Mortgage Affordability Calculator

Calculate how much house you can afford based on monthly budget

Mortgage Affordability Calculator

Calculation Results

Monthly Payment Breakdown and Total Cost Analysis

| Item | Monthly | Total |

|---|---|---|

| Mortgage Payment | \$0.00 | \$0.00 |

| Property Tax | \$0.00 | \$0.00 |

| Home Insurance | \$0.00 | \$0.00 |

| PMI | \$0.00 | \$0.00 |

| HOA Fee | \$0.00 | \$0.00 |

| Maintenance cost | \$0.00 | \$0.00 |

| Total Housing Cost | \$0.00 | \$0.00 |

Total Cost of Homeownership Distribution

Mortgage Payment Amortization Schedule

| Year | Principal | Interest | Payments | End Balance |

|---|

| Month | Principal | Interest | Payment | End Balance |

|---|

Regional Tax and Insurance Traps Buyers Often Miss

Two homes with the same purchase price can have very different monthly payments depending on the state, county, insurance market, and local tax rules. This is why a national mortgage affordability estimate should always be adjusted for location.

| State | Median Home Price | Median Income | Price-to-Income Ratio | Estimated Property Tax Rate |

|---|---|---|---|---|

| California | $785,000 | $91,500 | 8.6x | 0.74% |

| Hawaii | $720,000 | $88,000 | 8.2x | 0.28% |

| Massachusetts | $595,000 | $96,500 | 6.2x | 1.23% |

| New York | $430,000 | $78,000 | 5.5x | 1.72% |

| Washington | $575,000 | $90,000 | 6.4x | 1.03% |

| New Jersey | $480,000 | $89,000 | 5.4x | 2.47% |

| Florida | $400,000 | $67,000 | 6.0x | 0.86% |

| Texas | $340,000 | $73,000 | 4.7x | 1.80% |

| Arizona | $420,000 | $72,500 | 5.8x | 0.62% |

| Georgia | $350,000 | $66,000 | 5.3x | 0.92% |

| Illinois | $260,000 | $74,000 | 3.5x | 2.23% |

| North Carolina | $340,000 | $65,000 | 5.2x | 0.84% |

| Virginia | $385,000 | $85,000 | 4.5x | 0.82% |

| Ohio | $210,000 | $62,000 | 3.4x | 1.56% |

| Indiana | $230,000 | $63,000 | 3.7x | 0.85% |

For example, California has a high median home price but a relatively lower property tax rate. Texas often has a lower home price than California, but its property tax rate can be much higher. New Jersey and Illinois are also good examples of states where property taxes can materially change the affordability calculation.

Insurance is another regional trap. In coastal states, wildfire zones, hurricane-prone areas, or regions with rising replacement costs, homeowners insurance may be far higher than the default estimate. Before making an offer, request a real insurance quote for the specific property address.

Case Study: How a Family Earning $8,000 per Month Could Buy a $430,000 Home

This simulated case study shows how a household can use the calculator to move from a rough budget to a more realistic home-buying decision.

Buyer Profile

- Gross monthly income: $8,000

- Target home price: $430,000

- Down payment: 20%, or $86,000

- Loan amount: $344,000

- Loan term: 30 years

- Estimated interest rate: 6.5%

- Estimated property tax: 1.2% per year

- Estimated homeowners insurance: 0.5% per year

- Estimated maintenance reserve: 1.5% per year

What the Calculator Reveals

At a 6.5% interest rate, the principal and interest payment on a $344,000 loan is roughly $2,174 per month. But that is not the full cost of owning the home. Property tax, insurance, and maintenance reserves may add another $1,147 per month, bringing the estimated full housing cost to about $3,321 per month.

On an $8,000 gross monthly income, that full housing payment equals about 41.5% of gross income before counting car loans, student loans, credit cards, childcare, or retirement contributions. A bank might still evaluate the file depending on the borrower’s full profile, but from a household cash-flow perspective, this would be a tight purchase unless the family has low other debts and strong emergency savings.

The Decision

Instead of asking, “Can we technically buy a $430,000 home?” the better question is, “Can we own this home without sacrificing emergency savings, retirement contributions, and basic lifestyle stability?” In this case, the family may choose to increase the down payment, reduce other monthly debt first, look for a lower-tax area, or target a slightly lower purchase price.

Common Hidden Cost Traps in Homeownership

Many first-time buyers underestimate ownership costs because they focus on the mortgage payment alone. In real life, the home does not stop costing money after closing.

