Auto Loan Calculator

Calculate total loan amount, monthly payments, total interest, total cost of an auto loan.

Auto Loan Calculator

Calculation Results

Amortization Table

| Month | Date | Payment | Principal | Interest | End Balance |

|---|

| Year | Date | Payment | Principal | Interest | End Balance |

|---|

Payment Visualization

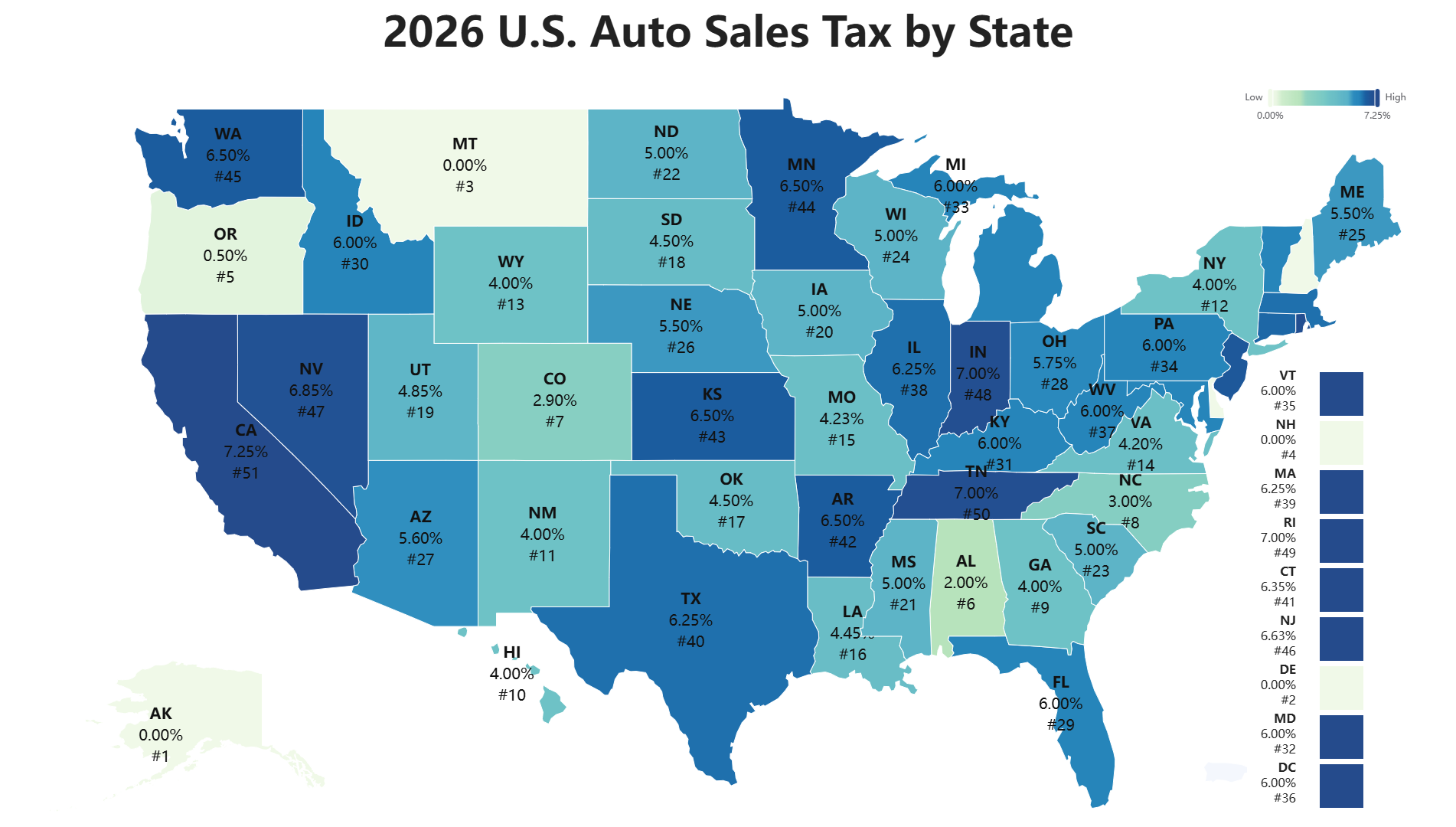

2026 U.S. Auto Sales Tax Comparison by State

Use this table to estimate the state-level sales tax portion of your auto purchase. Actual out-the-door cost may be higher because local taxes, registration fees, title fees, documentation fees, and dealer charges can vary by city, county, and dealership.

