Mortgage Payoff Calculator

Calculate savings from extra payments, biweekly schedules

Mortgage Payoff Calculator

Calculation Results

If Accelerated Repayment

Standard Schedule

Payment Visualization Comparison

Monthly Amortization Schedule

| Baseline Amortization Schedule | Amortization Schedule with Prepayment | ||||||||

|---|---|---|---|---|---|---|---|---|---|

| Month | Date | Interest | Principal | Payment | End Balance | Interest | Principal | Payment | End Balance |

How to Make Sure Extra Mortgage Payments Actually Reduce Principal

Making an extra mortgage payment is not always enough. In many servicing systems, an additional payment may be treated as a payment toward your next bill unless you clearly instruct the loan servicer to apply it to principal.

Before sending extra money, use this practical process:

- Confirm your loan servicer's extra-payment rules. Ask whether extra payments are automatically applied to principal or held as a future scheduled payment.

- Use the correct payment channel. Many servicers have a separate field labeled “Additional Principal,” “Principal Only,” or “Curtailment.” Use that field whenever available.

- Add a written instruction. If paying online, by check, or through bill pay, include a note such as: “Apply this additional amount to principal only. Do not apply it to future scheduled payments.”

- Check the next statement. After the payment posts, verify that the principal balance dropped by the expected amount.

- Keep records. Save confirmation numbers, screenshots, payment receipts, and monthly statements in case the payment needs to be corrected later.

Qiu's Insight

In my banking experience, this is one of the most common mistakes borrowers make. They send extra money with good intentions, but the servicing system treats it as a prepaid installment instead of a principal reduction. The difference matters because only principal reduction cuts future interest.

Expert Reminder: 3 Questions to Ask Your Bank Before Prepaying

Before making a large extra payment, call your lender or loan servicer and ask these three questions. The answers can change the best strategy for your situation.

| Question | Why It Matters | What to Confirm |

|---|---|---|

| Is there a prepayment penalty? | Some loans charge a fee if you pay off too much principal too early. | Ask whether the penalty applies to partial prepayments, full payoff, refinancing, or selling the home. |

| Will my extra payment go directly to principal? | Extra money may be applied to future installments instead of reducing your loan balance. | Confirm the exact instruction or payment option required for “principal-only” payments. |

| Can I recast the mortgage after a large prepayment? | A recast may lower your monthly payment while keeping the same interest rate and maturity structure. | Ask about eligibility, fees, minimum principal reduction, and whether recasting changes the payoff timeline. |

Important: A mortgage recast is different from refinancing. A recast usually keeps the same loan and interest rate, while refinancing replaces the loan with a new one.

Anonymized Case Studies: How Real Borrowers Used Prepayment Strategies

The following examples are anonymized and simplified for educational purposes. Actual savings depend on the loan balance, rate, payment timing, escrow rules, loan type, and servicer policies.

Case Study 1: Mr. Zhang Chose Term Reduction Instead of Lower Monthly Payments

Mr. Zhang had a fixed-rate mortgage and was in the fifth year of repayment. After receiving a work bonus, he planned to make a one-time principal payment of $50,000. His first thought was to lower the monthly payment, but after reviewing the numbers, the stronger option was to keep the same monthly payment and shorten the remaining term.

| Item | Before Prepayment | After Principal Reduction Strategy |

|---|---|---|

| Remaining balance | About $360,000 | About $310,000 after one-time prepayment |

| Interest rate | 5.75% | 5.75% |

| Monthly payment | Kept unchanged | Kept unchanged |

| Main result | Standard remaining schedule | Shorter payoff timeline and lower total interest |

By applying the lump sum directly to principal and keeping the original monthly payment, Mr. Zhang accelerated his payoff schedule. In this type of scenario, borrowers often save tens of thousands of dollars in interest compared with simply reducing the monthly payment.

Qiu's Insight

When clients can comfortably afford the current monthly payment, I often review the “shorten the term” option first. Lowering the monthly payment improves cash flow, but keeping the payment the same usually creates larger interest savings.

Case Study 2: A Homeowner's Extra Payments Were Misapplied

A homeowner made an extra $600 payment every month for nearly a year. The borrower believed the money was reducing principal, but the mortgage statement showed the loan was simply paid ahead. The servicer had been applying the extra money toward future monthly installments.

