Student Loan Early Payoff Calculator

Calculate Savings & Payoff Time With Extra Payments

Student Loan Early Payoff Calculator

($)

($)

(%)

($) per month

($) per year

($) one time

Calculation Results

If Accelerated Repayment

Monthly Pay

Total Payments

Remaining Interest

Additional Payments

Remaining Term

Interest Savings

Time Saved

Standard Schedule

Monthly Pay

Remaining Principal

Remaining Payments

Remaining Interest

Remaining Term

Payment Visualization Comparison

Monthly Amortization Schedule

| Baseline Amortization Schedule | Amortization Schedule with Prepayment | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| Month | Date | Interest | Principal | Payment | End balance | Interest | Principal | Payment | End balance |

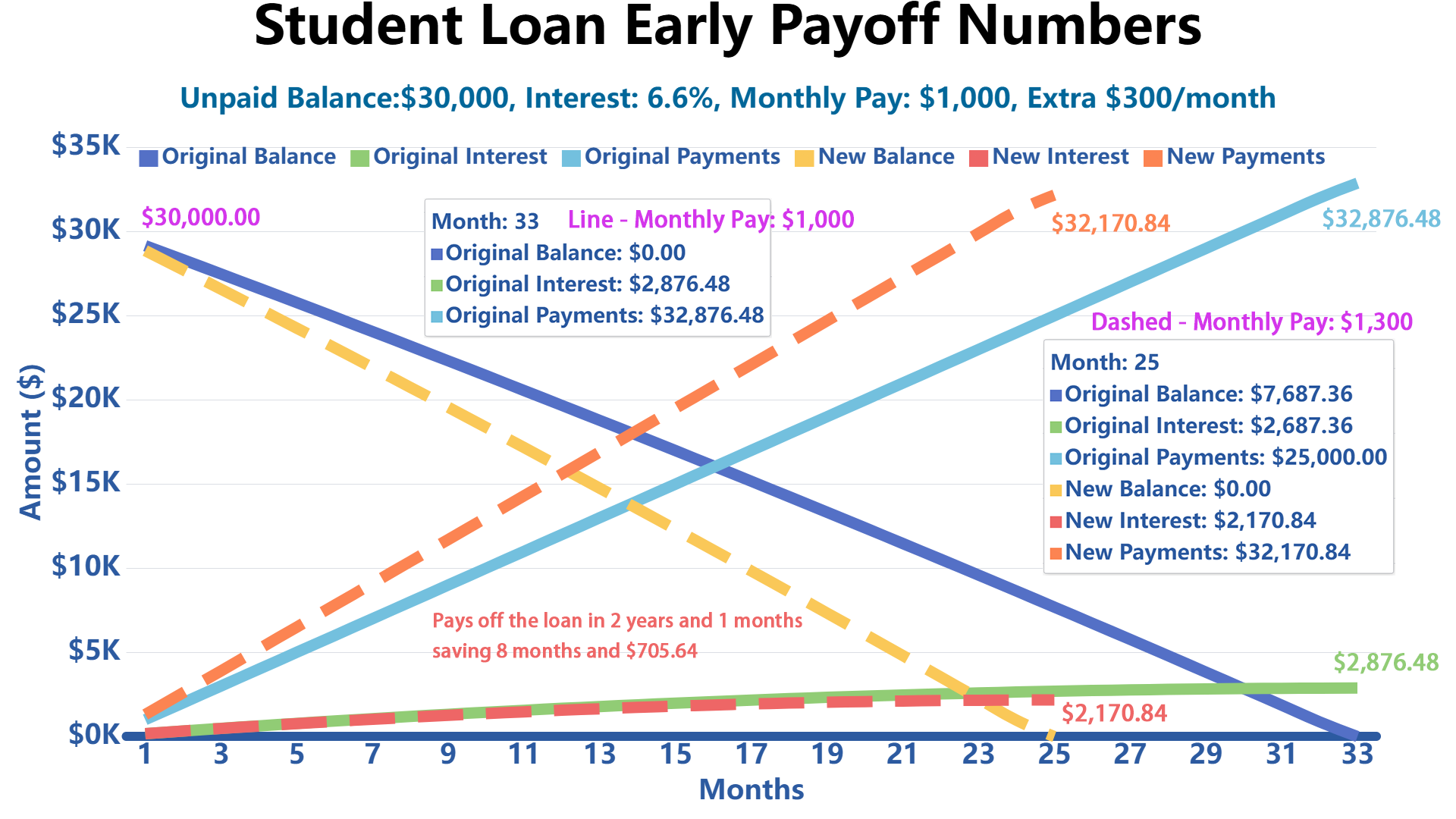

What Happens If I Increase My Monthly Payment From $1,000 to $1,300 on a $30,000 Loan With 6.6% Interest?

If you pay an extra $300 each month, bringing your total to $1300, you'll pay off the entire loan in just 2 years 1 months.

That's 8 months earlier than the original schedule, and you'll save a whopping $705.64 in interest.

FAQ

Should I Pay off Student Loans or Invest?

This depends on your loan interest rate and expected investment returns. Generally, if your loan rate is above 6-7%, prioritize loan repayment. For lower rates, investing may provide better long-term returns, especially with tax-advantaged accounts.

References

This calculator and information are based on standard financial formulas and federal student loan guidelines. For official information and personalized advice, consult these authoritative sources:

- Federal Student Aid - U.S. Department of Education

- Consumer Financial Protection Bureau - Student Loans

- IRS - Student Loan Interest Deduction

- National Student Loan Data System

- Federal Reserve - Student Loan Statistics

Related

Write Reply to This Calculator