PMI Calculator

Calculate Private Mortgage Insurance & Removal Date

PMI Calculator

Calculation Results

| Item | Monthly | Total |

|---|---|---|

| Mortgage Payment | ||

| PMI | ||

| Property Tax | ||

| Home Insurance | ||

| HOA Fee | ||

| Other Costs | ||

| Total Out-of-Pocket | With PMI: After PMI: |

PMI Payment Table

| Month | Date | Principal | Interest | LTV Ratio | PMI | Ending Balance | Out-of-Pocket |

|---|

| Year | Date | Principal | Interest | PMI | Ending Balance |

|---|

Payment Visualization

What PMI Rates Can I Expect Based on My Credit Score?

PMI rates vary significantly based on your credit score. Here's a typical breakdown:

| Credit Score Range | Annual PMI Rate | Monthly Cost (on $450,000 loan) |

|---|---|---|

| 760+ | 0.4% | $150.00/month |

| 740-759 | 0.5% | $187.50/month |

| 720-739 | 0.7% | $262.50/month |

| 700-719 | 0.8% | $300.00/month |

| 680-699 | 1.0% | $375.00/month |

| 660-679 | 1.25% | $468.75/month |

| 640-659 | 1.4% | $525.00/month |

| 620-639 | 1.50% | $562.50/month |

How To Calculate PMI (Private Mortgage Insurance)?

PMI is calculated by dividing the annual PMI cost by 12 to get the monthly payment, and it continues until your loan-to-value (LTV) ratio drops to 80% or below.

Step 1: Determine if PMI is Required

Down Payment Percentage = (Down Payment ÷ Home Price) × 100 PMI Required if: Down Payment < 20%

Step 2: Calculate Monthly PMI Payment

Monthly PMI = Annual PMI Cost ÷ 12

Step 3: Calculate When PMI Ends

Current LTV = (Remaining Loan Balance ÷ Home Price) × 100 PMI stops when: LTV ≤ 80%

Step 4: Calculate Monthly Mortgage Payment (P&I)

Monthly Payment = [P × r × (1 + r)^n] ÷ [(1 + r)^n - 1] Where: P = Principal (Loan Amount) r = Monthly Interest Rate (Annual Rate ÷ 12 ÷ 100) n = Total Number of Payments (Years × 12)

Step 5: Track Principal Balance Each Month

Interest Payment = Remaining Balance × Monthly Interest Rate Principal Payment = Monthly Payment - Interest Payment New Balance = Remaining Balance - Principal Payment

