Auto Affordability Calculator

How Much Car Can I Afford?

Auto Affordability Calculator

Calculation Results

Amortization Table

| Month | Date | Payment | Principal | Interest | Remaining Balance |

|---|

| Year | End Date | Payment | Principal | Interest | Remaining Balance |

|---|

Payment Visualization

Auto Affordability Pitfall Guide: Key Factors That Can Change Your Real Budget

A car affordability calculator is only as accurate as the numbers you enter. The monthly payment is important, but it is not the whole story. Documentation fees, sales tax, rebates, trade-in equity, and the amount still owed on your old vehicle can all change the true cost of the car.

Before you shop, use this guide to understand the numbers that most often surprise buyers at the dealership.

1. Documentation & Fees: The Hidden Cost Many Buyers Forget

Documentation & Fees include dealer documentation fees, title fees, registration fees, electronic filing fees, destination-related charges, and other administrative costs. These costs may look small compared with the vehicle price, but they can easily add hundreds or even thousands of dollars to the final amount due.

The biggest mistake is shopping based only on the sticker price. For example, a vehicle advertised at $28,500 may not actually cost $28,500 once taxes and fees are added. If you add a 7% sales tax and $2,000 in documentation and registration-related fees, the real purchase cost can rise significantly.

| Cost Item | Example Amount | Why It Matters |

|---|---|---|

| Vehicle Price | $28,500 | This is only the negotiated selling price, not the full cost. |

| Sales Tax at 7% | $1,995 | Tax can add nearly $2,000 before financing even begins. |

| Documentation & Fees | $2,000 | Dealer and government fees can materially change affordability. |

| Estimated Pre-Down-Payment Total | $32,495 | This is much higher than the sticker price. |

Some fees are government-required and usually not negotiable, such as title and registration. Others may be dealer-controlled or vary by dealership. Always ask for an out-the-door price, which includes the vehicle price, taxes, title, registration, documentation fees, dealer add-ons, and any mandatory charges.

2. Manufacturer Rebates: Helpful, But Do Not Let Them Replace Negotiation

Manufacturer Rebates are incentives offered by the automaker, not necessarily discounts funded by the dealer. A rebate can reduce your effective purchase cost, but it should not stop you from negotiating the vehicle price itself.

A common dealership tactic is to present the rebate as if it were the entire discount. For example, if a car has a $1,000 manufacturer rebate, the dealer may say, “We are taking $1,000 off.” But if that $1,000 comes from the manufacturer, the dealer may not have reduced its own selling price at all.

| Scenario | Dealer Price | Rebate |

|---|---|---|

| Weak Deal | $30,000 | $1,000 manufacturer rebate only |

| Better Deal | $29,000 negotiated price | Plus $1,000 manufacturer rebate |

The best approach is to negotiate in two steps. First, negotiate the selling price before rebates. Then apply eligible rebates afterward. This helps you avoid confusing a manufacturer-funded incentive with a true dealer discount.

3. Trade-In Value vs. Owed on Trade-In: The Rollover Loan Trap

Trade-In Value is what the dealer offers for your current vehicle. Owed on Trade-In is the remaining loan balance on that vehicle. The difference between these two numbers determines whether you have positive equity or negative equity.

| Situation | Formula | Result |

|---|---|---|

| Positive Equity | Trade-In Value is greater than Amount Owed | Helps reduce your new loan. |

| Break Even | Trade-In Value equals Amount Owed | No equity is added or subtracted. |

| Negative Equity | Amount Owed is greater than Trade-In Value | The unpaid balance may be rolled into your new loan. |

Negative equity can be dangerous because it creates a rollover loan. This means you are not only financing the new vehicle, but also part of the old vehicle you no longer own. That can make the new loan larger than the car is worth from the first day.

For example, if your old car is worth $10,000 but you still owe $14,000, you have $4,000 in negative equity. If that $4,000 is rolled into your next auto loan, a $30,000 car may effectively become a $34,000 financed purchase before taxes, fees, and interest.

4. Why Including Taxes and Fees in the Loan Changes the Real Cost

This calculator includes an option to Include Taxes and Fees in Loan. This can lower the amount of cash you need at signing, but it increases the amount you finance. When taxes and fees are financed, you pay interest on them over the life of the loan.

