Compound Interest Calculator

Calculate investment growth with monthly, yearly, weekly deposits and withdrawals.

Compound Interest Calculator

Calculation Results

Accumulation Table

Investment Visualization

How Is Compound Interest Calculated?

The compound interest formula is derived from the principle that each period's interest becomes part of the principal for the next period's calculation:

Year 1: A₁ = P(1 + r/n)ⁿ

Year 2: A₂ = P(1 + r/n)²ⁿ

Year t: Aₜ = P(1 + r/n)ⁿᵗ

- A = Final amount

- P = Principal (initial investment)

- r = Annual interest rate (decimal)

- n = Number of times interest compounds per year

- t = Number of years

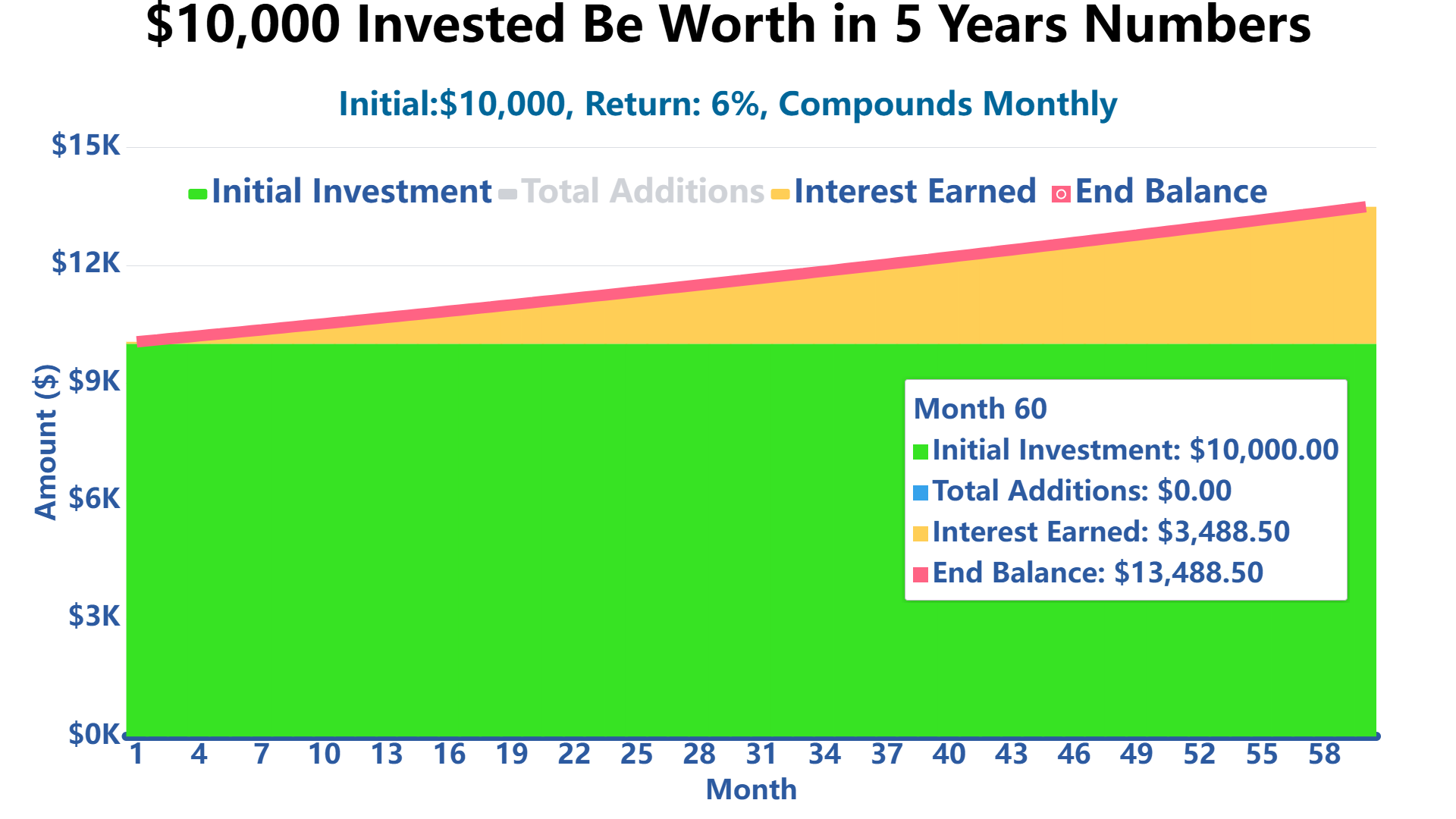

How Much Is $10,000 Worth at the End of 5 Years if the Interest Rate of 6% Is Compound Monthly?

