HELOC Calculator

Calculate Your Home Equity Line of Credit Payments and Costs

HELOC Calculator

Calculation Results

Payment Visualization

Amortization Tables

| Year | Date | Payment | Principal | Interest | Ending Balance |

|---|

| Month | Date | Payment | Principal | Interest | Ending Balance |

|---|

Banker Insight: The HELOC Costs Borrowers Often Miss

From a lender's point of view, most HELOC applicants ask about one thing first: the interest rate. That is understandable, but it is not enough. In actual underwriting and loan setup, several smaller items can quietly raise your holding cost.

One common mistake is ignoring the appraisal fee. Some banks advertise low or no closing costs, but may still require an appraisal, automated valuation, drive-by inspection, title update, flood certification, or recording fee depending on the property and credit line size. If your home value comes in lower than expected, the approved HELOC limit may also be smaller than what you planned.

Another overlooked cost is the inactivity fee. Some lenders charge a fee if you open the HELOC but do not use it, or if there is no activity for a set period. Others charge an annual fee, early closure fee, or require you to keep the account open for a minimum number of years to avoid paying back waived closing costs.

The practical takeaway: before choosing a HELOC, ask the lender for the full fee schedule in writing. Specifically ask about appraisal fees, annual fees, inactivity fees, early termination fees, minimum draw requirements, rate caps, and whether any "no closing cost" offer must be repaid if you close the line early.

HELOC vs Home Equity Loan vs Cash-out Refinance

These three products all let you borrow against home equity, but they behave very differently. The best choice depends on whether you need flexible access to cash, a fixed lump sum, or a full mortgage restructure.

| Feature | HELOC | Home Equity Loan | Cash-out Refinance |

|---|---|---|---|

| Rate Type | Usually variable rate, often Prime + margin | Usually fixed rate | Usually fixed rate |

| Funds Disbursement | Revolving credit line; borrow, repay, and borrow again during the draw period | One-time lump sum | One-time lump sum through a new mortgage |

| Repayment Structure | Draw period may be interest-only; repayment period includes principal and interest | Principal and interest from the beginning | New mortgage payment, often restarted over 15 or 30 years |

| Closing Costs | Can be as low as $0 with some lenders, but fee rules vary | Often 2% to 5% of the loan amount | Often 2% to 5% of the new mortgage amount |

| Flexibility | High; interest is charged only on the amount used | Low; interest applies to the full loan balance | Low; interest applies to the full refinanced mortgage balance |

| Interest Deductibility | Generally limited to qualified home improvement use | Generally limited to qualified home improvement use | Generally limited to qualified home improvement use for the cash-out portion |

| Best For | Renovations, phased projects, flexible cash needs, emergency backup credit | One-time major expenses where fixed payments are preferred | Borrowers who can improve their overall mortgage rate or need to restructure their mortgage |

Editorial view: a HELOC is usually the most flexible option, but flexibility can be dangerous if you treat your home equity like a credit card. A home equity loan is cleaner when you know the exact amount you need. A cash-out refinance only makes sense when the new first mortgage is attractive enough to justify resetting the clock and paying larger closing costs.

LTV and CLTV Limits: How Much Can You Borrow?

The key approval number for a HELOC is usually CLTV, or combined loan-to-value ratio. CLTV compares all debt secured by the home against the home's current value.

The formula is:

CLTV = (Current Mortgage Balance + HELOC Limit) / Home Value x 100%

For example, if your home is worth $500,000 and your current mortgage balance is $300,000, an 80% CLTV limit means total secured debt cannot exceed $400,000. In that case, the maximum HELOC line would be about $100,000 before lender-specific adjustments.

| Home Value | Mortgage Balance | CLTV Limit | Estimated Max HELOC |

|---|---|---|---|

| $500,000 | $300,000 | 80% | $100,000 |

| $500,000 | $300,000 | 85% | $125,000 |

| $500,000 | $300,000 | 90% | $150,000 |

Most lenders cap HELOC CLTV around 80% to 85%. Some may go up to 90%, but usually only for strong borrowers. In practice, borrowers with a FICO score above 720, stable income, low debt-to-income ratio, and a clean property profile are more likely to receive higher CLTV approval and better pricing.