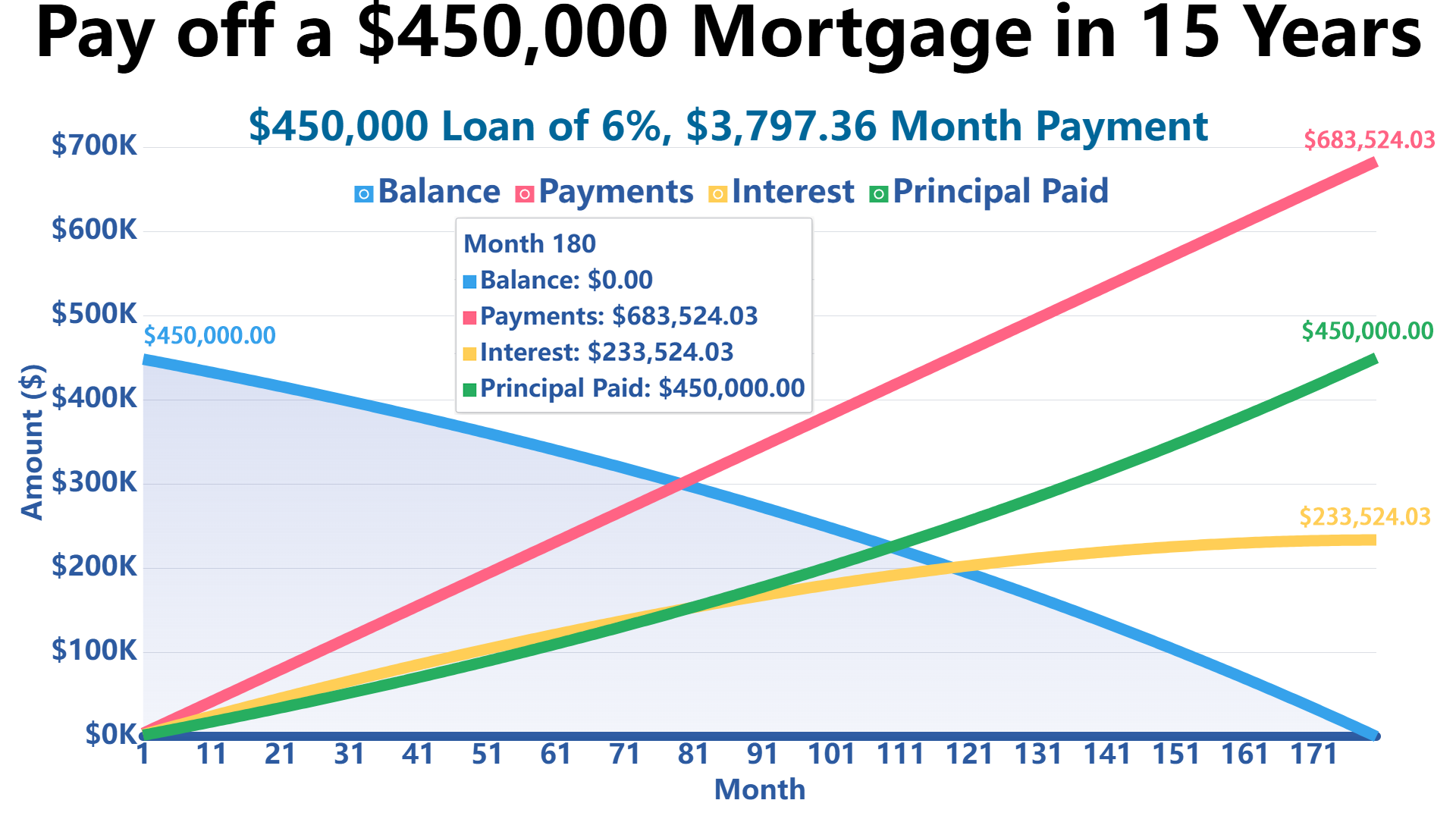

Given Data:

- Home Price: $500,000

- Down Payment: $50,000 (10%)

- Annual Interest Rate: 6%

- Loan Term: 15 years

- Annual PMI: $1,000

1. Down Payment Check

Down Payment % = ($50,000 ÷ $500,000) × 100 = 10%

Since 10% < 20% → PMI is REQUIRED ✓

2. Loan Amount

Loan Amount = $500,000 - $50,000 = $450,000

3. Monthly PMI

Monthly PMI = $1,000 ÷ 12 = $83.33

4. Monthly Mortgage Payment (P&I)

P = $450,000

r = 6% ÷ 12 ÷ 100 = 0.005

n = 15 × 12 = 180 months

Monthly P&I = [$450,000 × 0.005 × (1.005)^180] ÷ [(1.005)^180 - 1]

= $3,797.365. Total Monthly Payment (with PMI)

Total Payment = $3,797.36 + $83.33 = $3,880.69

6. When Does PMI Stop?

| Month | Principal Payment | Remaining Balance | LTV | PMI Status |

|---|---|---|---|---|

| 1 | $1,547.36 | $448,452.64 | 89.69% | Active |

| 2 | $1,555.09 | $446,897.55 | 89.38% | Active |

| ... | ... | ... | ... | ... |

| 30 | $1,788.16 | $400,051.33 | 80.01% | Active |

| 31 | $1,797.10 | $398,254.23 | 79.65% | STOPS ✓ |

7. Total PMI Paid

Total PMI = $83.33 × 30 = $2,500.00

| Item | Value |

|---|---|

| Monthly P&I Payment | $3,797.36 |

| Monthly PMI | $83.33 |

| Total with PMI (months 1-30) | $3,880.69 |

| PMI Duration | 30 months |

| Total PMI Paid | $2,500.00 |

| Payment after PMI ends | $3,797.36 |

You will pay $83.33/month PMI for 30 months, totaling $2,500.00. After month 30, your monthly payment drops from $3,880.69 to $3,797.36 (savings of $83.33/month).

