Mortgage Prepayment Calculator

Compare lump-sum payoff, extra monthly payments, and biweekly payment schedules.

Mortgage Prepayment Calculator

Calculation Results

Original Schedule

Payment Visualization Comparison

Monthly Amortization Schedule

| Baseline Amortization Schedule | Amortization Schedule with Prepayment | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| Month | Date | Interest | Principal | Payment | End Balance | Interest | Principal | Payment | End Balance |

Expert Mortgage Prepayment Guidance

Mortgage prepayment can be one of the simplest ways to reduce interest and shorten your loan term. But it is not always the best financial move. The right decision depends on your interest rate, cash reserves, other debts, investment alternatives, taxes, and whether your loan has a prepayment penalty.

From a banker's perspective, the best mortgage prepayment strategy is not simply “pay extra whenever you can.” It is to compare the guaranteed return from reducing mortgage interest against the flexibility and potential return of keeping that money elsewhere.

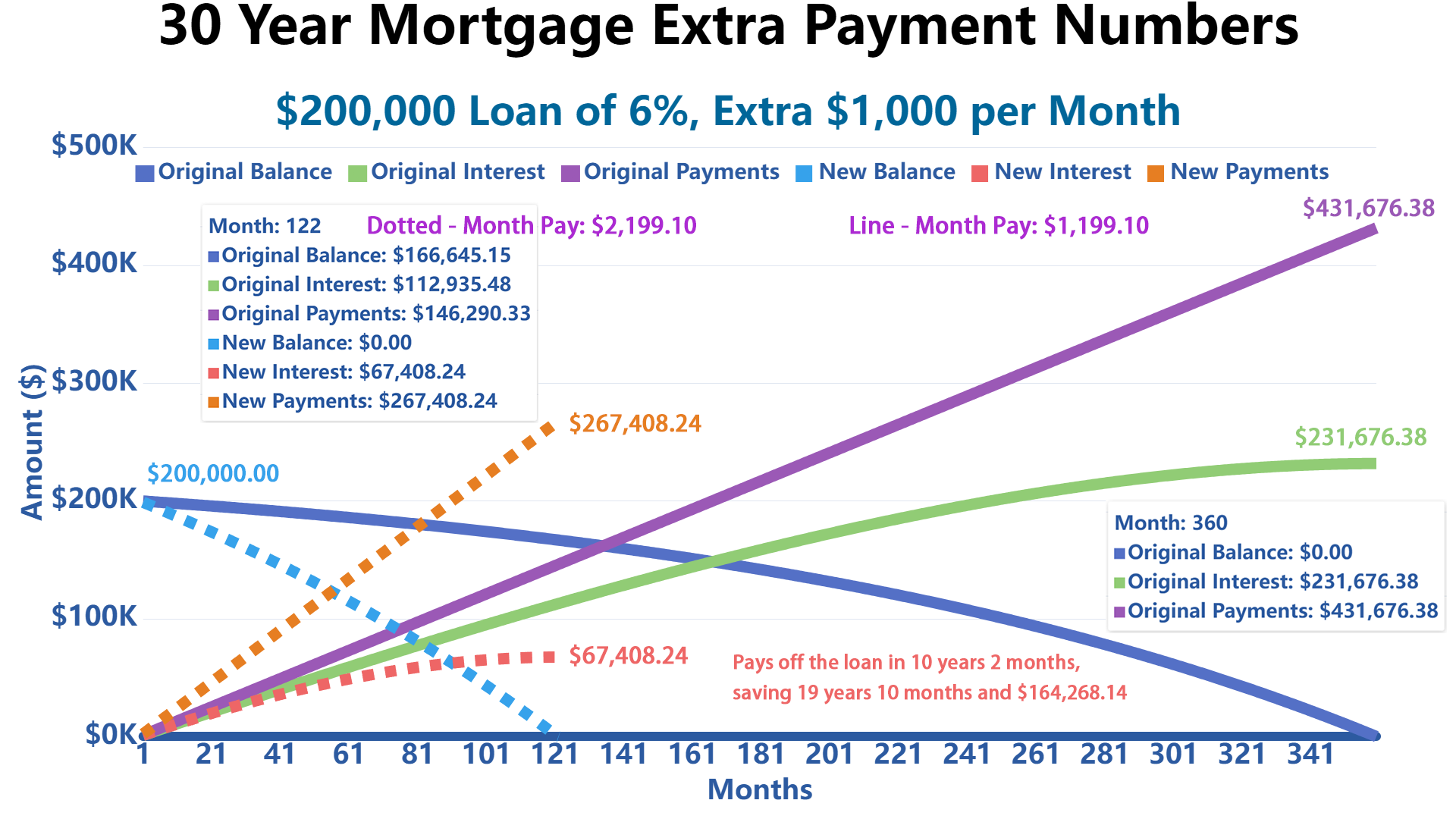

What Happens If I Pay an Extra $1,000 a Month on My Mortgage?

From a banker's perspective, an extra $1,000 per month can be powerful because it directly reduces principal, and every dollar of principal you remove stops future interest from accumulating on that dollar.

For example, on a $200,000 30-year fixed-rate mortgage at a 6% interest rate, the regular monthly principal and interest payment is approximately $1,199.10.

If you pay an extra $1,000 each month, your total monthly payment becomes approximately $2,199.10. In this example, the loan would be paid off in about 10 years and 2 months instead of 30 years.

| Scenario | Estimated Result |

|---|---|

| Original payoff time | 30 years |

| Payoff time with extra $1,000/month | About 10 years and 2 months |

| Time saved | About 19 years and 10 months |

| Estimated interest savings | About $164,268.14 |

This is why large recurring prepayments often produce dramatic savings on long-term fixed-rate mortgages, especially when the interest rate is 6% or higher.