Why This Calculator Uses a 1.5% Maintenance Cost

A 1.5% annual maintenance reserve means setting aside about 1.5% of the home’s value each year for repairs, upkeep, and replacement items. On a $400,000 home, that equals about $6,000 per year, or $500 per month. That may sound high until you face one major repair.

- Roof repairs or replacement: A damaged or aging roof can cost thousands of dollars, and full replacement can be much higher.

- HVAC replacement: Heating and cooling systems often fail at inconvenient times and can create a large one-time expense.

- Lawn care and landscaping: Mowing, irrigation, tree trimming, pest control, and seasonal cleanup are easy to overlook.

- Plumbing and water damage: Leaks, water heaters, sewer lines, and drainage problems can become urgent and expensive.

- Appliances: Refrigerators, washers, dryers, ovens, and dishwashers eventually need repair or replacement.

- HOA special assessments: Condo and HOA communities may charge special assessments for roofs, elevators, exterior repairs, or community infrastructure.

The goal of the maintenance estimate is not to predict the exact amount you will spend every year. The goal is to protect your budget from the years when several expensive items happen at once.

How to Determine Mortgage Affordability?

To determine mortgage affordability, you generally follow these steps:

- Set Your Monthly Budget: Decide how much you can comfortably pay each month for all housing costs, including mortgage, property taxes, insurance, and maintenance.

- Estimate Additional Costs: Besides the mortgage principal and interest, factor in property taxes, homeowners insurance, private mortgage insurance (if applicable), and upkeep costs. These usually add around 1.5% to 3% of the home’s value annually.

- Calculate Maximum Mortgage Payment: Subtract the estimated monthly extra costs from your total monthly housing budget. The remainder is what you can spend on your mortgage payment (principal + interest).

- Use a mortgage calculator or Formula: With your mortgage payment budget, loan term (usually 15 or 30 years), and interest rate, calculate the maximum loan amount you can afford.

- Add Down Payment: Remember, the price of a home equals the loan amount plus your down payment.

Example:

- Monthly budget: $1800

- Estimated extra costs: $600/month

- Maximum mortgage payment: $1200/month

- At 6% interest over 30 years, $1200/month might support a loan of about $200,000

- With 20% down, home price = $200,000 ÷ 0.8 = $250,000

By following this method, you get a clear, realistic view of what home price fits your budget. For precise qualification, consult with lenders or use the calculator on this page.

