Additional Contribution Calculator

How Much Monthly Deposit Will I Need to Reach My Target?

Additional Contribution Calculator

($)

(%)

year month

($)

(%) per year

Calculation Results

Monthly Contribution

Total Contribution

End Balance

Total Interest

Initial Balance

Effective Annual Rate

Interest from Initial Investment

Interest from Additional Deposits

Annualized Return (CAGR-Compound Annual Growth Rate)

Contributions Accumulation Schedule

Accumulation Visualization

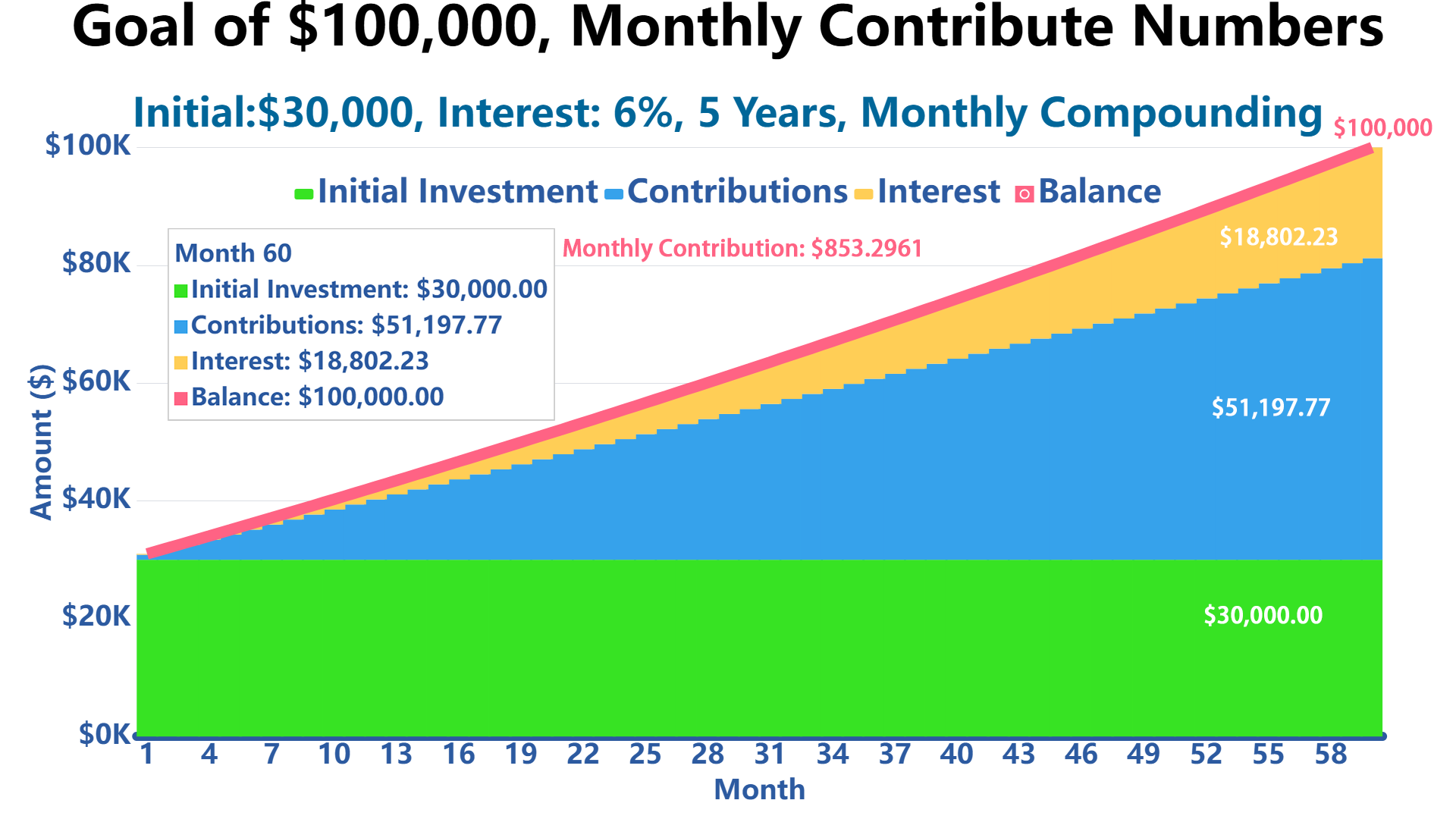

To Reach Your Goal of $100,000, How Much Should You Contribute to Investments Each Month?

So let's say you're starting with $30,000, and you're getting about 6% returns with monthly compounding. If you invest around $853.30 every month, you'll have $100,000 in your account after five years.

| Annual Return Rate | Monthly Contribution Amount (5 year) | Yearly Contribution Amount (5 year) |

