Annuity Growth Calculator

Estimate Your Annuity Future Value Based on Regular Deposits

Annuity Growth Calculator

($)

(%)

Years Months

($) per Year

($) per Month

(%) per year

Annuity Value Projection

End Balance

Total Return

Initial Balance

Total Addition Amount

Return from Initial Principal

Return from Addition Amount

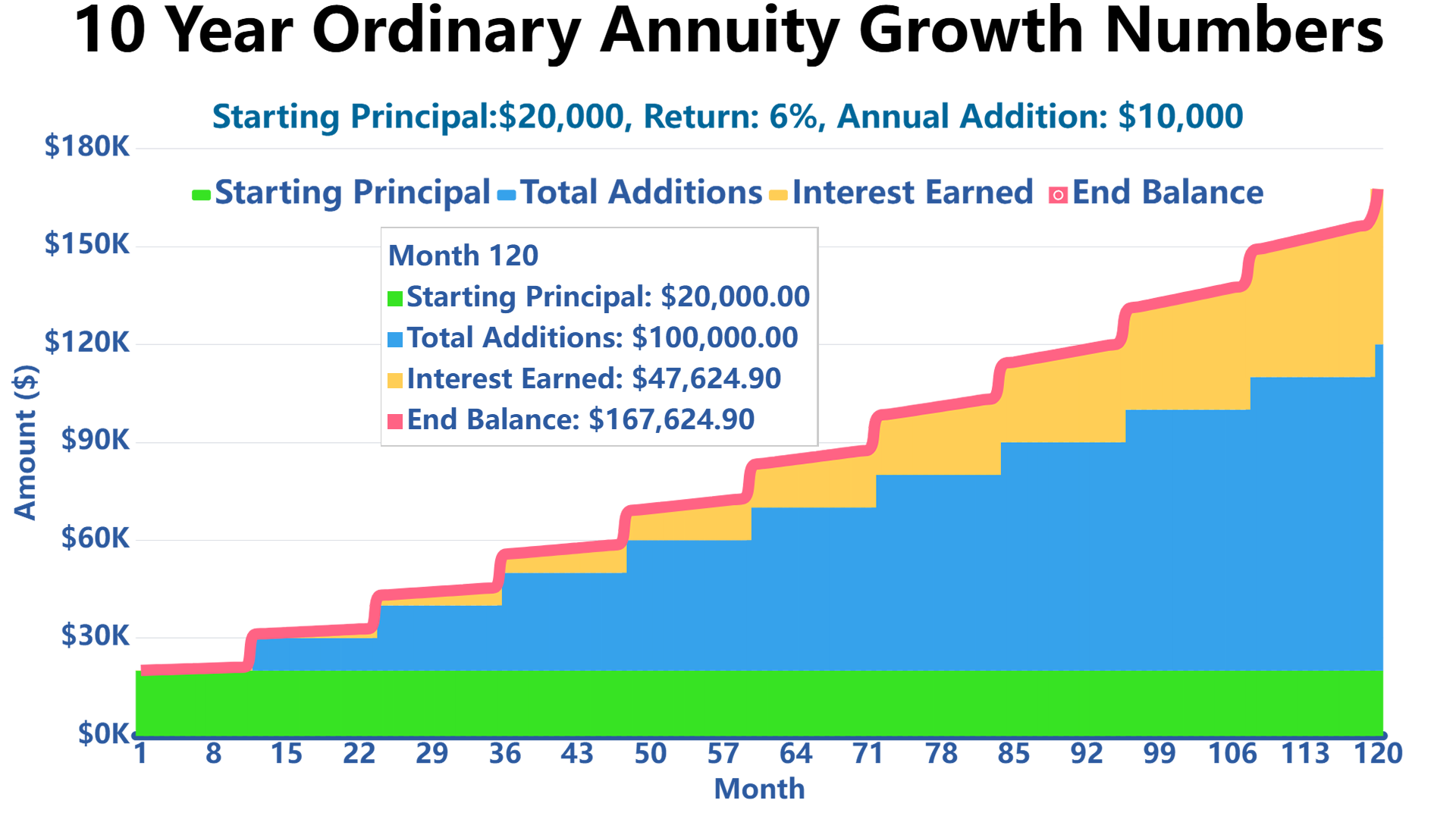

Accumulation Schedule

Accumulation Visualization

References

Government Resources

- SEC - Understanding Annuities

- FINRA - Annuity Investor Information

- Department of Labor - Annuity Guidelines

- IRS - Tax Treatment of Annuities

Professional Guidance

The SEC recommends consulting with qualified financial advisors when considering annuity purchases, as these products can be complex and may not be suitable for all investors.

Related

Write Reply to This Calculator