Debt Snowball Calculator

Compare Paying off Your Current Debts Using the Debt Snowball Method Versus Making Only Minimum Payments.

Debt Snowball Calculator

Calculation Results

| Month | Principal | Interest | Payment | Ending Balance | Cumulative Principal | Cumulative Interest | Cumulative Payment |

|---|

How the Debt Snowball Calculator Works?

This calculator estimates your debt payoff schedule by applying your monthly budget across all listed debts. First, it adds monthly interest to each balance based on the annual percentage rate (APR). Then it applies the minimum payment to each debt. Any remaining amount from your monthly budget is directed toward the debt with the smallest balance, which is the core principle of the debt snowball method.

Once a debt is fully paid off, the amount that had been going toward that debt becomes available for the next smallest balance. This process continues month by month until all debts are paid in full. The results may include your estimated payoff period, total interest paid, total amount paid, and a month-by-month repayment schedule.

Why Use a Debt Snowball Strategy?

Many people choose the debt snowball approach because it can provide quick psychological wins. Paying off smaller balances first may help you stay motivated and consistent. Even if another strategy may reduce interest faster in some cases, the debt snowball method is often valued for its simplicity and momentum-building approach.

How to Use the Debt Snowball Method to Pay Off Debt?

Debt snowball example

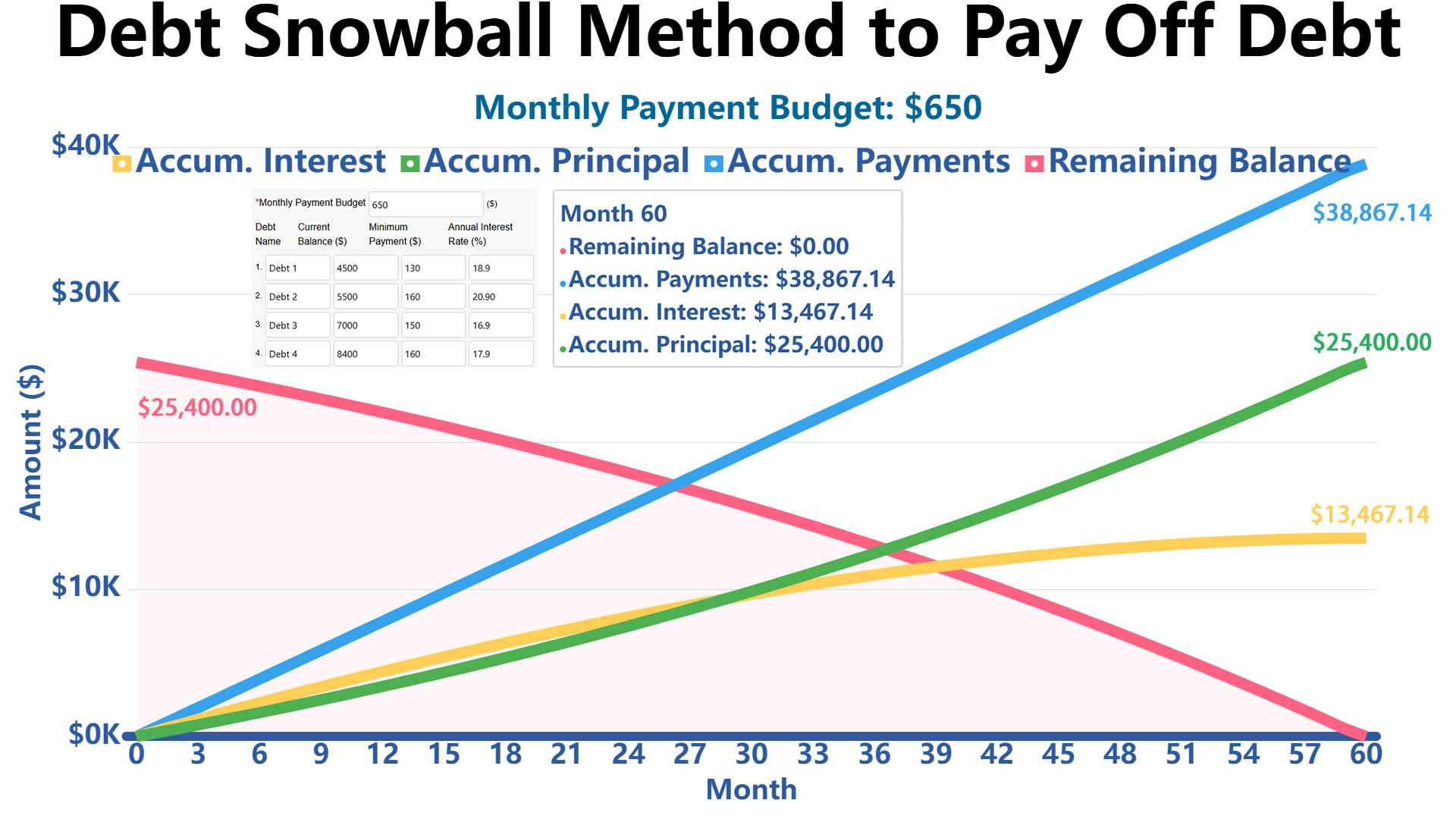

Monthly budget set aside for debts: $650

Let’s say you have the following debts:

- Debt 1 balance: $4,500 at 18.9% interest, with a $130 minimum payment.

- Debt 2 balance: $5,500 at 20.9% interest, with a $160 minimum payment.

- Debt 3 balance: $7,000 at 16.9% interest, with a $150 minimum payment.

- Debt 4 balance: $8,400 at 17.9% interest, with a $160 minimum payment.

With a monthly payment of $650.00, all debts will be cleared in 60 months (5 years 0 months). Total paid: $38,867.14, including $13,467.14 in interest.

