Credit Card Calculator

Estimate Credit Card Payoff Time, Monthly Payments, and Total Interest

Credit Card Calculator

($)

(%)

Fixed Monthly Payments

($)

Fixed Repayment Period

Years

Months

Calculation Results

Credit Card Balance

Payment Every Month

Repayment Period

Total Payments

Total Interest

Amortization Table

| Month | Payment | Principal | Interest | Ending Balance |

|---|

| Year | Payment | Principal | Interest | Ending Balance |

|---|

Payment Visualization

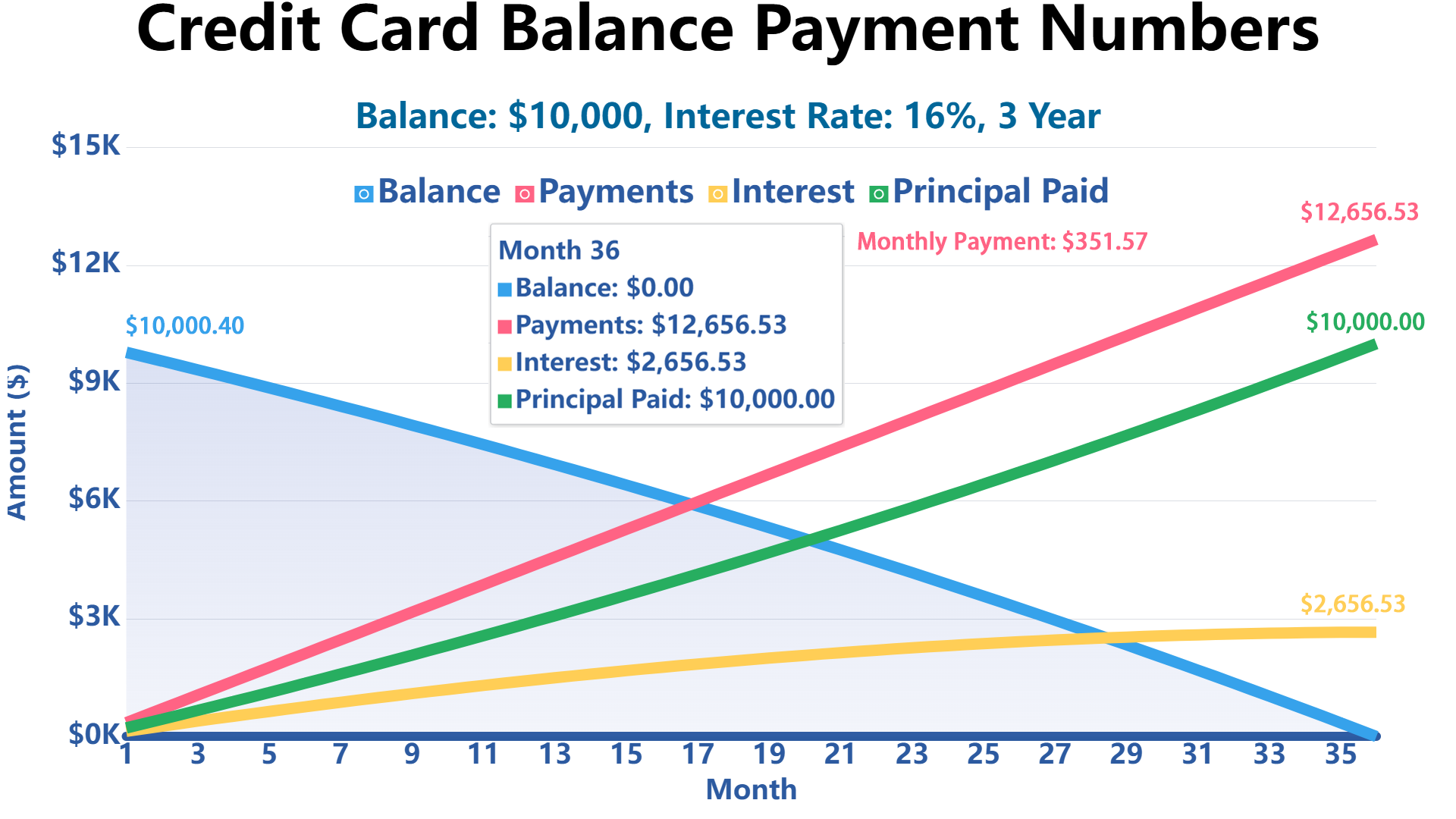

Credit Card Balance $10,000 at 16% Interest, Fixed 3-year Repayment — What Is the Monthly Payment?