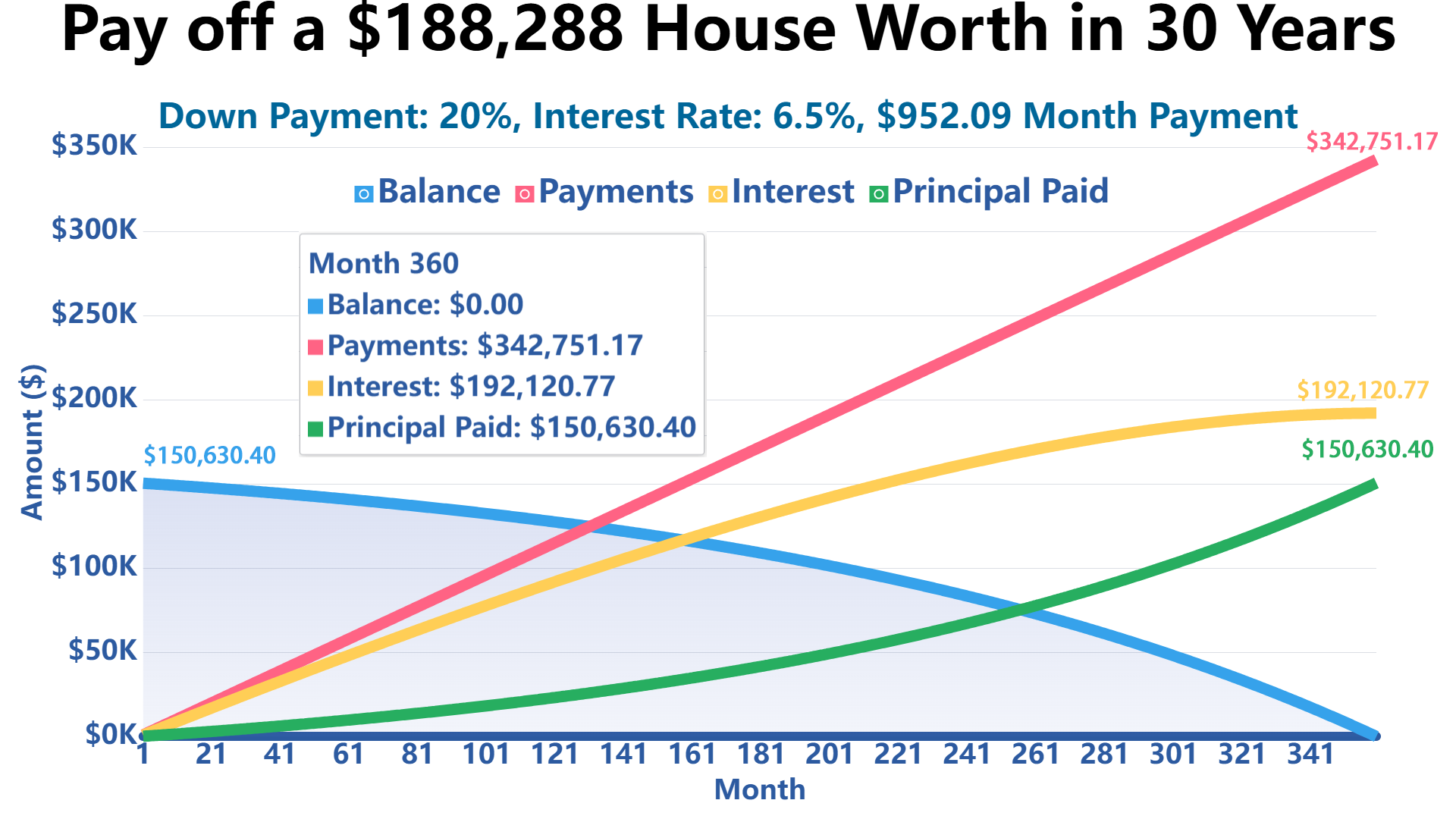

If My Monthly Housing Budget Is $1,500, How Much House Can I Afford?

If you're looking at a 30-year loan with 20% down, a fixed rate of 6.5%, property tax at 1.5% per year, home insurance at 0.5% per year, and maintenance costs at 1.5% per year, then you can afford a house worth about $188,288.

At that price, your monthly mortgage payment would be $952.09, property tax would be $235.36, home insurance $78.45, and maintenance costs $235.36.

Reference

Government Resources

- Consumer Financial Protection Bureau (CFPB): Your home loan toolkit - Comprehensive guide to the home buying process

- Federal Housing Administration (FHA): FHA Home Loans - Information about government-backed mortgages

- U.S. Department of Housing and Urban Development (HUD): Buying a Home - Government guidance on home purchasing

- Federal Reserve: A Consumer's Guide to Mortgage Lock-ins - Understanding mortgage terms and conditions

- Internal Revenue Service (IRS): Deductible Real Estate Taxes - Tax implications of homeownership

Professional Guidance

- Find HUD-Approved Housing Counselors: Free Housing Counseling - Locate certified housing counselors in your area

- National Association of Realtors: Home Buyers Guide - Professional real estate guidance

- Mortgage Bankers Association: Consumer Resources - Industry insights and guidance

Financial Education

- MyMoney.gov: Federal Financial Literacy and Education Commission - Government financial education resources

- CFPB Financial Well-being: Financial Well-being Resources - Tools for financial planning

Mortgage Affordability FAQ

Is the mortgage payment the same as the full monthly housing cost?

No. The mortgage payment usually refers to principal and interest. Your full housing cost may also include property tax, homeowners insurance, PMI, HOA fees, maintenance, utilities, and local assessments.

Why does property tax change affordability so much?

Property tax is usually based on the home value and local tax rate. A state or county with a high tax rate can make a lower-priced home more expensive on a monthly basis than buyers expect.

When can PMI be removed?

PMI may often be removed once the borrower reaches sufficient home equity, commonly around 20%, depending on loan type, payment history, property value, and lender rules. Contact your lender directly to confirm the exact process.

How much should I budget for home maintenance?

A common planning range is about 1% to 2% of the home’s value per year. This calculator uses 1.5% as a practical middle estimate, but older homes, larger homes, and properties in harsh climates may require more.

What DTI ratio do lenders prefer?

Many lenders use the 28/36 rule as a conservative benchmark, meaning housing costs near 28% of gross income and total debt near 36%. Some loan programs may allow higher ratios, but higher approval does not always mean the payment is comfortable.

Write Reply to This Calculator