If you put $10,000 into a five-year savings account with a 6% annual interest rate that compounds monthly, after five years your account balance will grow to $13,488.50.

| Initial Investment Amount | 5 Years at 6% Interest ($) | 10 Years at 6% Interest ($) |

|---|---|---|

| $5,000 | $6744.25 | $9096.98 |

| $10,000 | $13488.50 | $18193.97 |

| $15,000 | $20232.75 | $27290.95 |

| $20,000 | $26977.00 | $36387.93 |

| $25,000 | $33721.25 | $45484.92 |

| $30,000 | $40465.50 | $54581.90 |

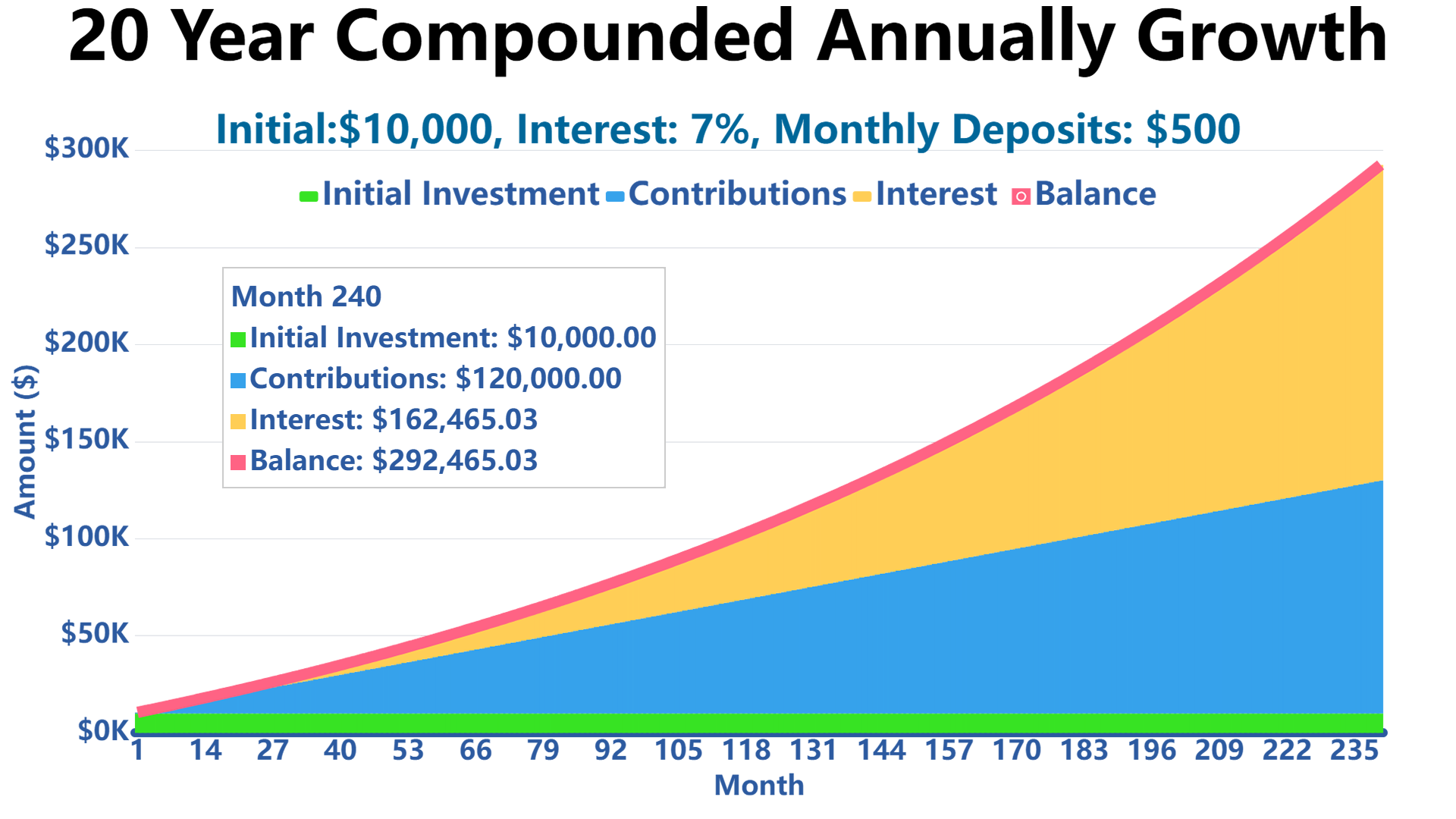

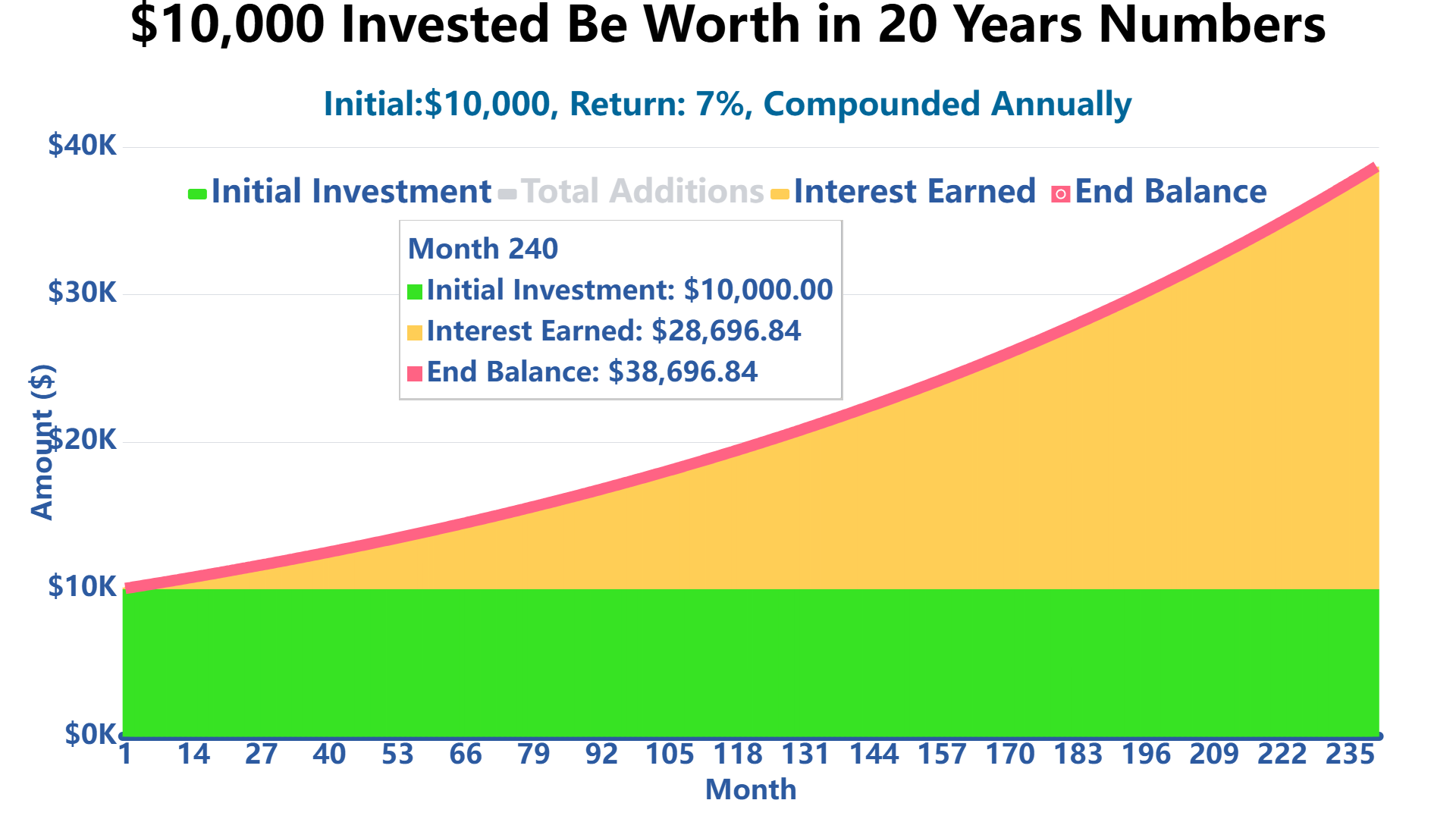

How Much Will $10,000 Invested Be Worth in 20 Years?

$10,000 invested at 7% compounded annually for 20 years would be worth approximately $38,696.84.

| Initial Investment Amount | 20 Years at 7% Interest ($) | 25 Years at 7% Interest ($) |