After contacting the servicer and correcting the payment instructions, future extra payments were applied as “principal only.” The borrower also requested a review of previous payments and asked whether any prior amounts could be reclassified.

| Problem | Correction | Lesson |

|---|---|---|

| Extra payments were treated as future scheduled payments. | The borrower added “apply to principal only” instructions. | Always verify your monthly statement after making extra payments. |

| The principal balance did not fall as expected. | The borrower contacted the servicer and requested clarification. | Do not assume extra money automatically reduces principal. |

Qiu's Insight

This is why I recommend checking the statement after every major prepayment. The principal balance should drop by more than it would under the regular amortization schedule. If it does not, contact the servicer immediately.

Is It a Good Idea to Prepay a Mortgage?

Prepaying a mortgage can be a smart move when your priority is reducing debt, lowering future interest, and gaining financial flexibility. However, it is not automatically the best choice for every borrower.

In my banking experience, I usually encourage borrowers to review four things before committing extra cash to the mortgage: emergency savings, high-interest debt, investment alternatives, and loan terms. If you have credit card debt, no emergency fund, or a loan with a low fixed rate, aggressive prepayment may not be your best first move.

Qiu's Insight

Mortgage prepayment is most powerful when the borrower has stable income, sufficient cash reserves, and no higher-cost debt. The goal is not just to pay faster. The goal is to improve the household balance sheet without creating liquidity pressure.