| Debt | Unpaid Balance | APR | Payoff Duration | Total Interest | Total Payments | Repayment Schedule |

|---|---|---|---|---|---|---|

| #1: Debt 1 | $4,500.00 | 18.90% | 33 months(2 years 9 months) | $1,264.53 | $5,764.53 | Pay $180.00/month until month #32,Then Pay $4.53/month until month #33 to pay off. |

| #2: Debt 2 | $5,500.00 | 20.90% | 41 months(3 years 5 months) | $2,646.65 | $8,146.65 | Pay $160.00/month until month #32,Then Pay $335.47/month until month #33,Then Pay $340.00/month until month #40,Then Pay $311.18/month until month #41 to pay off. |

| #3: Debt 3 | $7,000.00 | 16.90% | 51 months(4 years 3 months) | $3,622.82 | $10,622.82 | Pay $150.00/month until month #40,Then Pay $178.82/month until month #41,Then Pay $490.00/month until month #50,Then Pay $34.01/month until month #51 to pay off. |

| #4: Debt 4 | $8,400.00 | 17.90% | 60 months(5 years 0 months) | $5,933.13 | $14,333.13 | Pay $160.00/month until month #50,Then Pay $615.99/month until month #51,Then Pay $650.00/month until month #59,Then Pay $517.14/month until month #60 to pay off. |

FAQ

What Is the Debt Snowball Method?

The debt snowball method is a repayment strategy where you focus extra payments on the debt with the smallest balance first, while continuing to make minimum payments on all other debts.

Does the Debt Snowball Method Save the Most Interest?

Not always. A debt avalanche strategy, which targets the highest interest rate first, may reduce total interest more quickly in some situations. However, many people prefer the debt snowball method for its motivational benefits.

Can I Use This Calculator for Loans and Credit Cards?

Yes. You can use it for many types of debts as long as you know the current balance, minimum payment, and annual interest rate.

References

For general consumer financial education and debt-related guidance, you may review resources from official government and public agencies, including:

- Consumer Financial Protection Bureau (CFPB)

- USA.gov – Credit and Debt

- Federal Trade Commission (FTC)

Write Reply to This Calculator