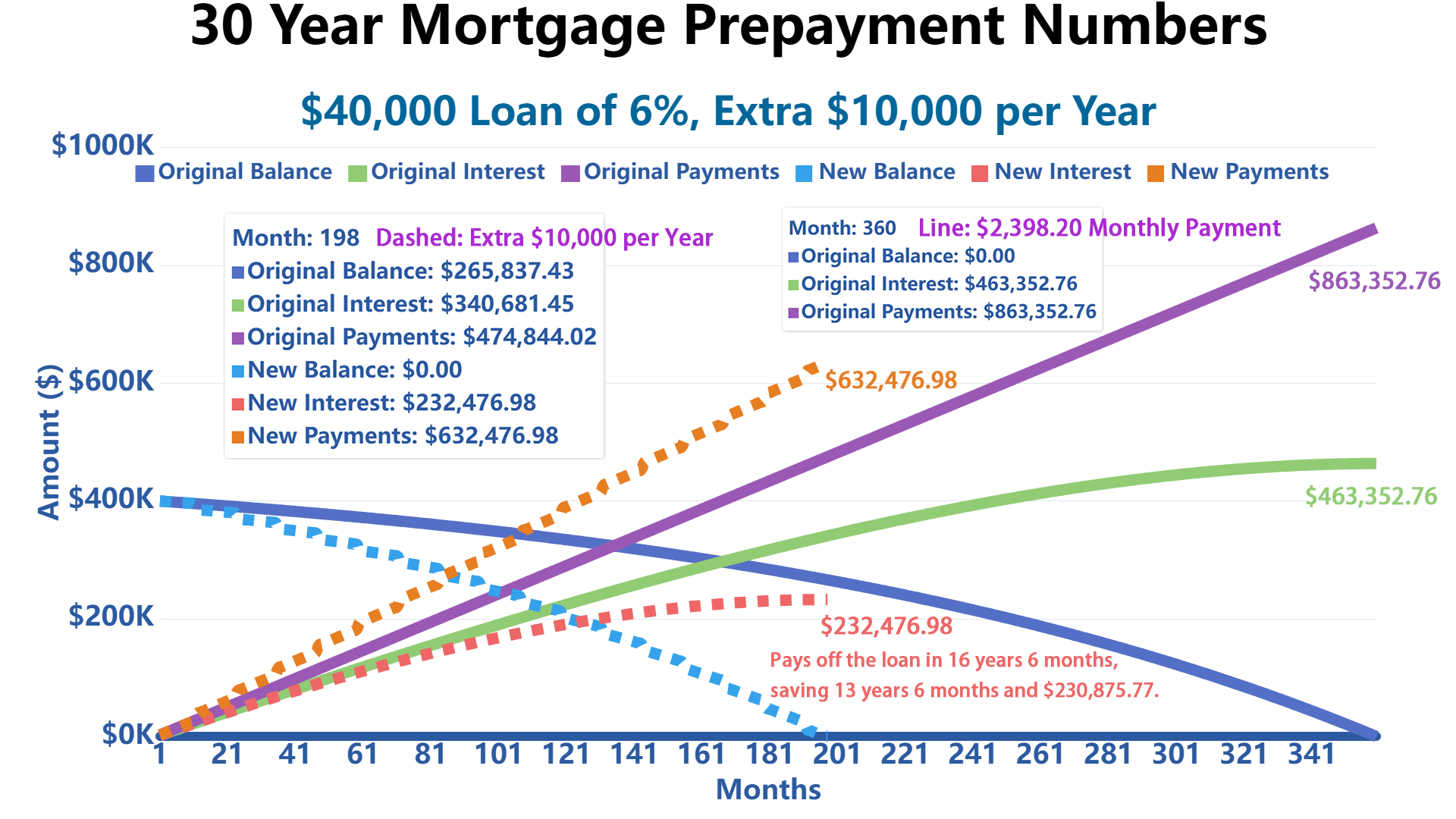

How Many Years Can an Extra $10,000 Annual Payment Take off a Mortgage?

From a banker's perspective, annual lump-sum payments work best when they are applied directly to principal and made early in the loan term. The earlier the extra payment is made, the more future interest it can eliminate.

For example, assume you have a $400,000 mortgage at 6% for 30 years. Without extra payments, the loan runs for the full 30 years. If you make an extra $10,000 principal payment every year, the payoff time could fall to about 16 years and 6 months.

| Scenario | Estimated Result |

|---|---|

| Original loan amount | $400,000 |

| Interest rate | 6% |

| Original loan term | 30 years |

| Extra annual payment | $10,000 |

| Estimated payoff time | About 16 years and 6 months |

The key is to confirm that your lender applies the extra $10,000 to principal, not to future scheduled payments.

Is It Worth Overpaying My Mortgage by $100 a Month?

From a banker's perspective, yes, even a small extra payment can be meaningful over time because mortgage interest compounds across decades. A $100 monthly prepayment may not feel dramatic, but it can quietly remove years of interest from a long-term loan.

For example, on a $300,000 30-year fixed-rate mortgage at 6%, the standard monthly principal and interest payment is approximately $1,798.65. Over the full 30 years, total interest would be approximately $347,514.

If you pay an extra $100 per month, for a total monthly payment of approximately $1,898.65, the loan would be paid off in about 27 years and 1 month. That means you could save roughly 2 years and 11 months and reduce total interest by approximately $45,000.

| Scenario | Estimated Result |

|---|---|

| Loan amount | $300,000 |

| Interest rate | 6% |

| Original monthly payment | About $1,798.65 |

| Monthly payment with extra $100 | About $1,898.65 |

| Estimated payoff time | About 27 years and 1 month |

| Estimated time saved | About 2 years and 11 months |

| Estimated interest savings | About $45,000 |

The practical takeaway: a $100 monthly prepayment is especially attractive if your mortgage rate is higher than what you can safely earn after tax elsewhere, and if you already have an emergency fund.