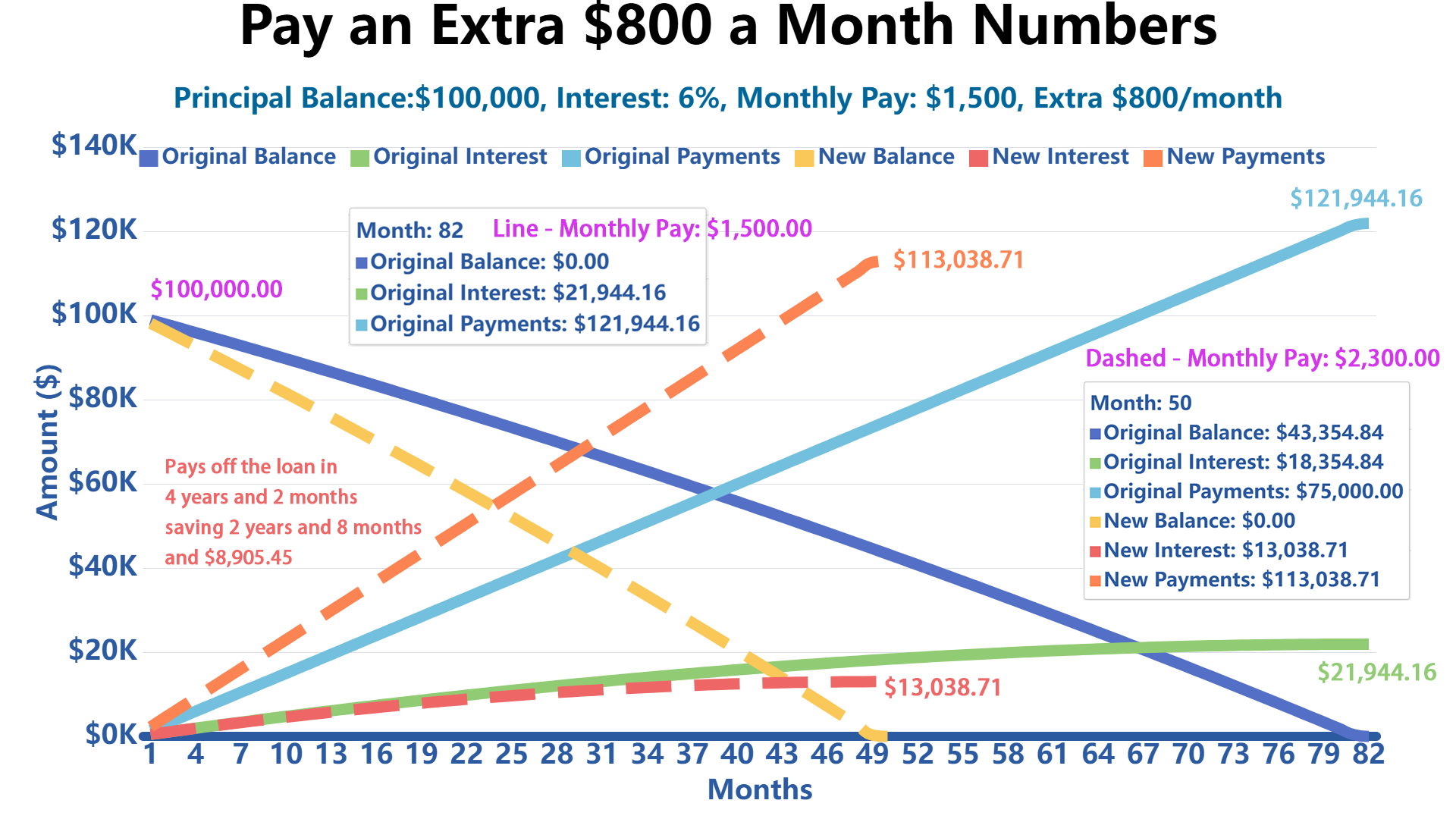

Is It Worth Paying an Extra $800 a Month on Your Mortgage?

Paying an extra $800 per month can create meaningful interest savings, especially when the loan rate is relatively high and the extra amount is applied directly to principal.

For example, if you have a $100,000 principal balance, a $1,500 monthly payment, and a 6% annual interest rate, adding $800 per month could save roughly $8,905.45 in interest and shorten the loan by about 2 years and 8 months.

Qiu's Insight

When a borrower asks whether an extra $800 is “worth it,” I do not look only at the interest savings. I also ask whether that $800 could be needed for emergency savings, insurance deductibles, repairs, tuition, or higher-interest debt. A strategy that looks good mathematically still has to work in real life.

