.63% | $218,600 | $3,563 |

| 47 | Vermont | 1.90% | $288,800 | $5,487 |

| 48 | New Hampshire | 1.93% | $367,100 | $7,085 |

| 49 | Illinois | 1.97% | $240,800 | $4,744 |

| 50 | Connecticut | 2.15% | $339,200 | $7,295 |

| 51 | New Jersey | 2.23% | $418,900 | $9,345 |

How to Use This Mortgage Calculator to Avoid Hidden Homeownership Costs

A mortgage payment is not just principal and interest. In many real-world purchases, the costs that surprise buyers the most are property taxes, homeowners insurance, HOA dues, PMI, repair reserves, and annual cost increases. This calculator is designed to help you estimate the full monthly cash flow of owning a home, not just the loan payment quoted by a lender.

The most important inputs are the home price, down payment, interest rate, loan term, property tax, insurance, PMI, HOA fees, and other recurring costs. For a more realistic estimate, use the “More Optional” section to model annual increases and extra payments. This is especially useful in states where insurance premiums, HOA dues, or property taxes can rise quickly after purchase.

Expert Insight: The “Affordable Mortgage” Can Still Become an Expensive Home

A buyer may qualify for a mortgage based on principal, interest, taxes, and insurance, but that does not mean the home is financially comfortable. HOA special assessments, rising insurance premiums, maintenance reserves, and PMI can add hundreds of dollars per month. Before making an offer, run at least three scenarios: today’s cost, a 10% higher insurance and HOA scenario, and a higher-rate refinance delay scenario.

Real Homeownership Cost Breakdown: A California Buyer Case Study

To illustrate how hidden costs affect cash flow, consider a recent buyer scenario we reviewed in California. The buyer purchased a condo-style property with a fixed-rate mortgage. The advertised mortgage payment looked manageable at first, but HOA dues and repair reserves changed the real monthly budget within the first three years.

| Cost Item | Initial Monthly Cost | Year 3 Monthly Cost |

|---|---|---|

| Principal & Interest | $1,918 | $1,918 |

| Property Tax | $389 | $405 |

| Homeowners Insurance | $125 | $165 |

| HOA Fee | $360 | $475 |

| Repair / Maintenance Reserve | $200 | $300 |

| PMI | $145 | $145 or removed if equity target is reached |

| Total Estimated Monthly Out-of-Pocket | $3,137 | $3,408 before PMI removal |

In this case, the buyer initially focused on the $1,918 mortgage payment. But the true first-year monthly cost was closer to $3,137 after adding taxes, insurance, HOA dues, PMI, and maintenance reserves. By year three, HOA increases and insurance adjustments pushed the estimated cost above $3,400 per month.

The lesson is simple: a fixed-rate mortgage does not mean fixed homeownership costs. Your principal and interest may stay the same, but property taxes, insurance, HOA dues, and repairs can change your monthly cash flow significantly.

Expert Insight: Model HOA and Insurance Inflation Before You Buy

If you are buying a condo, townhouse, or property in a managed community, do not treat HOA dues as a fixed number. Review the HOA budget, reserve study, recent meeting minutes, insurance coverage, and any upcoming special assessments. In high-cost states, a weak HOA reserve can become a major financial risk for owners.

PMI Trap: Why a Small Down Payment Can Cost More Than Expected

Private mortgage insurance, or PMI, is usually required on many conventional loans when the down payment is below 20%. PMI does not reduce your loan balance and does not protect you as the borrower. It protects the lender if you default.

PMI can be reasonable if it allows you to buy sooner and the home fits your long-term budget. However, it becomes a trap when buyers ignore how long it may remain in the payment. If home values flatten or if extra payments are not made, PMI can stay longer than expected.

How to Use This Calculator for PMI Planning

- Enter your down payment as a percentage or dollar amount to see whether your loan-to-value ratio is likely to trigger PMI.

- Add PMI as an annual dollar amount or percentage to estimate the monthly impact.

- Use the extra payment fields to test whether additional principal payments help you reach PMI removal faster.

- Compare your total out-of-pocket cost with and without PMI to see the true cost of a smaller down payment.

Expert Insight: Do Not Judge PMI in Isolation

PMI is not always bad. If home prices are rising quickly and rent is expensive, paying PMI for a limited period may be acceptable. But if your monthly budget is already tight, PMI can reduce your flexibility and make it harder to absorb repairs, insurance increases, or HOA assessments. The safer approach is to calculate the full monthly payment with PMI included, then stress-test the budget with higher taxes and insurance.