One insider point: the lender may approve you for less than the online estimate if the appraisal comes in low, your first mortgage balance is higher than reported, your debt-to-income ratio is tight, or your property type is considered riskier. Condos, investment properties, rural homes, and properties with title issues may face stricter limits.

Current HELOC Rate Environment: Fixed-rate or Variable-rate HELOC?

Most HELOCs use a variable rate tied to the Prime Rate, plus a lender margin. The margin is the bank's markup based on credit score, CLTV, loan size, occupancy type, and relationship discounts. A strong borrower may receive Prime + 0%, while a weaker file may receive Prime + 1% to Prime + 2% or more.

In a higher-rate environment, variable-rate HELOCs can feel expensive because payments move with benchmark rates. In a falling-rate environment, however, a variable HELOC may become more attractive because your rate can adjust downward without refinancing the entire loan.

A useful way to think about the choice:

- Choose a variable-rate HELOC if you expect to borrow for a short period, plan to pay the balance down aggressively, or believe rates may decline.

- Choose a fixed-rate HELOC option if you are carrying a large balance, need payment certainty, or would struggle if the rate rose by 1% to 2%.

- Split the balance if your lender allows it. Some banks let you lock a portion of the HELOC balance at a fixed rate while keeping the remaining credit line variable.

The banker's view: fixed-rate conversion features are often underused. Borrowers like the flexibility of a HELOC but panic when rates rise. If your lender offers a fixed-rate option, ask about the lock fee, minimum lock amount, maximum number of fixed-rate segments, repayment term, and whether the locked portion can be paid off early without penalty.

Do not choose variable simply because the starting rate is lower. Test the payment at a rate that is 2% higher than today's rate. If that payment breaks your budget, the loan is too aggressive or you should consider a fixed-rate structure.

How HELOC Interest Tax Deduction Works

HELOC interest is not automatically tax deductible. In general, interest may be deductible only when the borrowed funds are used to buy, build, or substantially improve the taxpayer's main home or second home that secures the loan.

That means a HELOC used for a kitchen remodel, bathroom renovation, roof replacement, or home addition may qualify. A HELOC used to pay credit cards, fund a vacation, buy stocks, cover daily expenses, or invest in crypto generally does not qualify for the home mortgage interest deduction.

There are also mortgage debt limits. For many taxpayers, the combined amount of qualifying mortgage debt is limited to $750,000 for married filing jointly or $375,000 for single filers. Interest on debt above the limit may not be deductible.

Practical advice: keep every contractor invoice, receipt, draw request, bank statement, and project contract. If the IRS ever questions the deduction, you need to show that the HELOC funds were used for qualified home improvement. Also remember that the deduction only helps if you itemize deductions. If your itemized deductions are lower than the standard deduction, the HELOC interest may provide no real tax benefit.

When a HELOC Is a Smart Choice

A HELOC can be a strong tool when the borrowing purpose is controlled, the repayment plan is realistic, and the homeowner understands the rate risk.

- Home renovations: HELOCs work well for phased remodeling projects because you can draw money as invoices arrive instead of borrowing the full amount upfront.

- High-interest debt consolidation: Replacing 18% to 25% credit card debt with an 8% to 10% HELOC can reduce interest cost, but only if you stop adding new card debt.

- Short-term bridge financing: A HELOC can help cover temporary cash needs, such as buying before selling or funding a project with expected reimbursement.

- Emergency backup liquidity: An unused HELOC can serve as a last-resort credit line, though you should confirm annual fees or inactivity fees first.

When a HELOC Is a Bad Idea

A HELOC is secured by your home, so it should not be used casually. The worst HELOC decisions usually happen when borrowers convert short-term lifestyle spending into long-term housing debt.

- Speculative investing: Borrowing against your home to buy stocks, crypto, or risky business assets can turn market losses into a housing problem.

- Vacations or luxury spending: A trip ends quickly, but the HELOC balance can follow you for years.

- Unaffordable rate risk: If a 2% rate increase would make the payment uncomfortable, the line is too large or too variable for your budget.

- Near-term home sale plans: A HELOC usually must be paid off when you sell the home, which can reduce your net sale proceeds.