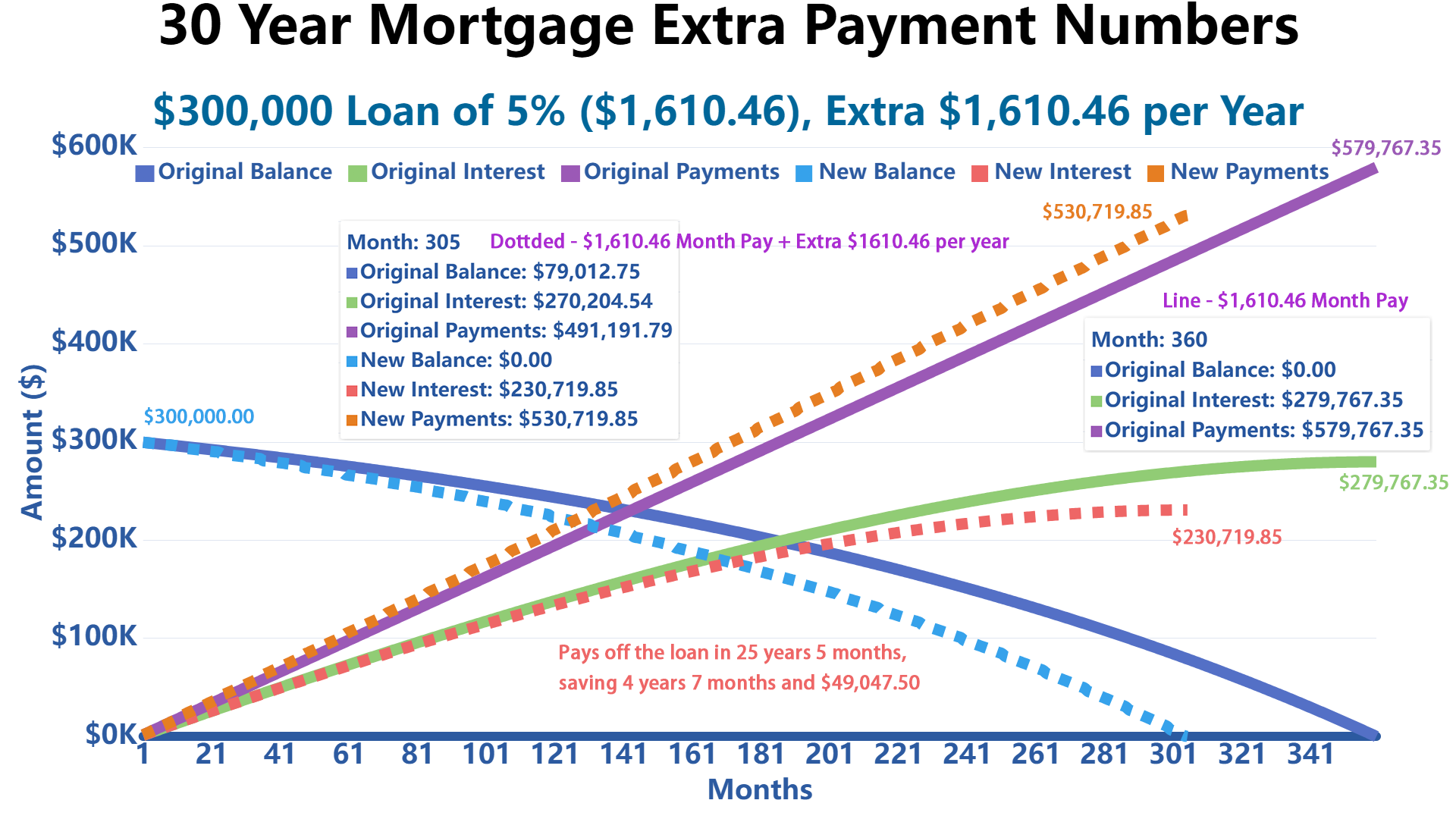

How Many Years Does One Extra Payment Take Off a 30-Year Mortgage?

Making one extra mortgage payment per year can often reduce a 30-year mortgage by about 4 to 6 years, depending on the loan amount, interest rate, and when the extra payments begin.

Example:

- Loan amount: $300,000

- Interest rate: 5% fixed

- Monthly payment: $1,610.46

Scenario 1: Regular payments

You pay $1,610.46 every month for 30 years. The loan is fully paid off at the end of the scheduled term.

Scenario 2: One extra payment per year

You make one additional payment of $1,610.46 each year, which is similar to making 13 monthly payments annually instead of 12.

Result: This strategy can reduce the loan term by approximately 4 years and 8 months, meaning the mortgage may be paid off in about 25 years and 5 months instead of 30 years. It may also save about $49,048.32 in interest over the life of the loan.

Qiu's Insight

The earlier you start extra annual payments, the more powerful the result. Extra principal paid in the first half of the loan usually saves more interest than the same amount paid near the end of the loan.