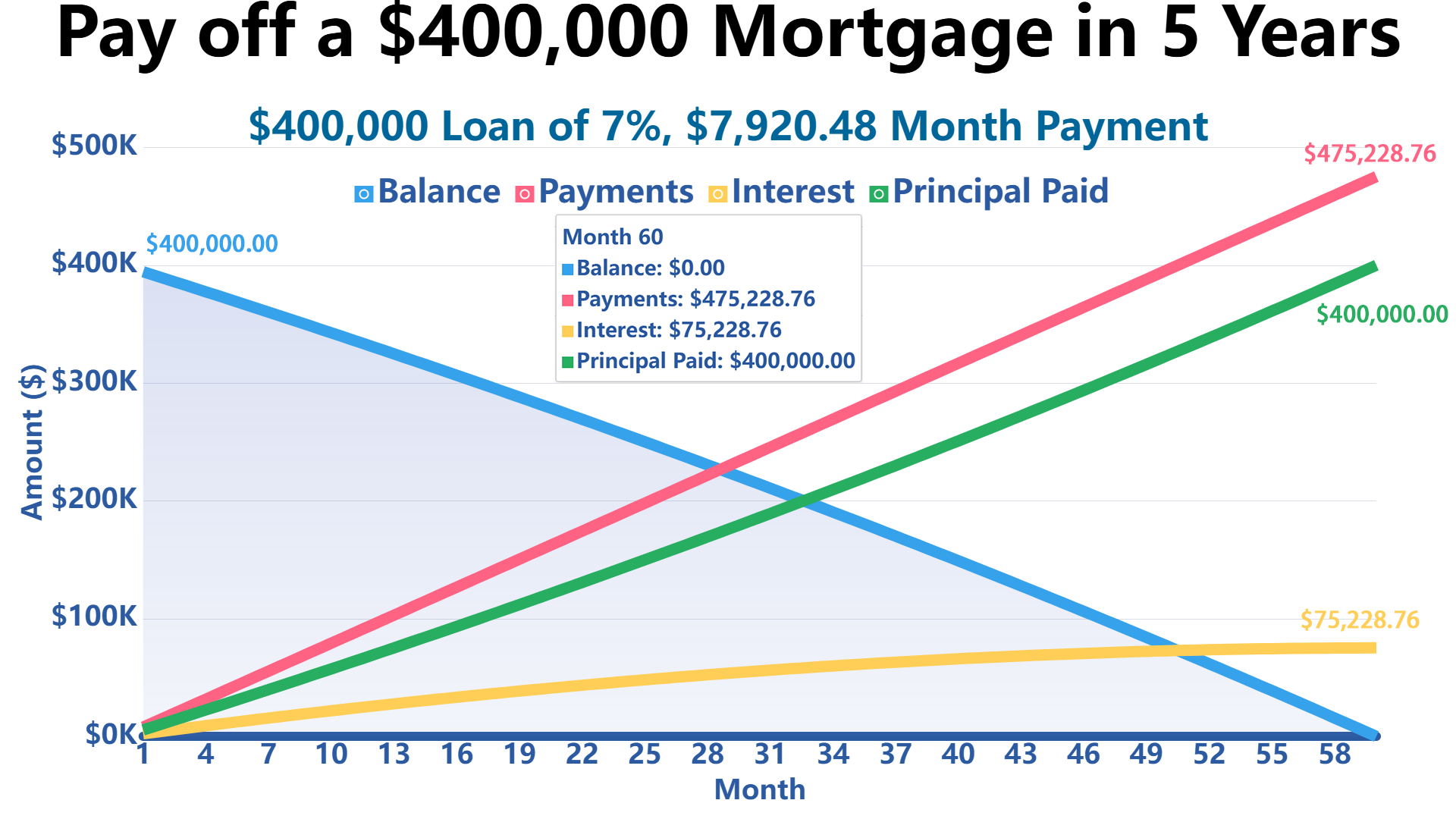

How to Pay off a $400,000 Mortgage in 5 Years

From a banker's perspective, paying off a $400,000 mortgage in 5 years is not a prepayment strategy for most households. It is an aggressive cash-flow commitment that should be tested against income stability, emergency reserves, retirement contributions, and tax planning.

If your mortgage interest rate is 7% APR and you want to fully repay $400,000 in 5 years, the required monthly principal and interest payment would be approximately $7,920.48.

| Input | Example |

|---|---|

| Mortgage balance | $400,000 |

| Target payoff period | 5 years |

| Interest rate | 7% |

| Required monthly payment | About $7,920.48 |

Before committing to this plan, stress-test your household budget. A fast payoff can be financially rewarding, but becoming cash-poor in the process can create avoidable risk.

