Home Equity Loan Calculator

Calculate Your Monthly Payments, Total Costs and APR

Home Equity Loan Calculator

Calculation Results

Payment Visualization

Amortization Tables

| Year | Date | Payment | Principal | Interest | Ending Balance |

|---|

| Month | Date | Payment | Principal | Interest | Ending Balance |

|---|

Expert Market Note: May 2026 Home Equity Loan Rate Watch

Updated May 29, 2026: Home equity loan rates remain elevated compared with the ultra-low-rate years, but they have become more competitive for well-qualified borrowers. As of May 2026, many advertised fixed home equity loan offers are clustered around the high-6% to low-8% APR range, depending on credit score, loan-to-value ratio, loan amount, property location and lender fees.

In practical terms, borrowers with a 740+ credit score, stable income, low debt-to-income ratio and at least 20% to 30% remaining equity after borrowing are usually in the strongest position to negotiate. If your quoted APR is near 8% or higher, it may still be reasonable in today’s market, but it is worth comparing at least three lenders, including a local credit union, a national bank and an online lender.

Expert takeaway: Do not compare rates alone. A 7.49% loan with high closing costs can be more expensive than a 7.90% loan with low or waived fees, especially if you plan to repay the loan early.

What the Home Equity Loan Application Process Usually Feels Like

A home equity loan is not approved only because you have equity. In most real applications, the lender reviews your credit profile, income documents, existing mortgage balance, property value and total monthly debts before issuing final approval. The process often feels similar to applying for a smaller second mortgage.

A typical borrower should expect several steps: a preliminary quote, document upload, property valuation, underwriting review, final approval, closing disclosure review and signing. Even if a lender advertises a fast approval, the timeline can slow down if the appraisal, title review or income verification raises questions.

| Application Stage | What Usually Happens | Common Borrower Tip |

|---|---|---|

| Prequalification | The lender estimates your rate and possible loan amount using basic credit, income and property information. | Ask whether the quote includes fees, points and any automatic payment discount. |

| Document Review | You may need to provide pay stubs, W-2s, tax returns, mortgage statements, homeowners insurance and ID. | Upload clear documents early to avoid underwriting delays. |

| Property Valuation | The lender may use an automated valuation, drive-by appraisal or full interior appraisal. | Do not assume your online home-value estimate will match the lender’s valuation. |

| Underwriting | The lender checks credit, debt-to-income ratio, combined loan-to-value ratio and title conditions. | Avoid opening new credit cards, auto loans or large debts during this stage. |

| Closing | You review final terms, sign loan documents and wait for funding after any required rescission period. | Compare the final APR, payment, fees and payoff date against your original quote. |

Home Equity Loan Mistakes to Avoid

Because a home equity loan is secured by your home, small mistakes can become expensive. Before signing, focus on the full cost of borrowing rather than just the monthly payment.

- Do not borrow more than you need. A larger loan may look affordable over 10 or 15 years, but it reduces your home equity and increases total interest.

- Do not ignore closing costs. Origination fees, appraisal fees, title charges and recording fees can change the real APR of the loan.

- Do not use home equity for short-lived purchases. Financing vacations, luxury goods or everyday spending with home equity can put long-term housing security at risk.

- Do not assume a fixed rate means the loan is always cheap. A fixed monthly payment is helpful, but the total interest cost can still be high on longer terms.

- Do not skip the payoff scenario. If you plan to sell or refinance soon, ask whether there are early closure fees, recording fees or payoff processing costs.

Estimated Home Equity Loan Closing Costs by State

Closing costs vary by lender, county and loan size. The table below shows common estimated third-party cost ranges a borrower may see when applying for a home equity loan. Some banks and credit unions may waive part of these costs, while others may charge them upfront or deduct them from the loan proceeds.

| State | Common Appraisal or Valuation Fee | Typical Title, Recording and Search Fees |

|---|---|---|

| California | $400-$750 | $300-$900 |

| Texas | $350-$700 | $250-$800 |

| Florida | $350-$650 | $300-$950 |

| New York | $450-$800 | $500-$1,200 |

| Illinois | $350-$650 | $250-$750 |

Important: These are estimated market ranges, not guaranteed lender quotes. Always request a written loan estimate or fee worksheet before comparing offers.

How to Read Your Home Equity Loan Results

The calculator results are designed to show both the monthly affordability and the long-term cost of the loan. The monthly payment tells you whether the loan fits your budget, while the total interest and real APR help you compare offers more accurately.

| Result | What It Means | Why It Matters |

|---|---|---|

| Loan Amount | The full amount borrowed before any deducted closing costs. | This is the balance used to calculate your scheduled repayment. |

| Cash Received | The amount you actually receive if fees are deducted from the loan. | This helps you avoid overestimating available funds. |

| Monthly Pay | Your estimated fixed monthly payment. | This should fit comfortably within your monthly budget. |

| Total Interest | The interest paid over the full loan term. | Longer terms usually lower the payment but increase total interest. |

| Real Rate APR | The estimated annual cost after accounting for closing costs. | This is often better than the note rate for comparing loan offers. |

FAQ

Why use this home equity loan calculator?

This calculator estimates your monthly payment, total interest, payoff date and real APR. It is especially useful when comparing loan offers with different interest rates, terms and closing costs.