|---|---|---|

| 3% | 1,007.808 | $12,261.382 |

| 3.5% | $981.755 | $11,971.903 |

| 4% | $955.823 | $11,682.514 |

| 4.5% | $930.011 | $11,393.216 |

| 5% | $904.32 | $11,104.011 |

| 5.5% | $878.748 | $10,814.901 |

| 6% | $853.296 | $10,525.887 |

| 6.5% | $827.964 | $10,236.972 |

| 7% | $802.751 | $9,948.155 |

| 7.5% | $777.656 | $9,659.438 |

| 8% | $752.681 | $9,370.822 |

| 8.5% | $727.824 | $9,082.307 |

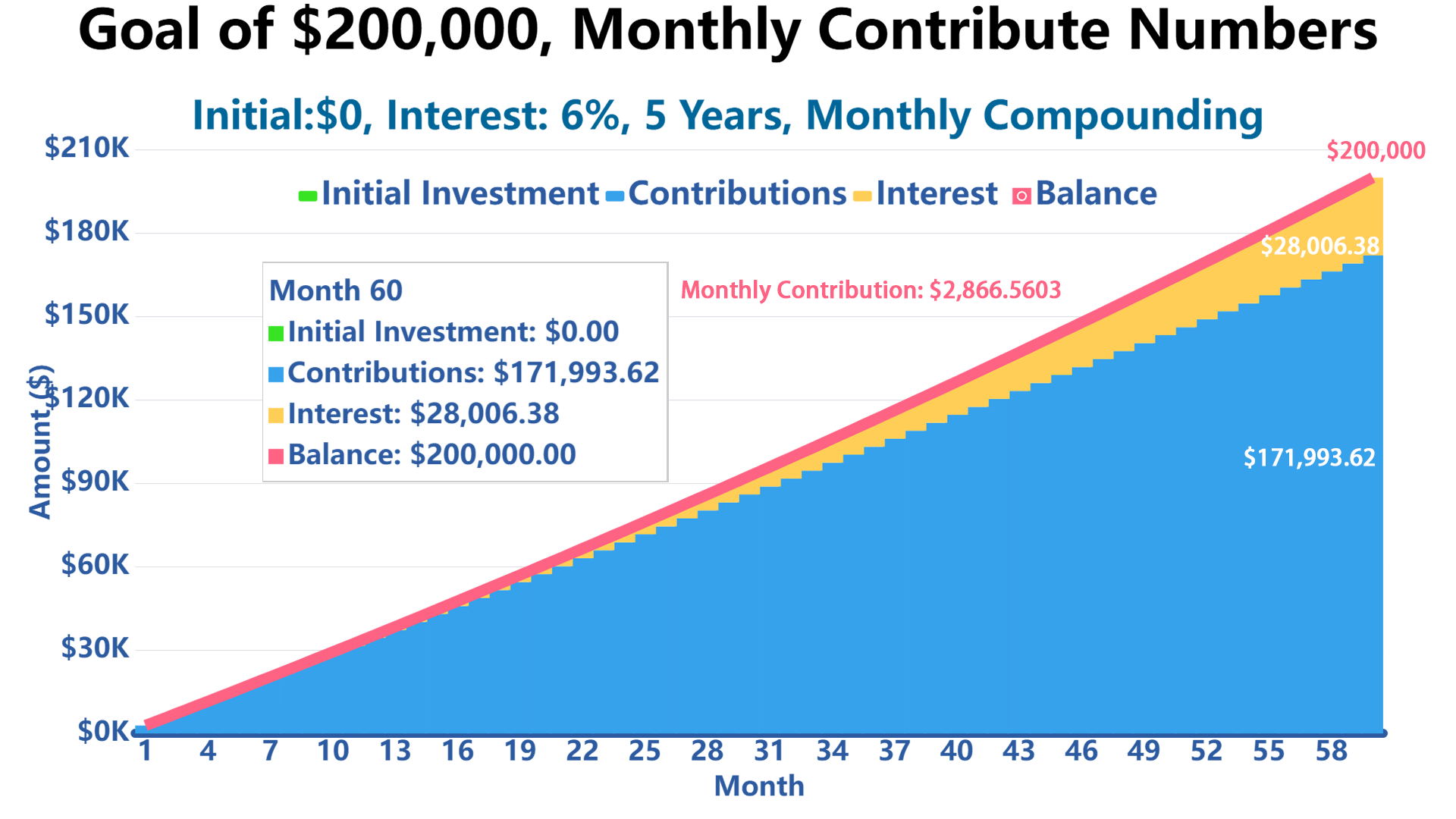

To Reach Your Goal of $200,000, How Much Should You Contribute to Your Investments Each Month, Assuming a 6% Annual Return With Monthly Compounding and an initial Investment of $0?

To reach your goal of $200,000 in 5 years with a 6% annual return compounded monthly and an initial investment of $0, you should contribute $2,866.56 each month.

| Annual Return Rate | Monthly Contribution Amount (5 year) | Monthly Contribution Amount (10 year) |

|---|---|---|

| 3% | $3,093.74 | $1,431.22 |

| 3.5% | $3,055.02 | $1,394.38 |

| 4% | $3,016.64 | $1,358.24 |

| 4.5% | $2,978.60 | $1,322.77 |

| 5% | $2,940.91 | $1,287.98 |

| 5.5% | $2,903.57 | $1,253.86 |

| 6% | $2,866.56 | $1,220.41 |

| 6.5% | $2,829.90 | $1,187.63 |

| 7% | $2,793.57 | $1,155.50 |

| 7.5% | $2,757.60 | $1,124.04 |

| 8% | $2,721.95 | $1,093.22 |

| 8.5% | $2,686.64 | $1,063.05 |

References

Government Resources

- SEC Investor.gov - Official SEC investor education and protection website

- SEC: 10 Things to Consider Before You Make Investing Decisions

- TreasuryDirect.gov - Official U.S. Treasury securities information

- Federal Reserve: Economic Research and Data

- CFPB Retirement Planning Tools

Educational Resources

- FINRA Investor Education

- SEC: Asset Allocation

- Bureau of Labor Statistics - Consumer Price Index (for inflation data)

Related

Write Reply to This Calculator