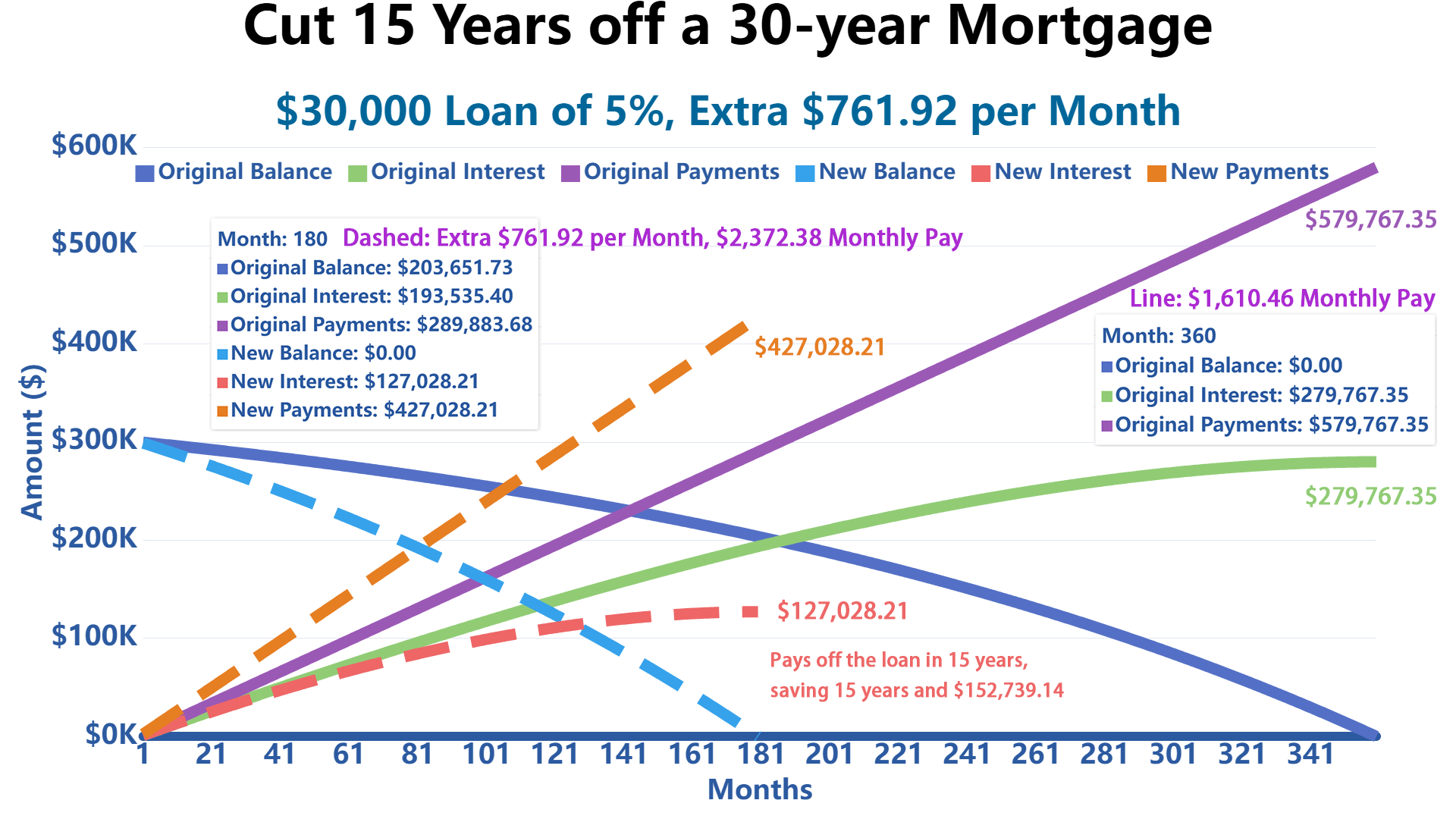

How to Cut 15 Years off a 30-Year Mortgage

From a banker's perspective, there are two common ways to cut 15 years off a 30-year mortgage: refinance into a 15-year loan or make your own accelerated payments while keeping the original 30-year mortgage.

Refinancing into a 15-year loan can force discipline and may offer a lower rate, but it also locks you into a higher required payment. Making extra payments on a 30-year mortgage gives you more flexibility because you can reduce or pause the extra payment if your finances change.