Paying taxes and fees upfront usually lowers your total interest cost. Financing them may be convenient, but it can make the vehicle more expensive over time.

| Choice | Cash Needed Today | Long-Term Cost |

|---|---|---|

| Pay Taxes & Fees Upfront | Higher | Lower loan balance and less interest. |

| Include Taxes & Fees in Loan | Lower | Higher loan balance and more interest. |

Real-World Case Study: How a Buyer Used Trade-In Equity and Rebates Wisely

Consider this example: a buyer has a monthly car budget of $500 and wants to buy a compact SUV priced around $28,500. The buyer also has an old vehicle to trade in.

| Input | Example Value | Meaning |

|---|---|---|

| Monthly Budget | $500 | Target monthly principal and interest payment. |

| Vehicle Price | $28,500 | Negotiated SUV selling price. |

| Down Payment | $10,000 | Cash paid upfront to reduce the loan. |

| Manufacturer Rebate | $1,000 | Automaker incentive applied after negotiation. |

| Trade-In Value | $1,500 | Dealer offer for the old vehicle. |

| Owed on Trade-In | $600 | Remaining loan balance on the old vehicle. |

| Sales Tax | 7% | Estimated tax rate. |

| Documentation & Fees | $2,000 | Estimated dealer, title, registration, and processing fees. |

In this case, the buyer has $900 in positive trade-in equity, because the trade-in is worth $1,500 and only $600 is still owed.

That $900 helps reduce the amount that needs to be financed. Combined with the $10,000 down payment and the $1,000 manufacturer rebate, the buyer lowers the loan balance substantially.

The key lesson is that the buyer did not focus only on the monthly payment. Instead, the buyer checked the full structure of the deal:

- The trade-in had positive equity, so it helped reduce the new loan instead of increasing it.

- The manufacturer rebate was applied after price negotiation, so it did not replace dealer-level negotiation.

- Documentation and fees were reviewed before signing, so there were no last-minute surprises.

- The buyer avoided rolling old debt into the new loan, which helped keep the loan healthier from day one.

This is a much safer structure than buying based only on whether the monthly payment looks affordable.

Current Auto Loan APR Benchmarks for 2026

Auto loan rates vary based on credit score, loan term, vehicle age, lender, down payment, and loan-to-value ratio. The rates below are examples of publicly listed credit union rates as of late May 2026. They are useful as a general benchmark, but your actual rate may be higher or lower.

| Lender / Source | New Auto APR Benchmark | Used Auto APR Benchmark |

|---|---|---|

| Navy Federal Credit Union | As low as 3.89% for 12-36 months | As low as 4.79% for 12-36 months |

| UW Credit Union | As low as 4.72% for 48 months | As low as 4.72% for 36 months |

| Greater Texas Credit Union | As low as 5.51% for eligible newer models up to 36 months | Varies by model year, mileage, and term |

| Innovations Financial Credit Union | As low as 2.99% for a 24-month term | Rates vary by loan type, term, and credit history |

As a practical planning range, strong-credit borrowers may see advertised auto loan APRs roughly between 3% and 6% for shorter terms, while longer terms, older used vehicles, weaker credit profiles, and higher loan-to-value deals can cost more.

A lower monthly payment from a longer loan term can be misleading. Longer terms often increase total interest and may keep you upside down on the loan for a longer period. Many affordability guidelines recommend keeping the car payment around 10% to 15% of take-home pay and total transportation costs below 20% of take-home pay.

Quick Checklist Before You Sign an Auto Loan

Before accepting a financing offer, review the full deal instead of focusing only on the monthly payment.

- Ask for the out-the-door price, including vehicle price, taxes, title, registration, documentation fees, and dealer add-ons.

- Negotiate the selling price before rebates, then apply manufacturer incentives afterward.

- Check your trade-in equity by subtracting the amount owed from the trade-in value.

- Avoid rolling negative equity into the new loan unless you fully understand the long-term cost.

- Compare APRs from banks, credit unions, and dealer financing before going to the dealership.

- Keep the loan term reasonable, because very long terms may reduce the monthly payment but increase total interest.

- Review optional products carefully, including GAP insurance, extended warranties, service contracts, tire protection, and maintenance plans.