|---|---|---|

| $5,000 | $19348.42 | $27137.16 |

| $10,000 | $38696.84 | $54274.33 |

| $15,000 | $58045.27 | $81411.49 |

| $20,000 | $77393.69 | $108548.65 |

| $25,000 | $96742.11 | $135685.82 |

| $30,000 | $116090.53 | $162822.98 |

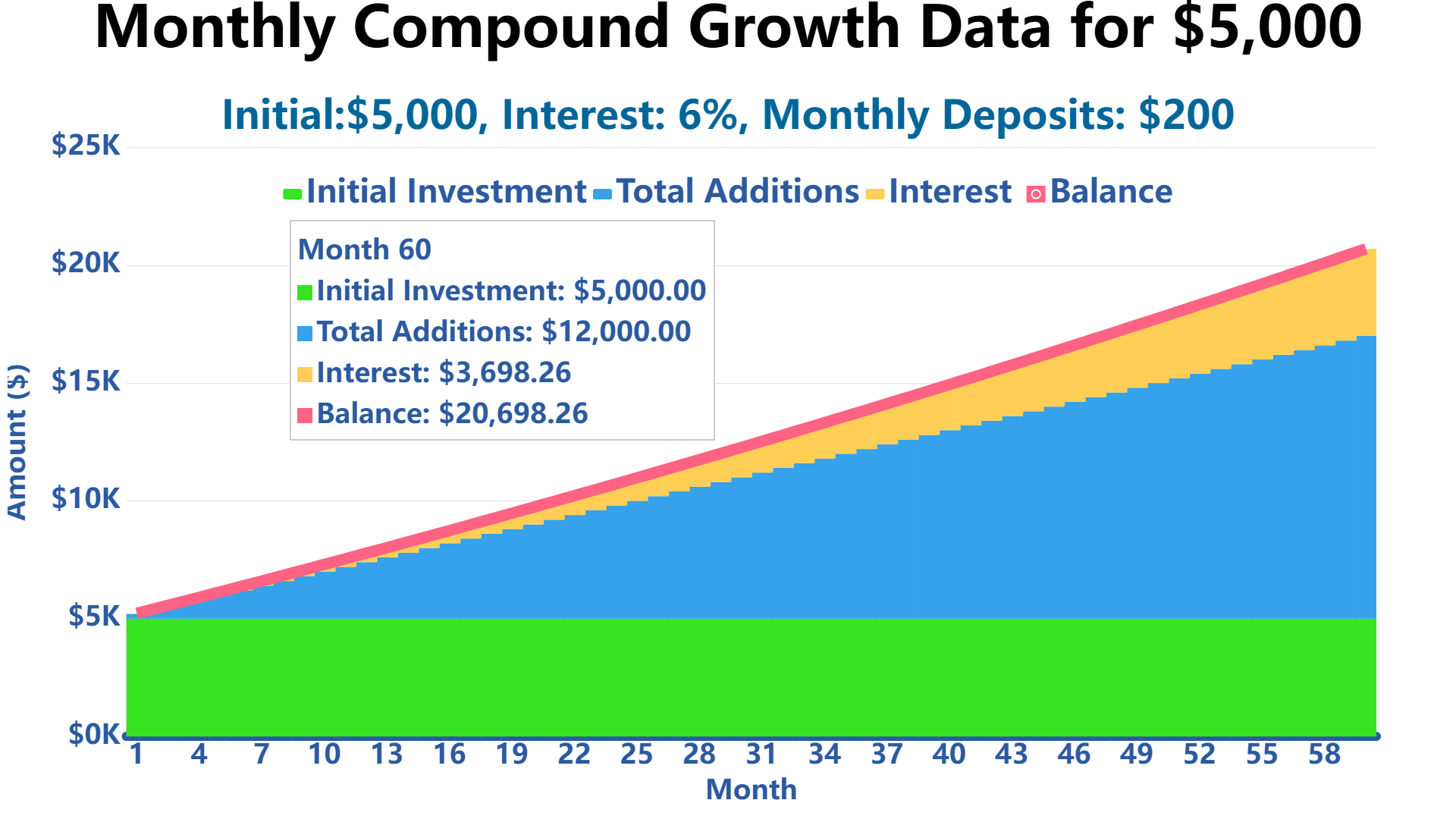

If You Deposit $5,000 With a 6% Annual Interest Rate That Compounds Monthly, and Then Add $200 at the End of Each Month, How Much Will You Have After 5 Years?

You'll have $20,698.26, which includes $3,698.26 in interest earned and $12,000 in additional deposits.

| Initial Investment Amount | 5 years, $200 monthly contribution | 10 years, $200 monthly contribution |

|---|---|---|

| $5,000 | $20,698.26 | $41872.85 |

| $10,000 | $27442.51 | $50969.84 |

| $15,000 | $34186.76 | $60066.82 |

| $20,000 | $40931.01 | $69163.80 |

| $25,000 | $47675.26 | $78260.79 |

| $30,000 | $54419.51 | $87357.77 |

References

For additional information about investing and compound interest, consult these authoritative government sources:

- U.S. Securities and Exchange Commission: Investor.gov - The SEC provides comprehensive resources to help investors understand compound interest and make informed investment decisions

- Consumer Financial Protection Bureau: CFPB.gov - Consumer protection and financial education resources

- Federal Trade Commission: FTC.gov - Consumer protection and investment fraud prevention

- Internal Revenue Service: IRS.gov - Tax implications of investments and retirement accounts

2 Replies to This Calculator