5 Practical Ways to Use a HELOC Without Overpaying

- Borrow only what you need. A $200,000 approval is not a recommendation to use $200,000. Interest is charged on the drawn balance, so smaller draws usually mean lower cost and lower risk.

- Pay principal during the draw period. Interest-only payments are the minimum, not the best strategy. Paying principal early reduces lifetime interest and softens the payment shock when repayment begins.

- Ask about fixed-rate conversion. If you carry a meaningful balance, locking part of it into a fixed rate may protect your budget if benchmark rates rise.

- Keep home improvement records. If you hope to deduct HELOC interest, save contracts, receipts, invoices, and proof of payment.

- Set a rate and payment alert. Know your lifetime rate cap, periodic adjustment cap, and payment trigger point. If the monthly payment crosses your comfort level, consider accelerating repayment or converting to a fixed-rate product.

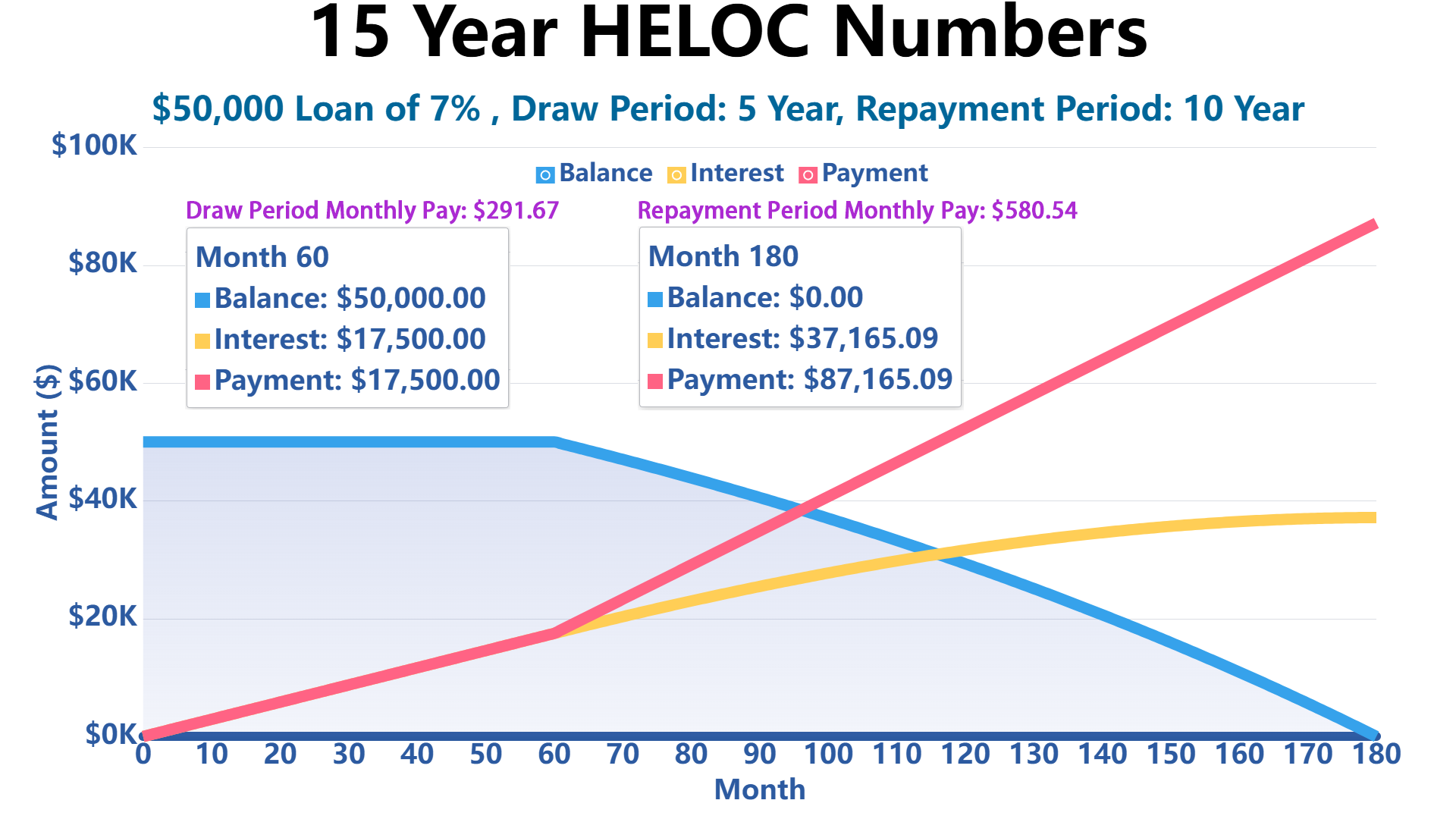

What Is the Monthly Payment on a $50,000 HELOC?