15-Year vs. 30-Year Mortgage: Expert Strategy in Today’s Rate Environment

Choosing between a 15-year and 30-year mortgage is not only about the interest rate. It is a cash-flow decision. A 15-year mortgage usually has a lower rate and much lower total interest, but the monthly payment is significantly higher. A 30-year mortgage costs more over time, but it gives the borrower more monthly flexibility.

| Loan Type | Best For | Main Risk |

|---|---|---|

| 15-Year Fixed | Buyers with stable income, strong emergency funds, and a goal of fast debt payoff | Higher monthly payment can create cash-flow pressure |

| 30-Year Fixed | Buyers who want lower required payments and more flexibility | Higher total interest if no extra payments are made |

In a higher-rate environment, many buyers prefer the 30-year mortgage because it protects monthly cash flow. They can then make extra principal payments when income allows. This creates a “30-year required payment, 15- or 20-year payoff goal” strategy.

In a lower-rate environment, a 15-year mortgage can be attractive for borrowers who are confident in their income and have enough liquidity after closing. However, even when rates are low, it is risky to choose a payment that leaves no room for repairs, insurance increases, or job changes.

Expert Insight: Flexibility Has Value

A 30-year loan with disciplined extra payments can sometimes be more practical than a 15-year loan. The reason is optionality. You can pay extra in strong months, but you are not forced into the higher payment during a financial setback. This is especially important for self-employed buyers, commission-based earners, and households expecting major life changes.

When Does Refinancing Make Sense?

Refinancing can reduce your payment or shorten your loan term, but it is not free. Closing costs, lender fees, title fees, appraisal fees, and prepaid expenses can reduce or eliminate the benefit if you sell too soon.

Refinance Checklist

- Rate difference: A refinance is usually more attractive when the new rate is meaningfully lower than your current rate.

- Break-even period: Divide total refinance costs by monthly savings to estimate how many months it takes to recover the cost.

- Loan term reset: Restarting a 30-year loan can lower the payment but may increase lifetime interest if you do not pay extra.

- PMI removal: If your home equity has increased, refinancing may help remove PMI, but compare this against closing costs.

- Time in the home: Refinancing is less useful if you plan to sell before reaching the break-even point.

Expert Insight: Refinance to Improve the Whole Loan, Not Just the Monthly Payment

A lower monthly payment can be misleading if it extends your repayment period too far. The better question is: does the refinance improve your total interest cost, cash-flow safety, or PMI position after accounting for fees? Use this calculator to compare the original loan with a new loan scenario, then evaluate both the monthly savings and the lifetime cost.

Location Matters: Property Taxes and Insurance Vary Widely by State

Property tax is one of the biggest reasons two homes with the same price can have very different monthly payments. A $400,000 home in a low-tax state may have a much lower annual tax bill than a similarly priced home in a high-tax state. Insurance also varies sharply by location, especially in areas exposed to hurricanes, wildfires, floods, hail, or coastal risk.

Before relying on a national average, check the county assessor, local tax authority, insurance quotes, and any homestead exemptions available in the specific state or county where you plan to buy.

Expert Insight: Use State Averages Only as a Starting Point

Statewide property tax averages are useful for early planning, but they can hide major county-level differences. Two homes in the same state may have very different effective tax rates because of school districts, municipal levies, assessment rules, exemptions, and local bond measures. Always verify the actual tax history for the property before making an offer.

Practical Checklist Before You Make an Offer

- Verify the property tax history. Look up the actual tax bill, not just the listing estimate. Ask whether the assessed value may reset after purchase.

- Get insurance quotes early. Do not rely on generic national averages, especially in wildfire, hurricane, flood, or coastal areas.

- Read the HOA documents. Review monthly dues, reserve funds, insurance coverage, litigation, recent increases, and upcoming special assessments.

- Model PMI removal. If your down payment is below 20%, estimate how long PMI may last and whether extra payments could shorten that period.

- Budget for repairs from day one. Even newer homes need maintenance. A repair reserve is not optional; it is part of the real cost of ownership.

- Stress-test your payment. Increase taxes, insurance, HOA, and other costs in the calculator to see whether the home remains affordable.

Example: Why the Same Mortgage Can Feel Different in Two States

Suppose two buyers each purchase a $400,000 home with the same down payment, interest rate, and loan term. Their principal and interest may be nearly identical, but their total monthly cost can differ dramatically because of taxes and insurance.

A buyer in a lower-tax state may have more room for savings, repairs, or extra principal payments. A buyer in a higher-tax state may need to budget several hundred dollars more per month for the same home price. This is why location-specific tax and insurance assumptions are essential when using any mortgage calculator.

Expert Insight: The Best Mortgage Decision Is a Cash-Flow Decision

Buyers often ask, “How much house can I afford?” A better question is, “How much monthly housing cost can I carry while still saving, investing, and handling emergencies?” The safest home purchase leaves room for uncertainty. A calculator should not only confirm that you can buy the home; it should help you understand whether you can comfortably own it.

