Debt Consolidation Calculator

Compare Repaying Your Current Debts With the Debt Avalanche Method Against a Consolidation Loan to See if Debt Consolidation Is Worth It.

Debt Consolidation Calculator

1.

2.

3.

4.

5.

6.

($)

Years Months

(%)

Calculation Results

Visual Comparison

Payment Comparison

All Debts Detailed Amortization

Amortization Schedule Comparison

| Month | Principal | Interest | Payment | Ending Balance |

|---|

| Month | Principal | Interest | Payment | Ending Balance |

|---|

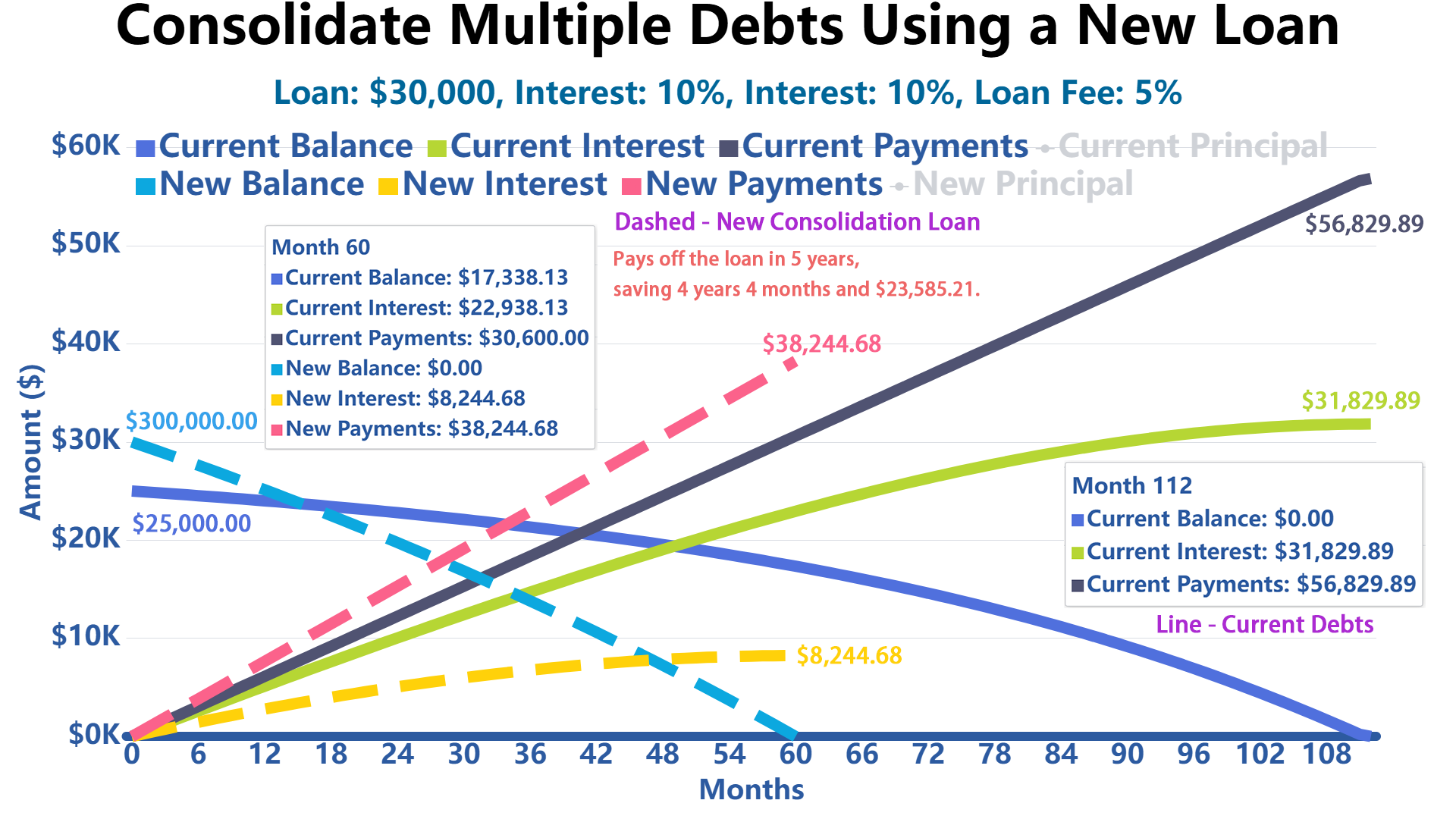

How to Consolidate Multiple Debts Using a New Loan?

Debt consolidation example

Let’s say you have the following debts:

- Credit card 1 balance: $3,500 at 19.9% interest, with a $120 minimum payment.

- Credit card 2 balance: $5,500 at 20.9% interest, with a $110 minimum payment.

- Credit card 3 balance: $7,500 at 18.9% interest, with a $130 minimum payment.

- Credit card 4 balance: $8,500 at 22.9% interest, with a $150 minimum payment.

Debt Consolidation Loan:

- Loan Amount ($): $30,000

- Loan Term: 5 Year

- Interest: 10%

- Loan Fee: 5%

Your current debts carry an effective APR of 20.91%, while the consolidation loan (including fees) has an APR of 12.24%. Overall, the loan’s financing cost is lower, meaning new consolidation loan would save you money in the long run.

With a loan fee of $1500.00, you’ll actually receive $28,500.00 to pay off your existing balance of $25,000.00. This leaves you with a surplus of $3,500.00 after paying off your debts.

| Your Current debts | New Consolidation Loan | |

|---|---|---|

| Effective APR | 20.91% | 12.24% |

| Outstanding Balance / Loan Amount | $25,000.00 | $30,000.00 |

| Origination Fee / Points | $0 | $1,500.00 |

| Net Amount Received | - | $28,500.00 |

| Monthly Payment | $510.00 | $637.41 |

| Estimated Payoff Period | 112 months (9 years and 4 months) | 60 months (5 years and 0 months) |

| Extra Cash After Payoff | $0 | $3,500.00 |

| Total You’ll Pay | $56,829.89 | $38,244.68 |

| Total Interest Cost | $31,829.89 | $8,244.68 |

References

Government Resources

- Federal Trade Commission - Debt Relief Services

- Consumer Financial Protection Bureau - Debt Consolidation Guide

- USA.gov - Managing Debt

- IRS - Interest Deduction Guidelines

Educational Resources

Related

Write Reply to This Calculator