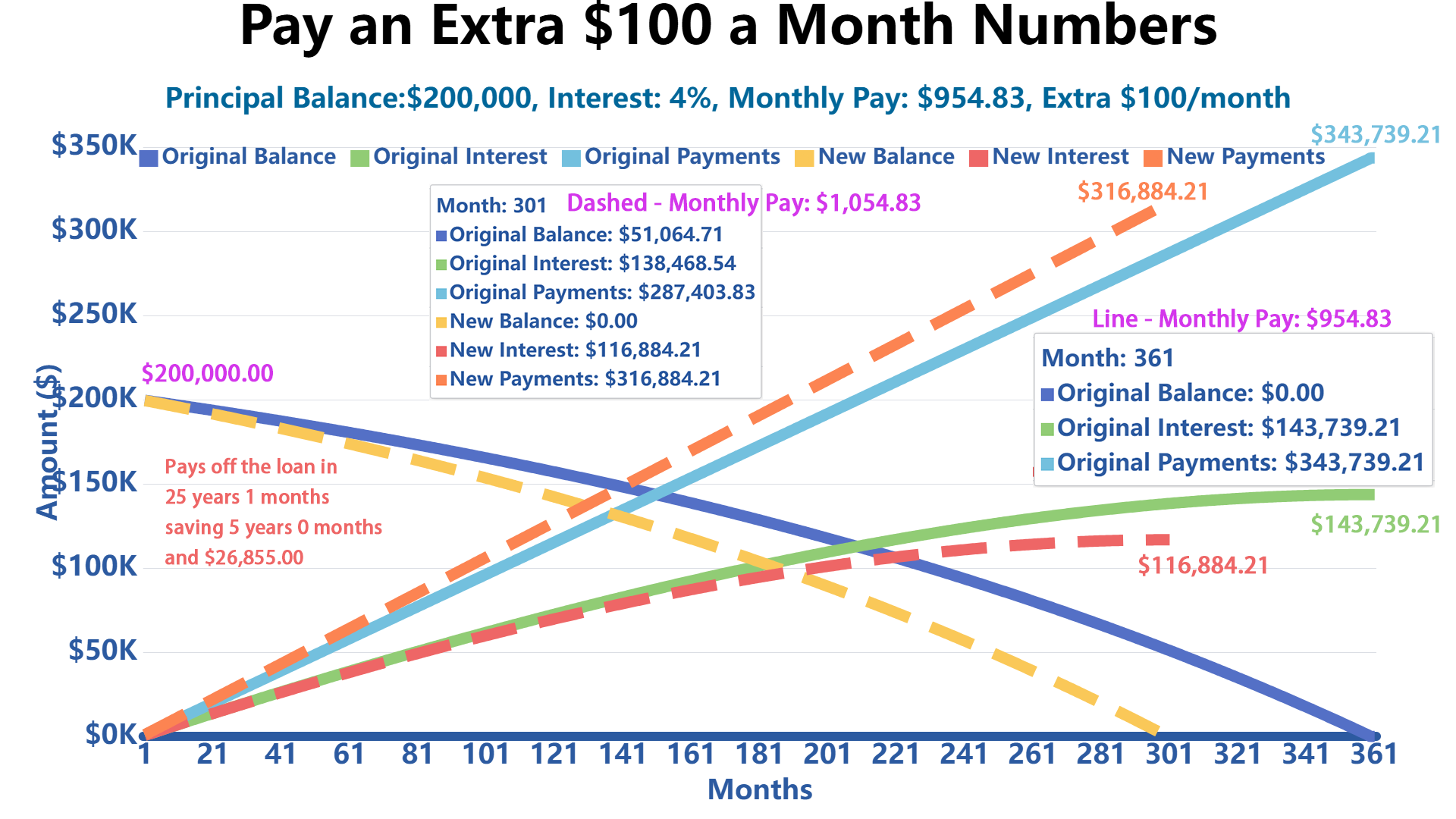

What Happens if I Pay an Extra $100 a Month on My Mortgage Principal?

Paying an extra $100 per month toward principal reduces your balance faster, shortens the loan term, and lowers total interest paid over time. Even a small recurring amount can have a noticeable long-term effect.

Example:

- Loan amount: $200,000

- Interest rate: 4% fixed

- Loan term: 30 years

- Regular monthly payment: about $954.83

If you pay an extra $100 each month, for a total monthly payment of about $1,054.83, you could pay off the mortgage about 5 years earlier and save approximately $26,855 in interest over the life of the loan.

Qiu's Insight

I often tell borrowers that consistency matters more than size. A manageable $100 monthly principal payment that you can maintain for years may be better than an aggressive prepayment plan that strains your cash flow and gets abandoned after a few months.

Mortgage Prepayment FAQ

Should I reduce my monthly payment or shorten my loan term?

If your goal is maximum interest savings, shortening the loan term usually produces the stronger result. If your goal is monthly cash-flow relief, reducing the payment through a recast may be more useful.

Qiu's Insight

In my 15 years of banking experience, I have seen both strategies work well for different borrowers. Clients with strong cash flow often benefit from term reduction, while clients preparing for lower income, retirement, or family expenses may prefer a lower required monthly payment.

Does biweekly payment really save money?

Yes, a true biweekly payment plan can save interest because you make 26 half-payments per year, which equals 13 full monthly payments. That extra annual payment reduces principal faster.

However, some third-party biweekly programs charge fees. Before enrolling, compare the cost of the program with simply making one extra principal payment yourself each year.

Qiu's Insight

I generally prefer simple, transparent strategies. If your servicer lets you make principal-only payments for free, you may not need a paid biweekly program.

Will prepaying my mortgage lower my monthly payment automatically?

Usually, no. A principal prepayment lowers your balance and interest cost, but your required monthly payment often stays the same unless your loan is recast, refinanced, or otherwise modified by the lender.

Qiu's Insight

This surprises many borrowers. Paying extra principal helps you pay off the loan sooner, but it does not always lower the bill due next month.

Is it better to prepay the mortgage or invest?

It depends on your mortgage rate, investment return expectations, tax situation, risk tolerance, and liquidity needs. Prepaying a mortgage provides a predictable interest-saving benefit. Investing may offer higher long-term returns, but it also carries market risk.

Qiu's Insight

I usually frame this as a risk decision, not just a return decision. Prepayment is like earning a guaranteed return equal to the interest you avoid, while investing introduces uncertainty and requires discipline during market volatility.

Can I get my extra mortgage payment back later?

Usually, no. Once an extra payment is applied to principal, that money becomes home equity. You may be able to access equity later through a refinance, home equity loan, or HELOC, but those options require approval and may involve fees or higher rates.

Qiu's Insight

This is why I rarely recommend using all available cash for prepayment. Home equity is valuable, but it is not the same as money in a savings account.

Write Reply to This Calculator