At 7% APR, a $50,000 HELOC has an interest-only payment of about $291.67 per month during the draw period. If the same $50,000 balance is repaid over 10 years with principal and interest, the payment is about $580.54 per month.

The key risk is payment shock. A borrower who gets comfortable paying only $291.67 during the draw period may be surprised when the required payment nearly doubles during repayment. That is why it is smart to test both the draw-period payment and the repayment-period payment before opening the line.

| Interest Rate | Draw Period Payment | Repayment Period Payment 10-year |

|---|---|---|

| 7% | $291.67 | $580.54 |

| 7.5% | $312.50 | $593.51 |

| 8% | $333.33 | $606.64 |

| 8.5% | $354.17 | $619.93 |

| 9% | $375.00 | $633.38 |

| 9.5% | $395.83 | $646.99 |

| 10% | $416.67 | $660.75 |

| 10.5% | $437.50 | $674.67 |

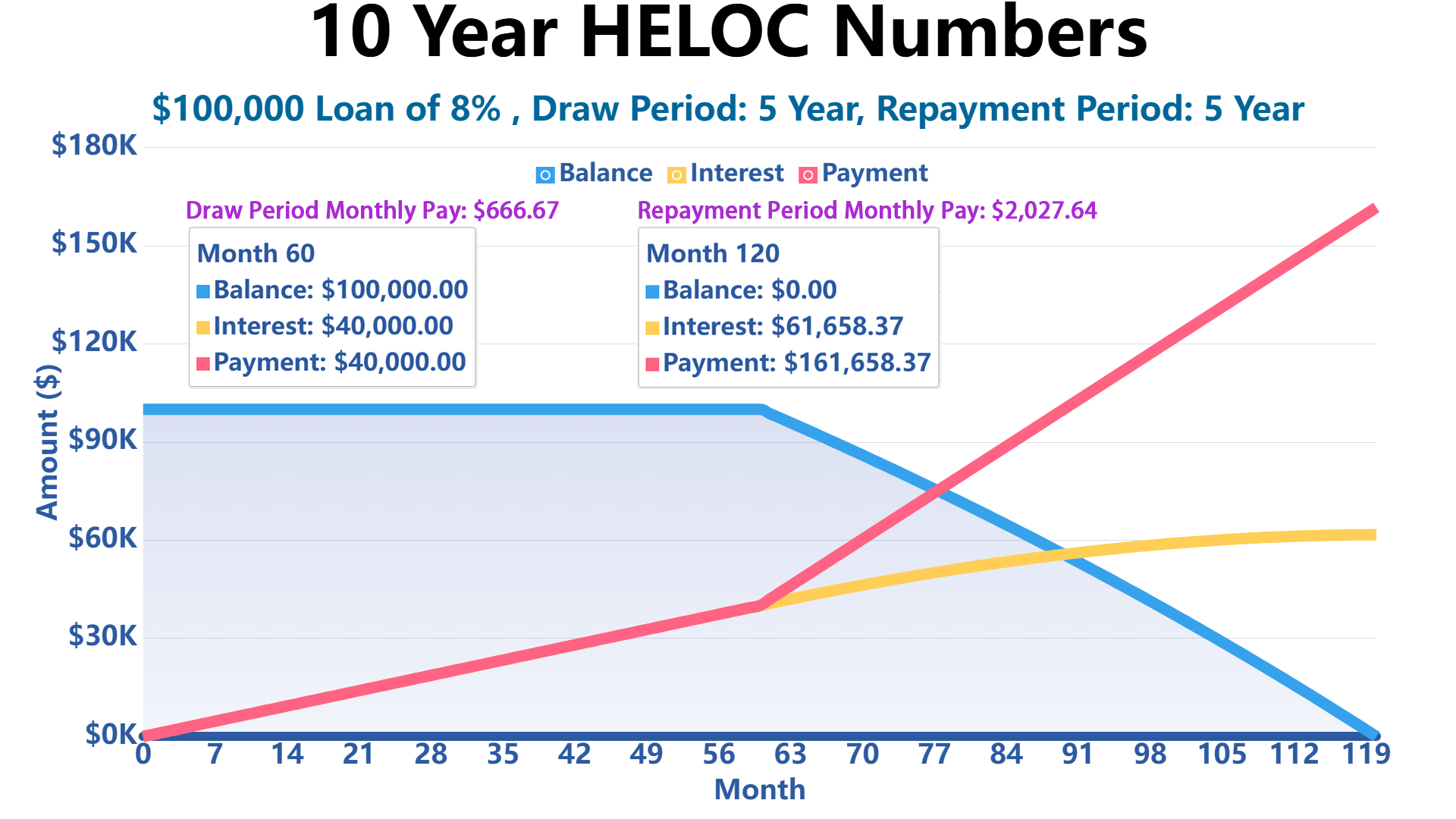

How Much Is the HELOC Payment for $100,000?

At 8% APR, a $100,000 HELOC has an interest-only payment of about $666.67 per month during the draw period. If the same $100,000 balance is repaid over 5 years with principal and interest, the payment is about $2,027.64 per month.

This is where many borrowers underestimate the obligation. A $100,000 HELOC can look manageable during the interest-only phase, but the repayment period can feel like a second mortgage. Before drawing the full line, calculate whether the principal-and-interest payment still fits your budget.

| Interest Rate | Draw Period Payment | Repayment Period Payment 5-year |

|---|---|---|

| 7% | $583.33 | $1,980.12 |

| 7.5% | $625.00 | $2,003.79 |

| 8% | $666.67 | $2,027.64 |

| 8.5% | $708.33 | $2,051.65 |

| 9% | $750.00 | $2,075.84 |

| 9.5% | $791.67 | $2,100.19 |

| 10% | $833.33 | $2,124.70 |

| 10.5% | $875.00 | $2,149.39 |

FAQ

Is a HELOC Better Than a Personal Loan?

In my view, a HELOC is better than a personal loan only when the borrower has a disciplined repayment plan and is using the money for something that justifies putting home equity at risk. The lower rate can be attractive, but the collateral changes the risk completely. A personal loan may have a higher APR, but it does not place a lien on your home.