| State | Sales Tax Rate | State | Sales Tax Rate |

|---|---|---|---|

| Alabama | 2.00% | Alaska | 0.00% |

| Arizona | 5.60% | Arkansas | 6.50% |

| California | 7.25% | Colorado | 2.90% |

| Connecticut | 6.35% | Delaware | 0.00% |

| Florida | 6.00% | Georgia | 4.00% |

| Hawaii | 4.00% | Idaho | 6.00% |

| Illinois | 6.25% | Indiana | 7.00% |

| Iowa | 5.00% | Kansas | 6.50% |

| Kentucky | 6.00% | Louisiana | 4.45% |

| Maine | 5.50% | Maryland | 6.00% |

| Massachusetts | 6.25% | Michigan | 6.00% |

| Minnesota | 6.50% | Mississippi | 5.00% |

| Missouri | 4.23% | Montana | 0.00% |

| Nebraska | 5.50% | Nevada | 6.85% |

| New Hampshire | 0.00% | New Jersey | 6.63% |

| New Mexico | 4.00% | New York | 4.00% |

| North Carolina | 3.00% | North Dakota | 5.00% |

| Ohio | 5.75% | Oklahoma | 4.50% |

| Oregon | 0.50% | Pennsylvania | 6.00% |

| Rhode Island | 7.00% | South Carolina | 5.00% |

| South Dakota | 4.50% | Tennessee | 7.00% |

| Texas | 6.25% | Utah | 4.85% |

| Vermont | 6.00% | Virginia | 4.20% |

| Washington | 6.50% | Washington D.C. | 6.00% |

| West Virginia | 6.00% | Wisconsin | 5.00% |

| Wyoming | 4.00% |

Note: These are base state-level rates used for calculator estimates. Local vehicle taxes and DMV fees may apply.

Real-World Case Study: When Your Trade-In Still Has a Loan Balance

One of the most common dealer finance-office traps happens when a buyer trades in a car that still has a loan payoff. The dealer may talk mainly about the monthly payment and the trade allowance, while the unpaid loan balance quietly gets rolled into the new car loan.

Case Setup Based on This Calculator

| Item | Amount | What It Means |

|---|---|---|

| Auto Price | $50,000 | The negotiated vehicle price before tax, fees, and finance charges. |

| Down Payment | $10,000 | Your cash contribution that reduces the loan balance. |

| Trade Allowance | $1,500 | The dealer’s value for your old car. |

| Owed on Trade-In | $600 | The remaining payoff to the bank on your old car. |

| Net Trade Equity | $900 | $1,500 trade allowance minus $600 payoff. |

Why the $600 Payoff Matters

At first, a $600 payoff does not look dangerous. But if that amount is rolled into the new loan, you are not just paying $600. You are financing that $600 over the life of the new auto loan. With the calculator’s default 36-month term at 5% APR, that $600 adds approximately $17.98 per month and about $47.36 in extra interest.

| Loan Scenario | Extra Principal Rolled In | Approx. Extra Monthly Payment | Approx. Total Paid on That $600 | Approx. Interest Cost |

|---|---|---|---|---|

| 36 months at 5.0% APR | $600 | $17.98 | $647.36 | $47.36 |

| 60 months at 6.5% APR | $600 | $11.74 | $704.40 | $104.40 |

| 72 months at 7.5% APR | $600 | $10.38 | $747.36 | $147.36 |

| 84 months at 8.0% APR | $600 | $9.35 | $785.40 | $185.40 |

The risk becomes much larger when the old car has negative equity. For example, if you owe $4,000 on a car worth only $1,500, the $2,500 shortfall may be added to the new loan. That means you begin the new loan already underwater.

How to Avoid the Trade-In Trap

- Ask your current lender for a written 10-day payoff quote before visiting the dealer.

- Negotiate the new car price separately from your trade-in value.

- Focus on the out-the-door price, not the monthly payment.

- Confirm that the retail installment contract clearly shows the trade allowance and payoff amount.

- Do not accept a longer loan term just to hide negative equity inside a lower monthly payment.

New Car vs. Used Car: Which Is More Cost-Effective?

New and used cars have different cost structures. A new car usually has lower maintenance costs and full warranty coverage, but it depreciates faster. A 2–3 year certified pre-owned vehicle often avoids the steepest depreciation while still offering a relatively modern safety package and partial warranty coverage.

| Comparison Item | New Car | Used Car, 2–3 Year CPO |

|---|---|---|

| 3-Year Depreciation | About 40%–50% | About 15%–25% |

| Typical Loan Rate | About 6%–7% | About 7.5%–10% |

| Annual Insurance Cost | Roughly 4% of vehicle value | Roughly 3.5% of vehicle value |

| Annual Maintenance Cost | $500–$1,000 | $1,000–$2,000 |

| Warranty | Full factory warranty | Remaining factory warranty or CPO extended warranty |

| Safety Technology | Latest driver-assistance features | May lack the newest ADAS features |

Editorial conclusion: If your priority is value, a 2–3 year certified pre-owned car is often the best balance because it has already absorbed the steepest depreciation. If you plan to keep the vehicle for 7+ years and want the newest safety technology, full warranty coverage, and lower early maintenance risk, a new car can still be financially competitive on an annualized cost basis.

Brands with historically strong reliability and resale value, such as Toyota, Honda, and Mazda, often perform well in long-term ownership cost comparisons.