What Is the Difference Between PMI and FHA Mortgage Insurance?

It's important to distinguish between conventional PMI and FHA mortgage insurance:

| Feature | Conventional PMI | FHA Mortgage Insurance |

|---|---|---|

| Cancellation | Removable at 78-80% LTV | Permanent (if down payment < 10%) |

| Upfront Cost | None | 1.75% of loan amount |

| Monthly Cost | 0.4% - 1.5% annually | 0.55% - 0.85% annually |

| Credit Requirements | Higher (typically 620+) | Lower (typically 580+) |

A Banker's Insider Tip: 3 Hidden Pitfalls When Requesting Your Lender to Drop PMI

Reaching 80% loan-to-value does not always mean your PMI disappears automatically the next day. In practice, lenders often have internal rules and documentation requirements that a calculator cannot predict. Before you request PMI cancellation, watch out for these common hidden pitfalls.

1. You may have to pay for a lender-approved appraisal

Many borrowers assume the lender will simply use the current market value from Zillow, Redfin, or a recent local sale. In reality, many banks require a formal appraisal or broker price opinion from an institution or appraiser they approve.

This appraisal is often paid by the borrower, and the cost can range from a few hundred dollars to more than $700, depending on your location and lender policy. If the appraisal comes in lower than expected, your request to remove PMI may be denied even if online home value estimates suggest you have enough equity.

2. Some lenders require the loan to be at least two years old

Even if your home value rises quickly, some lenders will not consider PMI removal based on a new appraised value until the mortgage has been seasoned for a certain period, commonly two years.

For example, if you bought a home with 10% down and home prices increased significantly after one year, you may believe your LTV is already below 80%. However, your lender may still require you to wait until the loan reaches its minimum seasoning requirement before approving PMI cancellation based on appreciation.

3. Late payments can delay or block PMI cancellation

PMI cancellation is not based only on your LTV ratio. Lenders may also review your payment history. If you have recent late payments, the lender may deny your request even if your equity position is strong.

Under many lender policies, you must be current on your mortgage and may need a clean recent payment history. Before applying for PMI removal, check whether you have had any late payments in the past 12 to 24 months.

Before paying for an appraisal or submitting a PMI removal request, call your loan servicer and ask for their exact PMI cancellation rules. Specifically ask about appraisal requirements, loan seasoning rules, payment history requirements, and whether they use original home value or current appraised value to calculate LTV.

FAQ

How Can I Avoid PMI?

Avoid PMI by making a 20% down payment, using a piggyback loan, or qualifying for VA/USDA loans that don't require PMI.

When Can You Remove PMI?

You can remove PMI when your loan-to-value ratio reaches 80% (by request) or it's automatically cancelled at 78%.

What Are Tips for Reducing PMI Costs?

Reduce PMI costs by improving your credit score, making extra principal payments to reach 80% LTV faster, and shopping multiple lenders for the best rates.

Does PMI Protect Me as the Homeowner?

No, PMI protects the lender, not you. It covers the lender's risk if you default on the loan. You should maintain separate homeowners insurance to protect your investment.

References

This PMI calculator is based on industry-standard practices and regulations. For official information about mortgage insurance and consumer protections, consult these authoritative sources:

Government Resources

- Consumer Financial Protection Bureau (CFPB) - Private Mortgage Insurance:

https://www.consumerfinance.gov/ask-cfpb/what-is-private-mortgage-insurance-en-122/

Official guidance on PMI requirements, cancellation rights, and consumer protections under the Homeowners Protection Act. - U.S. Department of Housing and Urban Development (HUD) - Home Loans:

https://www.hud.gov/buying/loans

Information about FHA mortgage insurance and how it differs from conventional PMI. - Internal Revenue Service (IRS) - Mortgage Insurance Premiums:

https://www.irs.gov/forms-pubs/about-publication-936

Tax information regarding mortgage insurance premium deductions (Publication 936). - USA.gov - Mortgages and Homebuying:

https://www.usa.gov/mortgages

Comprehensive government resources for homebuyers including mortgage insurance information.

Write Reply to This Calculator