Here is the lender-side reality: banks like HELOCs because the loan is secured by real estate. That security is why the rate is often lower than a personal loan. But for the borrower, that same feature is the danger. If the loan is used for remodeling, emergency liquidity, or short-term financing with a clear payoff source, a HELOC can be efficient. If it is used for vacations, lifestyle spending, or debt consolidation without changing spending habits, it can turn unsecured debt into home-secured debt.

My rule: use a HELOC when the purpose is tied to home value, cash-flow timing, or a high-confidence payoff plan. Use a personal loan when you want fixed payments, a clean payoff date, and no risk of attaching the debt to your house.

What Is the Difference Between a HELOC and a Home Equity Loan?

The biggest difference is control versus certainty. A HELOC gives you control because you can draw funds as needed and pay interest only on the amount used. A home equity loan gives you certainty because you receive one lump sum with a fixed payment schedule from day one.

From an underwriting and pricing perspective, a HELOC is often treated like a revolving risk product. The bank approves a maximum line, but you decide when to use it. That flexibility is valuable for remodeling projects where costs arrive in phases. However, because most HELOCs are variable-rate products, your payment can change.

A home equity loan is usually better when you know the exact amount you need and want a fixed monthly payment. It is less flexible, but easier to budget. The trap is borrowing the full amount upfront when you only need part of it. You begin paying interest on the entire balance immediately, even if the money sits unused in your checking account.

My practical advice: choose a HELOC for phased or uncertain costs, and choose a home equity loan for one-time expenses with a clear price tag. If your main concern is avoiding payment surprises, fixed-rate debt is usually safer than a variable HELOC.

Write Reply to This Calculator