For example, if you have a $300,000 mortgage at 5% for 30 years, the standard monthly principal and interest payment is approximately $1,610.46. Paying approximately $2,372.38 per month instead could reduce the payoff period to about 15 years, depending on loan terms and payment timing.

| Scenario | Estimated Result |

|---|---|

| Original loan | $300,000 at 5% for 30 years |

| Standard monthly payment | About $1,610.46 |

| Accelerated monthly payment | About $2,372.38 |

| Extra monthly amount | About $761.92 |

| Estimated payoff period | About 15 years |

Real Client Case Study: When Prepaying Too Fast Backfired

The biggest mistake is not prepaying. The biggest mistake is prepaying without looking at the whole balance sheet.

In my 15 years of banking experience, I once worked with an anonymized client who had a mortgage near 7%. After receiving a large bonus, the client wanted to put nearly all of it toward the mortgage. At first glance, that seemed logical: a 7% guaranteed interest saving is attractive.

But after reviewing the full financial picture, we found three issues:

- No emergency cushion: The client had less than two months of expenses in cash reserves.

- High-interest credit card debt: Part of the household debt carried an interest rate above 18%.

- Potential prepayment charge: The mortgage had a penalty clause during the early years of the loan.

The better decision was to first pay off the credit card debt, build a six-month emergency fund, confirm the prepayment penalty with the lender, and then apply a smaller recurring amount toward the mortgage principal.

The lesson: mortgage prepayment should not be judged by the mortgage rate alone. Liquidity, debt hierarchy, penalty rules, and opportunity cost matter just as much.

Mortgage Prepayment Decision Tree

From a banker's perspective, use this decision tree before making extra mortgage payments.

Start | |-- Do you have high-interest debt above your mortgage rate? | |-- Yes: Pay that debt first. | |-- No: Continue. | |-- Do you have 3-6 months of emergency savings? | |-- No: Build cash reserves first. | |-- Yes: Continue. | |-- Does your loan have a prepayment penalty? | |-- Yes: Calculate the penalty before prepaying. | |-- No: Continue. | |-- Is your mortgage rate higher than your safe after-tax alternative return? | |-- Yes: Prepayment may be attractive. | |-- No: Investing or saving may be better. | |-- Are you on track for retirement contributions and employer match? | |-- No: Capture retirement benefits first. | |-- Yes: Consider regular principal prepayments.

Prepayment Penalty and Policy Checklist

The prepayment penalty is one of the most overlooked details in mortgage planning. Many borrowers focus only on interest savings and forget that the lender may charge a fee if the loan is paid down or paid off too early.

Before making a large extra payment, refinancing, or selling the home, review your loan documents or contact your servicer and ask these questions:

| Checklist Item | What to Confirm |

|---|---|

| Penalty period | Does the penalty apply only during the first 1, 2, 3, or 5 years? |

| Trigger event | Does the penalty apply to extra payments, refinancing, selling the home, or full payoff? |

| Soft vs. hard penalty | A soft penalty may apply only to refinancing, while a hard penalty may apply to both refinancing and selling. |

| Allowed annual prepayment | Can you prepay up to a certain percentage each year without penalty? |

| Calculation method | Is the penalty based on months of interest, a percentage of balance, a flat fee, or an interest rate differential? |

| Principal application | Will the extra payment be applied directly to principal? |

| Recast option | Can the lender recast the loan after a lump-sum payment to lower the monthly payment? |

| Written confirmation | Can the lender provide a payoff or prepayment quote in writing? |

Prepayment penalties vary by lender, loan type, and jurisdiction. Some modern residential mortgages do not include them, while certain commercial, investment, jumbo, or specialized loans may still use them. Always check your actual loan agreement before making a large prepayment.