Expert Perspective: Why I Do Not Recommend 72-Month or 84-Month Auto Loans

As a former bank credit analyst, I view 72-month and 84-month auto loans as a warning sign for many buyers. The lower monthly payment feels attractive, but the financial risk is often hidden in three places:

- Slower equity building: During the first few years, most of your early payments are split between interest and a slowly declining principal balance.

- Higher chance of negative equity: Cars depreciate quickly. If your loan balance falls slower than the vehicle’s market value, you become underwater.

- More expensive total interest: A long term may reduce the payment, but it usually increases the total amount paid to the lender.

A practical rule: if you cannot afford the car on a 48–60 month loan, the vehicle may be too expensive for your current budget. For used cars, keeping the term at 48 months or less is often safer because the vehicle is already further along its depreciation curve.

Expert Tips and Cost-Saving Guide

Should You Include Taxes and Fees in the Loan?

The calculator includes an option called “Include Taxes and Fees in Loan.” This choice has a major impact on both your upfront cash requirement and your total interest cost.

| Option | Advantage | Disadvantage | Best For |

|---|---|---|---|

| Do Not Include Taxes and Fees | Lower loan balance and less interest paid | Higher amount due at signing | Buyers with enough cash reserves |

| Include Taxes and Fees | Lower upfront cash requirement | You pay interest on taxes and fees | Buyers who need to preserve short-term cash |

Example: if taxes and fees total $5,500 and you finance them for 36 months at 5% APR, you add about $164.84 to the monthly payment and pay roughly $434 in interest on those taxes and fees alone.

How to Reduce Your Total Car Buying Cost

- Negotiate the out-the-door price: Do not negotiate based on monthly payment. Ask for the full out-the-door price including vehicle price, taxes, registration, dealer fees, and add-ons.

- Get pre-approved before visiting the dealer: Credit unions and banks often beat dealer financing by 0.5%–2%, especially for strong-credit borrowers.

- Keep the loan term reasonable: A 60-month maximum is a practical ceiling for many new cars. For used cars, 48 months or less is often safer.

- Reject unnecessary finance-office add-ons: Extended warranties, VIN etching, fabric protection, rustproofing, and marked-up GAP products can carry very high dealer profit margins.

- Shop at the right time: Month-end, quarter-end, and year-end periods can increase dealer motivation. September through December may be especially useful for outgoing model-year vehicles.

- Compare total cost of ownership: A cheaper vehicle is not always cheaper to own. Insurance, fuel economy, depreciation, repairs, and resale value can change the real 5-year cost.

Auto Loan FAQ and Deep Payment Guide

How much is a $40,000 car payment for 60 months?

Assume a $40,000 vehicle, $5,000 down payment, 7% sales tax, $1,000 in additional fees, and taxes and fees financed into the loan. The estimated financed amount is:

$40,000 - $5,000 + $2,800 sales tax + $1,000 fees = $38,800 financed

Your monthly payment depends heavily on credit score and APR:

| Credit Score Tier | Example APR | Estimated Monthly Payment | Total Interest Over 60 Months | Total Cost Including Down Payment |

|---|---|---|---|---|

| Excellent, 740+ | 5.8% | About $747 | About $6,014 | About $49,814 |

| Good, 700–739 | 6.5% | About $760 | About $6,788 | About $50,588 |

| Fair, 660–699 | 8.5% | About $796 | About $8,972 | About $52,772 |

| Nonprime, 620–659 | 11.5% | About $854 | About $12,422 | About $56,222 |

| Subprime, below 620 | 15.5% | About $933 | About $17,186 | About $60,986 |

The lesson: the same $40,000 car can cost more than $11,000 extra when the borrower moves from excellent credit to subprime credit. Improving your credit score before financing can be more powerful than negotiating a small discount on the vehicle price.

How much is the payment on an $80,000 car?

For an $80,000 vehicle with a $16,000 down payment, 5% APR, and a 60-month term, the estimated monthly payment is about $1,208 before considering sales tax, registration, dealer fees, insurance, and add-ons. In real buying conditions, the payment may be higher if taxes and fees are financed.

Is it better to put more money down on a car?

Usually, yes. A larger down payment reduces the financed balance, lowers total interest, and reduces the risk of becoming upside down on the loan. A down payment of at least 10%–20% is commonly recommended, especially for new cars that depreciate quickly.

Should I choose the lowest monthly payment?

Not always. A lower payment can be created by extending the loan term, increasing the down payment, or rolling fees into the loan. Always compare the total loan interest, total repayment, and payoff date before choosing a financing offer.

What is negative equity?

Negative equity means your loan balance is higher than the vehicle’s market value. This is common when buyers use small down payments, long loan terms, high APRs, or roll old trade-in debt into a new loan.

References

- Consumer Financial Protection Bureau - Auto Loans Guide

- Federal Trade Commission - Car Financing Guide

- USA.gov - Buying a Car

- National Highway Traffic Safety Administration - Buying a New Car

- Federal Reserve - Auto Loan Shopping Guide

Write Reply to This Calculator