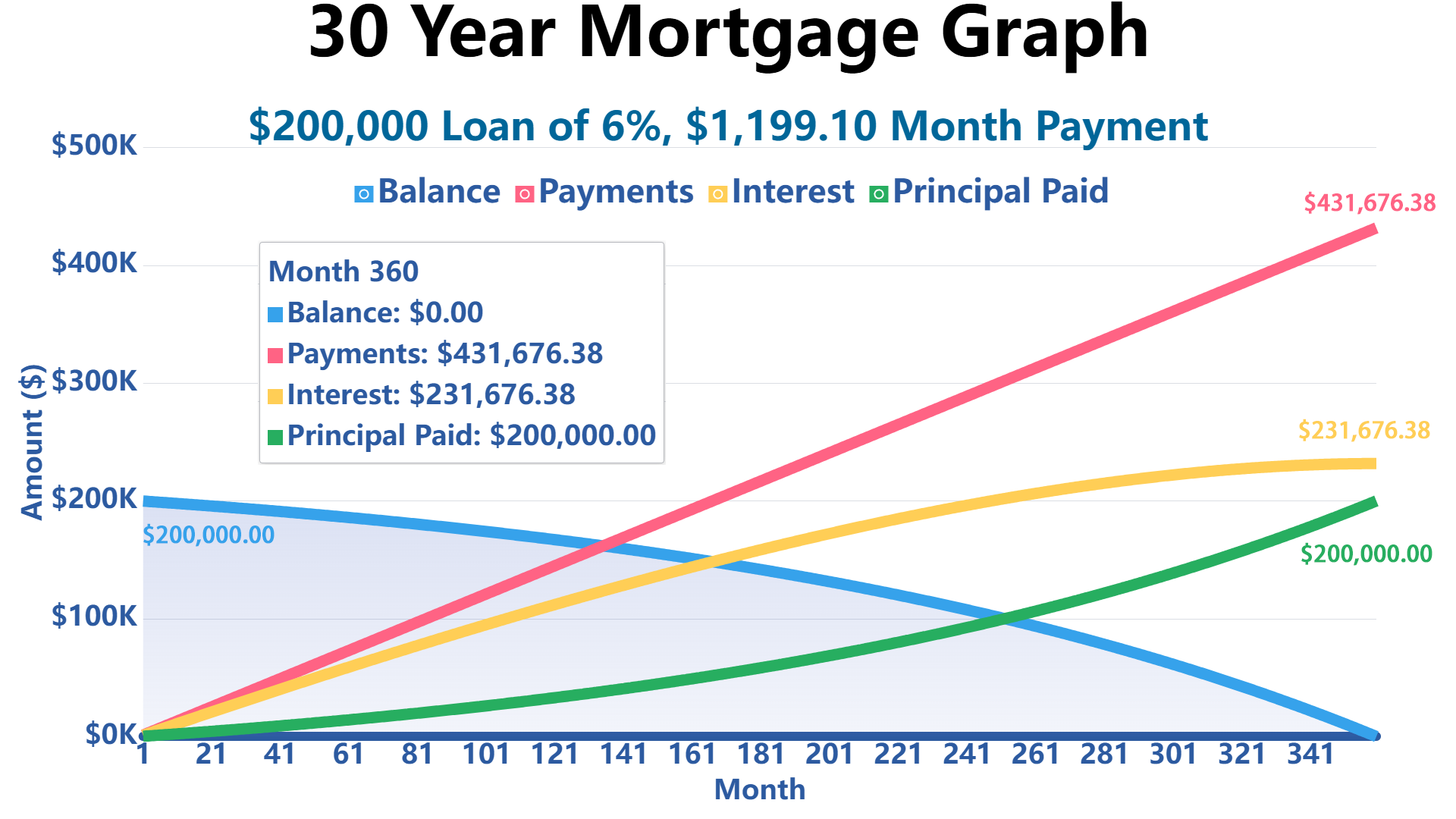

How Much Is $200,000 Mortgage Payment for 30 Years?

Simply put, if you borrow $200,000 for a home at 6% interest over 30 years, you'll pay $1,199.10 each month. That payment covers your principal and interest.

But when you're actually buying a house, there's a lot more to consider. For example:

- Down Payment: 10%

- Property Tax: 1.2%

- Home Insurance: $1,500

- PMI Insurance: $1,000

- HOA Fee: $1,000

- Other Costs: $4,000

When you factor all of these in, your monthly payment jumps to $1904.19. This amount includes principal, interest, insurance, taxes, HOA fees, and other expenses.

So the real cost of homeownership is way more than just the mortgage interest!

References

- Consumer Financial Protection Bureau (CFPB): Official Home Buying Guide

- U.S. Department of Housing and Urban Development: HUD.gov - Housing Information

- Federal Housing Administration: FHA Loan Programs and Requirements

- Fannie Mae: Conventional Loan Guidelines

- Federal Reserve: Mortgage Shopping Tools (PDF)

- IRS Publication 936: Home Mortgage Interest Deduction

Write Reply to This Calculator