How Prepayment Penalties Are Commonly Calculated

A prepayment penalty is the lender's way of recovering some of the interest income it expected to earn. The exact method depends on your contract.

| Penalty Type | How It Works |

|---|---|

| Percentage of balance | The lender charges a percentage of the remaining loan balance, such as 1% or 2%. |

| Months of interest | The lender charges a set number of months of interest, such as 3 or 6 months. |

| Step-down schedule | The penalty decreases over time, such as 3% in year one, 2% in year two, and 1% in year three. |

| Interest rate differential | The lender compares your contract rate with current rates and charges part of the difference. |

| Yield maintenance or defeasance | Common in commercial real estate loans and can be complex and expensive. |

Example: If your remaining mortgage balance is $250,000 and your penalty is 2% of the balance, the prepayment penalty would be approximately $5,000. If prepaying would save you $8,000 in interest, the net benefit may still be positive. But if the penalty is $12,000, prepaying may not make sense.

Dynamic Opportunity Cost: Should I Prepay or Invest?

From a banker's perspective, every extra dollar sent to your mortgage has an opportunity cost. Once you prepay, that money is no longer available for an emergency fund, retirement account, business investment, or liquid savings.

A simple way to compare choices is:

Prepayment advantage = Mortgage rate - Safe after-tax alternative return - Estimated penalty cost rate

If the result is positive, prepayment may be financially attractive. If the result is negative, keeping the money liquid or investing it may be better.

Example Opportunity Cost Comparison

Assume your mortgage rate is 6.5%. Also assume a safe alternative, such as short-term U.S. Treasury bills or a high-yield savings product, is yielding around 4.5% before tax. If your combined tax rate is 24%, the after-tax return is approximately:

4.5% × (1 - 24%) = 3.42%

Now compare:

| Item | Example Rate |

|---|---|

| Mortgage interest rate | 6.50% |

| Safe alternative yield before tax | 4.50% |

| Estimated after-tax alternative return | 3.42% |

| Estimated prepayment advantage before penalties | About 3.08% |

In this example, mortgage prepayment looks attractive because the guaranteed interest saving of 6.5% is higher than the estimated after-tax safe return of 3.42%. But if your mortgage rate were only 3%, and your after-tax safe return were 3.42%, prepayment would be less compelling.

Use this formula as a decision framework, not as personal financial advice. Treasury yields, savings rates, taxes, and mortgage rates change over time, so the comparison should be updated before making a major lump-sum payment.

When Should I Not Make Mortgage Prepayments?

From a banker's perspective, mortgage prepayment is usually not the first priority if it weakens your overall financial position. Consider delaying extra mortgage payments in the following situations.

| Situation | Banker's View |

|---|---|

| High-interest debt | If credit cards, personal loans, or other debts carry higher rates than your mortgage, pay those first. |

| Insufficient emergency fund | If you do not have at least 3-6 months of expenses saved, liquidity should usually come first. |

| Employer retirement match not captured | If your employer offers a 401(k) match, contributing enough to receive the match may be more valuable than prepaying. |

| Low mortgage rate | If your mortgage rate is lower than your safe after-tax alternative return, prepayment may not be optimal. |

| Prepayment penalty applies | If the penalty is larger than the expected interest savings, waiting may be smarter. |

| Upcoming major cash needs | If you expect tuition, medical costs, business expenses, or relocation costs, keeping cash may be safer. |

| Tax planning considerations | If you deduct mortgage interest, compare the after-tax cost of the mortgage before deciding. |

Banker's Rule of Thumb

From a banker's perspective, the cleanest prepayment decision is when all five conditions are true:

- Your mortgage rate is meaningfully higher than your safe after-tax alternative return.

- You have no higher-interest debt.

- You already have an adequate emergency fund.

- You are receiving any available employer retirement match.

- Your loan has no costly prepayment penalty.

If those conditions are met, extra principal payments can be a disciplined, low-risk way to reduce interest expense and become mortgage-free faster.

Important Notes Before You Prepay

The small operational details matter. Before sending extra money, confirm the following with your lender or loan servicer:

- Mark the payment as principal-only. Otherwise, the payment may be treated as a future scheduled payment.

- Confirm there is no prepayment penalty. Ask for the answer in writing if you plan to make a large lump-sum payment.

- Ask whether a recast is available. A recast may lower your monthly payment after a large principal reduction.

- Keep proof of payment. Save confirmations showing the amount and how the payment was applied.

- Recalculate after major life changes. A new job, child, business purchase, or relocation can change the best strategy.

References

For more information on mortgage rates, prepayment strategies, and financial advice, please visit:

Write Reply to This Calculator