The monthly payment for a $10,000 credit card balance at 16% interest over 3 years is $351.57.

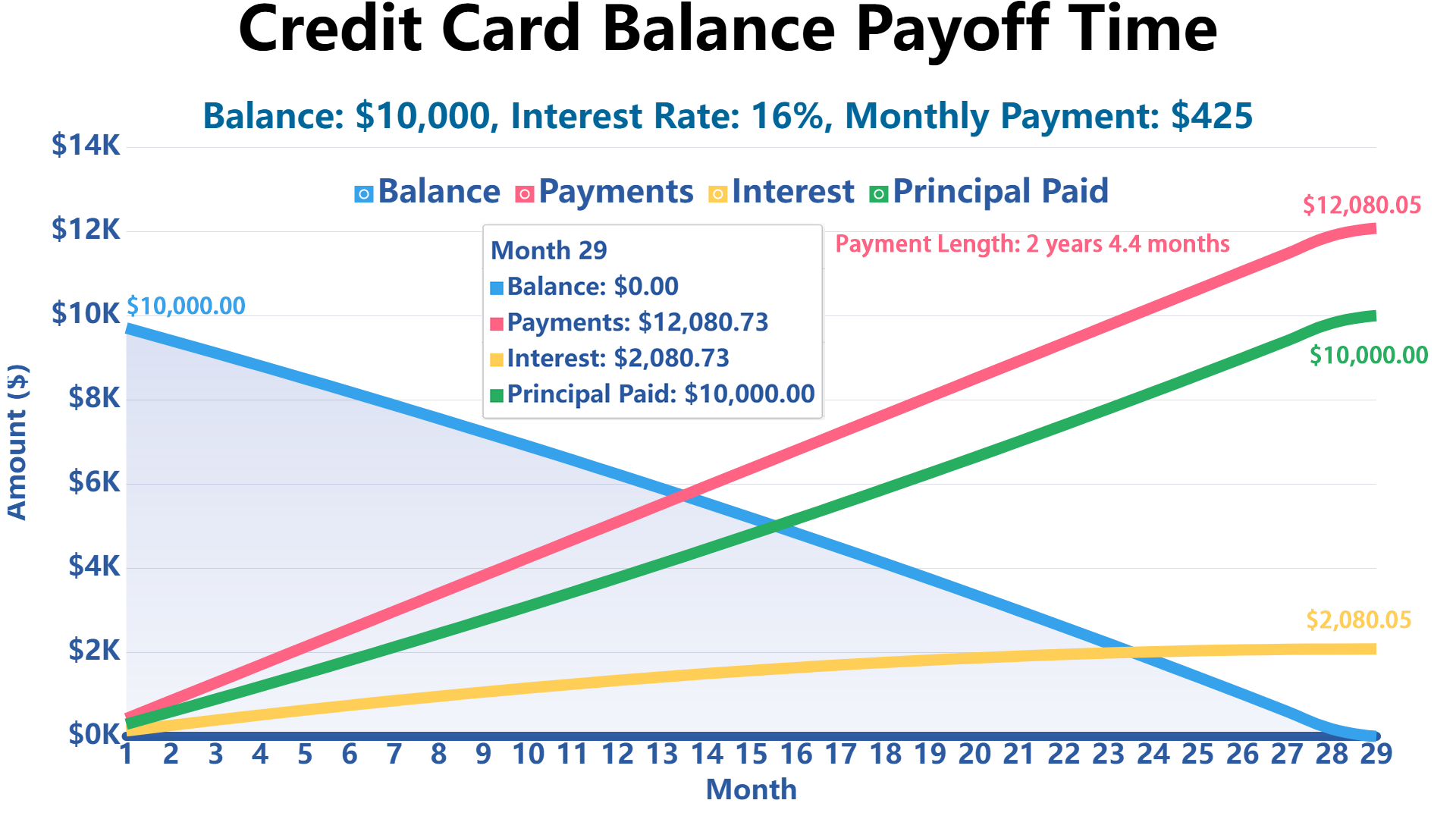

Credit Card Balance $10,000 at 16% Interest, Fixed Monthly Payment $425 - How Long to Pay off?

It will take 2 years and 5 months to pay off the balance.

References

Government Resources:

- Consumer Financial Protection Bureau - Credit Card Interest Rates

- Federal Reserve - Credit Card Interest Rate Information

- Federal Trade Commission - Choosing a Credit Card

- U.S. Treasury - Financial Education Resources

Educational Resources:

- CFPB - Debt Management Strategies

- FDIC Money Smart Financial Education

- SEC - Credit and Your Consumer Rights

Related

Write Reply to This Calculator