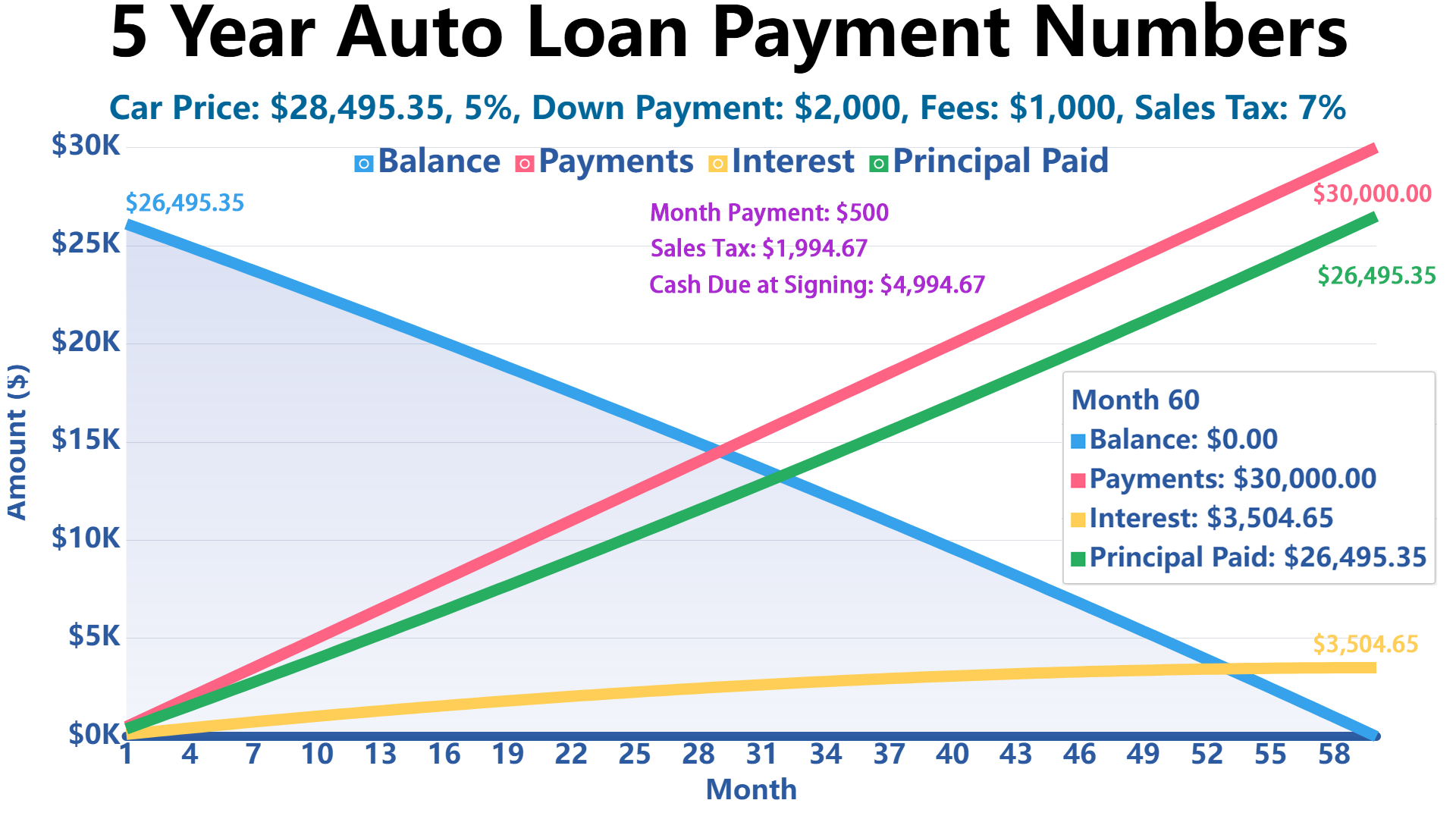

If My Monthly Car Budget Is $500, How Much Car Can I Afford?

That depends on your down payment, interest rate, loan term, as well as sales tax and fees. Let's say you put down $2,000, with a 5% APR, a 60-month loan term, 7% sales tax, and $1,000 in fees. With those numbers, the most expensive car you could afford would be priced at $28,495.35.

References

Government Resources:

- Consumer.gov - Buying a Car

- FTC.gov - Auto Financing Guidelines

- CFPB.gov - Auto Loan Information

- USA.gov - Car Buying Guide

Write Reply to This Calculator