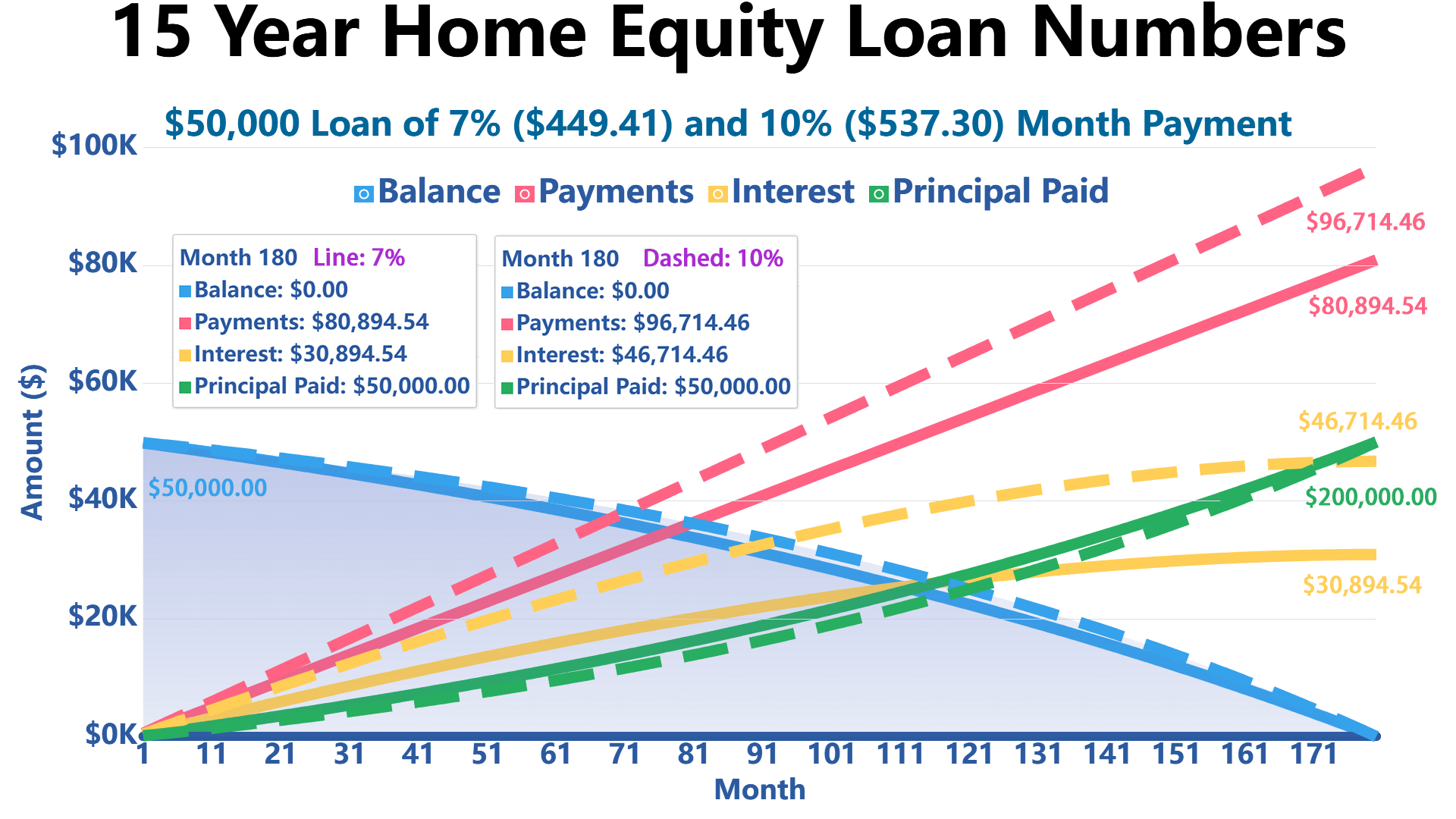

How Much Would a $50,000 Home Equity Loan Cost Per Month?

A $50,000 home equity loan might cost about $449.41–$537.30 per month on a 15-year term at roughly 7%–10% APR (exact payment depends on your rate and term).

What Is the Average Payment on a $100,000 Home Equity Loan?

The average payment on a $100,000 home equity loan is often around $1,161.08–$1,321.51 per month on a 10-year term at roughly 7%–10% APR, depending on the exact rate and term.

What is one major disadvantage of a home equity loan?

The biggest disadvantage is that your home is used as collateral. If you cannot repay the loan as agreed, the lender may have the right to foreclose on your home.

How much can I borrow with a home equity loan?

Many lenders allow qualified borrowers to borrow up to about 80% to 85% of the home’s appraised value, minus the current mortgage balance. For example, if your home is worth $300,000 and your mortgage balance is $200,000, an 85% combined loan-to-value limit could allow total mortgage debt of up to $255,000, leaving about $55,000 in possible home equity borrowing capacity.

Is a home equity loan better than a HELOC?

A home equity loan may be better if you want a fixed rate, one lump sum and predictable monthly payments. A HELOC may be better if you need flexible access to funds over time, but HELOC rates are often variable and payments can change.

What credit score do I need for a home equity loan?

Requirements vary by lender, but many lenders prefer borrowers with scores in the high 600s or above. Borrowers with scores above 720 or 740 often have a better chance of receiving more competitive pricing, assuming income, debt and equity requirements are also strong.

Can closing costs be deducted from a home equity loan?

Some lenders allow closing costs to be deducted from the loan proceeds, while others require them to be paid upfront. Deducting costs may reduce the cash you receive and can increase the real cost of the loan.

Is home equity loan interest tax deductible?

In some cases, interest may be deductible if the funds are used to buy, build or substantially improve the home that secures the loan. Tax rules can change, so borrowers should consult a qualified tax professional before relying on a deduction.

Write Reply to This Calculator